Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

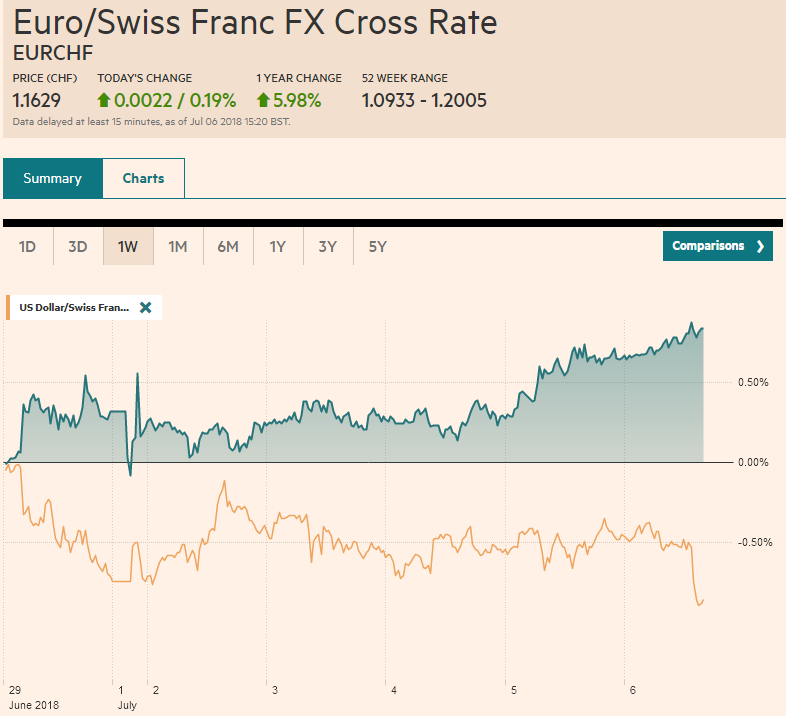

Swiss FrancThe Euro has risen by 0.19% to 1.1629 CHF. |

EUR/CHF and USD/CHF, July 06(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe first set of US tariffs aims specifically at China were implemented, and the retaliatory actions were also launched. The tariffs cover hundreds of goods, though the initial amount of trade covered is relatively small at $34 bln. Tariffs on another $16 bln are in the pipeline and could be put into effect in a few weeks. The US is threatening to ramp up its response by imposing a tariff on another $200 bln of Chinese goods, though the details have not been announced. The market has taken the action in stride, but rising trade tensions are among the major risks for investors and policymakers. This evident in the FOMC minutes released yesterday and will likely feature in Fed chief’s Powell’s prepared remarks to be published next week ahead of semi-annual congressional testimony. Although many observers are disturbed by the treatment of Canada and Europe as security threats for steel, aluminum, and possibly autos but are broadly sympathetic to action against China, even if tariffs are seen as counter-productive. Asian equities rose, with the MSCI Asia Pacific Index ending a four-day slide with a 0.6% rise. While the week’s losses were pared, the 1.5% decline extends the rout for the fourth week, the longest downdraft in over a year. Singapore was a notable exception. The 2.3% decline was spurred by an expected tightening of restrictions against speculation in the property market. Malaysia was the other exception to regional advance. The decline in Singapore and trade tensions took a toll on financial and consumer sectors. |

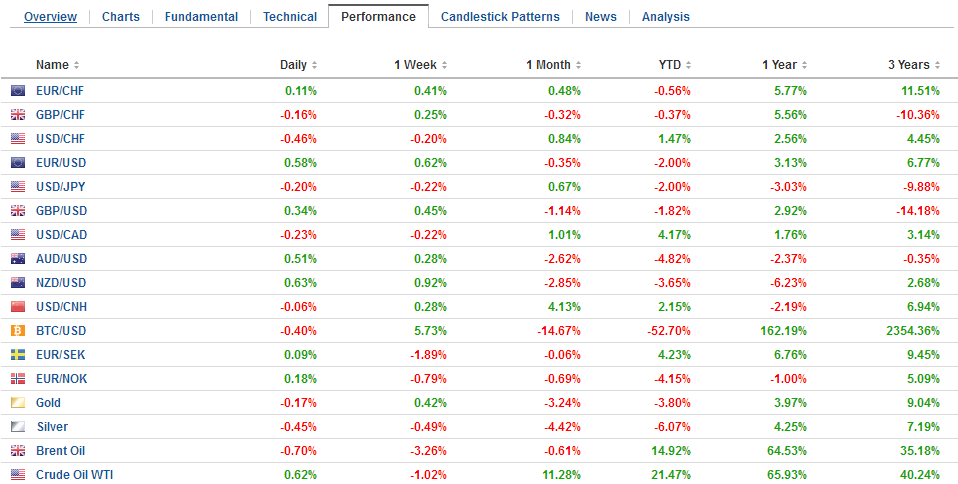

FX Performance, July 06 - Click to enlarge |

Japan reported both an unexpected surge in labor income and a sharp fall in household spending. Cash earnings rose 2.1% year-over-year in May. This matches the strongest increase since the last 1990s. Real cash earnings rose 1.3%, which is the strongest in a couple years. However, despite the apparent wherewithal, Japanese households were thrifty. Household spending fell more than twice what economists expected. The 3.9% decline, year-over-year, compared with a 1.3% decline in April, and forecasts for a 1.5% drop. Poor weather may have exacerbated the fall, but it is the fourth consecutive decline.

