Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The first week of a new month features the US jobs data. It is the most important economic report of a new month. It sets the broad tone for much of the economic data over the next several weeks, including consumption, industrial production, and construction spending.

However, there are two reasons why it may not pack the punch it has in the past. First, the bar to dissuade the market against a 25 bp rate hike on September 26 is very high. The market has discounted about a 95% chance of a hike, up from about 82% at the end of July. The January 2019 fed funds futures contract, the contract that offers the best insight into the year-end rate expectations, was virtually unchanged in August, discounting a little less than a 2/3 chance of a December hike.

Second, there are larger more powerful forces at work. Trade tensions are set to rise. The public comment period for the new tariff that the Trump Administration wants to levy on $200 bln of imports from China ends on September 6. The US President has made it clear that he intends to move forward as China has not signaled its willingness to change its behavior. China has responded by announcing that it will retaliate with tariffs on $60 bln its imports from the US. Even if the tariffs are not implemented immediately, it will cast a pall over the investment climate.

Trump also indicated that he will get around to addressing Europe’s unfair trade practices too. He dismissed as insufficient Europe’s offer, according to reports, to drop all auto tariffs. Europe is chaffing under a series of actions that the US has taken over the past two years, including pulling out of the Paris Agreement, slapping its steel and aluminum with tariffs justified on national security grounds, and the unilateral withdrawal from the treaty with Iran. Trump encouraged the UK to leave the EU and has offered France “a better deal” if it left too. At the end of last week, Trump again threatened to leave the WTO, “if it does not shape up.”

Meanwhile, NAFTA negotiations were not concluded at the end of last week. Talks will resume the middle of next week. Canada appears willing to cede some market share to the US dairy industry, but it cannot accept the steel and aluminum tariffs and the weakening of the conflict resolution mechanism. However, the White House has gone ahead and notified Congress that it planned to sign a deal with Mexico in 90-days and Canada can “join if it is willing.” By informing Congress on August 31, it allows the current president of Mexico to sign the agreement before AMLO takes office on December 1.

Since Congress had authorized the President to negotiate a trilateral agreement and he has submitted a bilateral agreement, the stage is set for a battle between the two branches. Also, if the lame duck Congress does not return to take up the measure, the duty will fall to the next Congress. The composition of the next Congress is not known, polls suggest the historical pattern in which the party that controls the executive branch loses seats in the legislative branch, will likely remain intact.

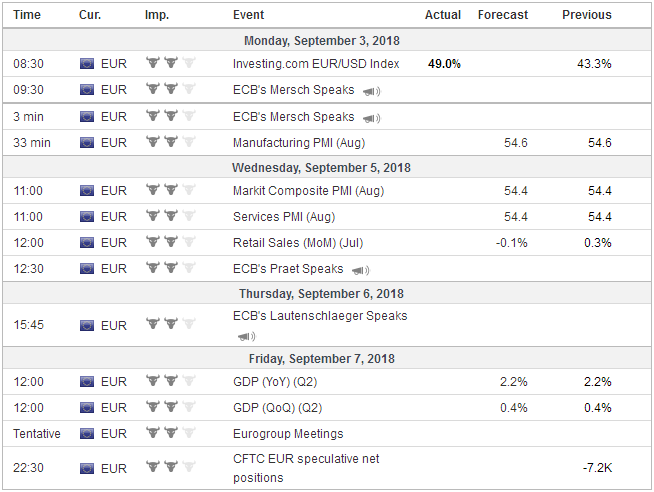

United StatesIt is not that the US jobs data are unimportant. It is the continued strong jobs growth more than wage growth that appears to be fueling US consumption that rose 3.8% at an annualized rate in Q2. Non-farm payrolls have expanded by 200k a month on average over the past 12 months. Job growth has averaged 215k this year. The weakness in July (157k), the lower end of this year’s range, is not expected to be repeated and recovery back toward the long-term average is expected. Manufacturing jobs growth is expected to remain strong. It is largely accounted for by the energy sector. The unemployment rate which eased to 3.9% in July from 4.0% in June can return to the multi-year low of 3.8% seen in May. The Fed targets core inflation because research indicates the headline rate gravitates to the core rate and not the way around. Many economists see the core rate as driven by wages. Hourly earnings need to rise 0.2%, which is the 12- and 24-month average, in order to keep the year-over-year pace at 2.7%. The year-over-year rate has not been above 2.8% since 2009. US auto sales will be reported on September 4. Lower incentives (especially for sedans), rising interest rates and higher prices make for adverse market conditions. The year-over-year comparison will be flattered by the storms that hit the auto market last August. July auto sales of 16.68 mln vehicles (SAAR) was the weakest since last August. Most economists are looking for a small recovery toward 16.80 mln. That would be the second month below the 17.0 mln unit pace for the first time since last summer. Disappointment could knock forecasts for retail sales, and consumption more broadly. |