The dollar has been confined to a narrow range of about a quarter yen around the middle of this weeks range (~JPY110.30-JPY111.15). Ahead of the US employment data, the dollar is nursing a small loss on the week. There is a $572 mln option at JPY110.50 that expire today.

On the heels of a strong recovery in factory orders, Germany reported an impressive recovery in industrial output. The 2.6% surge compares with forecasts for a 0.3% rise. It is only the second monthly increase this year and the largest since last November and follows a downward revision to the April series from -1.0% to -1.3%.

European stocks are trading higher for the fourth consecutive session, which is the longest streak in two months. All sectors are higher but energy. Oil prices are edging lower after yesterday’s unexpected increase in US oil inventories and reports that Saudi Arabia was shaving prices for July delivery. Of the large European bourses, Spain has performed the best this week with a nearly 3% advance. Sweden, where the Riksbank has confirmed its intention to hike rates later this year, has one of the worst performing markets this week with a little more than a 2% loss.

For the sixth session, the euro is recording a higher low. It also set a new three-week high by edging briefly above $1.1720. The net important technical objective is found near $1.1850. The US jobs report will likely widen today’s narrow range of less than half a cent, and some chunky options expirations may influence the price action There is an option at $1.1750 for nearly 660 mln euros that expire, and 2.1 bln euros struck at $1.1700. Below the figure, there are options at $1.1650 and $1.1675 (for 820 mln euros and 1.2 bln euros respectively) that also will be cut today.

Sterling is trying to end a three-week slide. It is up about a quarter of a cent for the week before the North American session. Initial resistance is seen in the $1.3275-$1.3300 ara. It is pulled in two directions. On the one hand, BOE Governor Carney sounded increasingly confident yesterday that soft economic start to the year was fading and that inflation pressures continue to build. This reinforces ideas that Reuters survey now suggests is the consensus that the BOE will likely hike rates next month.

On the other hand, Brexit remains a mess. Prime Minister May’s special cabinet meeting today was supposed to hammer out a consensus for a unified government position. Not only has the UK’s chief Brexit negotiator determined that the Prime Minister’s plan for a new customs union-like proposal was unworkable, but the EC and Germany have indicated it is not sufficient. In fact, the UK’s push for an agreement on goods but not services plays into the critics’ hands who claim the UK is still engaged in cherry picking at this late stage.

The focus in the North American session will be on US jobs data. After averaging 221k net new private sector jobs a month in Q1 ( and 223k in Q4 17), it has averaged 190k in Q2, and that is around the median forecast for June. ADP estimate averaged 227k in Q1 and 178k in Q2. Job growth is not the chief concern now. Rather attention is on hourly earnings growth, which is understood to be a key element in inflation expectations as well as income that supports consumption, which drives the economy.

Economists are looking for a 0.3% increase. That would equal the May increase and lift the year-over-year rate to 2.8%, which would match the fastest pace in recent years. The last time average hourly earnings rose more than 2.8% year-over-year was in 2010. Despite increasing concerns that the trade tensions are already impacting some business investment decisions, the market remains convinced the Fed will hike rates again in September and roughly an 80% chance has been discounted.

Separately, the US reports its May trade balance. The US trade deficit peaked near $55.5 bln in February and has been slowly improving. The preliminary data suggests it continued to improve in May. The deficit is expected to have fallen from $46.2 bln in April to a little below $44 bln in May. Still, in the broader picture, the US deficit is expanding, and it is running about 10% wider than a year ago.

Canada also reports its June employment data and the May merchandise trade balance. The reaction to the US reports typically overshadows the response to the Canadian data. Firm Canadian jobs growth after a soft May report will likely add confidence to the now consensus view that the Bank of Canada will hike rates at next week’s meeting. Canada is expected to have grown around 30k full-time positions after losing nearly as many in May. Hourly earnings for permanent employees may slow from the lofty 3.9% pace to 3.7%. After the merchandise trade deficit was halved in April, it is expected to have widened a bit in May.

The US dollar has been confined to a narrow CAD1.3115 to CAD1.3160 range for the past two sessions. It remains stuck in it ahead of the economic reports. The intraday technicals seem to favor the upside for the US dollar, but resistance near CAD1.3200, reinforced by options expirations may limit the enthusiasm.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,EUR/CHF and USD/CHF,newslettersent,yuan