Economic Events: United States, Week September 03 - Click to enlarge |

EurozoneThe ECB meets on September 13. The staff will update its economic forecasts, but there will not be a rate hike for another year. That takes some of the sting from high-frequency data, like the slight downward revision to the August CPI. Two large exogenous variables that the ECB does not target but plays a role in its forecasts, the euro on a trade-weighted basis and oil, are little changed net-net since mid-June. The flash PMI for August points to a robust rebound by Germany after a soft patch earlier this year and a somewhat less impressive recovery in France. Germany’s July factory orders and industrial output are expected to rebound after June’s weakness. The flash PMI hinted at softer activity in the periphery. This is likely to be borne out in the final readings in the coming days. Although the EMU economy has slowed from the 0.7% quarterly prints in the last nine months of 2017, activity remains solid and near what the ECB sees as trend growth. The 0.4% estimate for Q2 growth is expected to be confirmed, and growth here in Q3 seems similar. There maybe downside risk to July EMU retail sales. Spain and Germany reported disappointing numbers ahead of the weekend Spain saw a 0.6% decline, which offset the June increase and put the year-over-year rate at -0.4%, the weakest in four years. Falling 0.4%, German retail sales were twice as bad as expected. The year-over-year fell to 0.8%. The average year-over-pace this year through July is 1.3% compared with 2.4% both the same period last year and 2017 entirely. More important for investors than the eurozone high-frequency data is rising tensions from Italy and Spain ahead of the submission of the 2018 budget. The premium over Germany is widening sharply and on a purely directional basis, is inversely correlated with the euro. This means that the euro tends to weaken as the spreads widen. The Italian premium on 10-year yields widened to a new six-year high ahead of the weekend of 290 bp. Seven weeks ago, it was below 220 bp and began the year near 150 bp. |

Economic Events: Eurozone, Week September 03 - Click to enlarge |

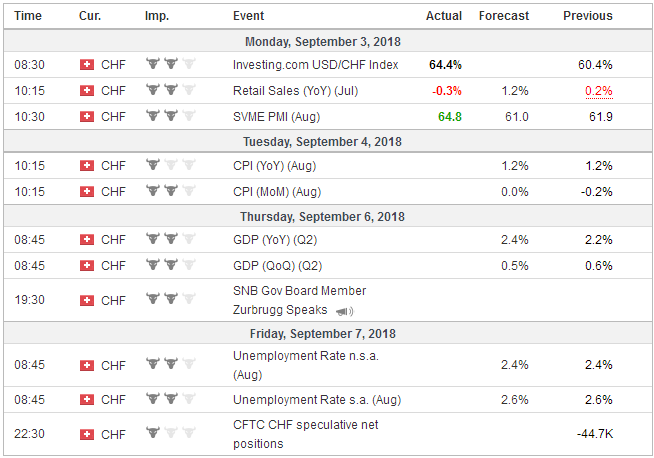

Switzerland |

Economic Events: Switzerland, Week September 03 - Click to enlarge |

Italian bonds often behave like risk assets, and the sell-off in emerging market does not help matters, but the main factor is home-grown. The nationalist-populist government is looking to take on the EU on budget and immigration issues. The link between Italian sovereign bonds and Italy banks remains tight. An index of Italian bank stocks fell 17% in August. It began the month off 2% for the year. The index is testing an important technical level near 8800. That is the 61.8% retracement of the recovery from the 2016 low near 6410, which matched the 2012 low. Ahead of the weekend, Fitch changed the outlook for Italy’s BBB credit rating to negative from stable.

Spain’s new government will also likely test the EC budget rules, but the economy is stronger, thanks, at least in part, to more fiscal stimulus and ability to recapitalize the banks before the rules changed. Still, Spain’s premium has risen proportionately almost as much as Italy’s. In the first part of the year, the premium was near 66 bp. It is now testing the highs seen around the middle of August near 115 bp. In May, the premium briefly spiked a little above 135 bp.

Three major central banks meet next week, and none are expected to move. The Bank of Canada is the closest to hiking rates. A robust employment report at the end of the week after disappointing July data will reinforce expectations for a hike in October. The Reserve Bank of Australia is nowhere near a hike, and the central bank is unlikely to push back against the Australian dollar’s weakness. A little below $0.7200, the Australian dollar is about 6.5% rich to the OECD’s measure of purchasing power parity.

Sweden’s Riksbank meets, and although it has hinted it could begin raising rates, the market expects it to wait longer and past October 24, its next meeting. The euro made fresh nine-year highs against the krona last week near SEK10.73. The technicals are stretched, and it appears a correction may have begun, and over the last couple of sessions, the euro has pulled back almost 1% (~SEK10.60). A 38.2% correction to the August rally puts the euro by SEK10.54, and a 50% retracement is found close to SEK10.48. That said, national elections on September 9 looms over the price action in the week ahead.

Even investors with no exposure to emerging markets will be watching Turkey {CPI}, Argentina {IMF negotations}, South Africa and Brazil. Although Fed tightening and a strong dollar make for a challenging environment, poor policies and domestic political factors are playing a central role. Quietly and without much fanfare, the Indian rupee fell to record lows last week. It has weakened every month this year since January. The nearly 3.5% loss last week brings depreciation to 10% this year, the most in Asia. It is also the most after the BRATS (Brazil, Russia, Argentina, Turkey, and South Africa). Investors will also monitor the CNY-fixing after officials re-introduced counter-cyclical factor again in the process. China may report reserves toward the end of the week, and they are expected to be little changed in August.

Full story here Are you the author?Tags: #USD,$AUD,$CAD,$CNY,$EUR,Italy,newsletter,SEK