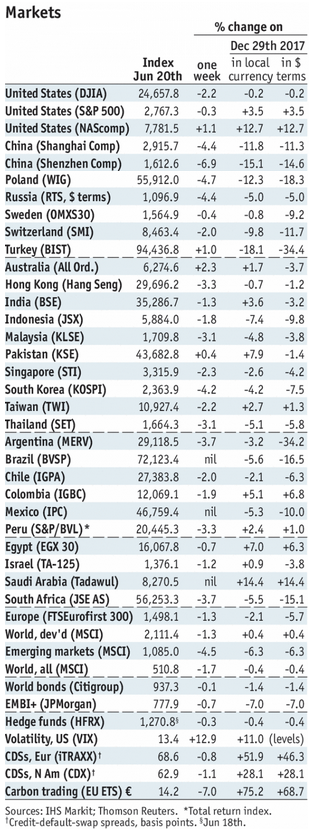

Stock MarketsEM FX ended Friday mixed, and capped off a mixed week overall as the dollar’s broad-based rally was sidetracked. EM may start the week on an upbeat after PBOC cut reserve requirements over the weekend. Best EM performers last week were ARS, MXN, and TRY while the worst were THB, IDR, and BRL. |

Stock Markets Emerging Markets, June 20 - Click to enlarge |

IndonesiaIndonesia reports May trade Monday. Exports are expected to rise 6% y/y and imports by 12% y/y. Bank Indonesia meets Thursday and is expected to hike rates 25 bp to 5.0%. Though inflation remains low, the bank has hiked twice already to help support the rupiah. SingaporeSingapore reports May CPI Monday, which is expected to rise 0.3% y/y vs. 0.1% in April. The MAS does not have an explicit inflation target. May IP will be reported Tuesday and is expected to rise 10.2% y/y vs. 9.1% in April. The economy is in solid shape, but low price pressures and rising headwinds will likely keep the MAS on hold at its October policy meeting. BrazilBrazil reports May current account data Monday, and a $935 mln surplus is expected. COPOM minutes will be released Tuesday. The central bank will release its quarterly inflation report Thursday. Central government budget data for May will be reported that day too, and a -BRL9.2 bln primary deficit is expected. Consolidated budget data will be reported Friday, and a -BRL10 bln primary deficit is expected. If the real continues to weaken, the FX losses from the swaps will start showing up more in the budget data. Czech RepublicCzech National Bank meets Wednesday and is expected to keep rates steady at 0.75%. However, the market is split. Of the 17 analysts polled by Bloomberg, 13 see steady rates and 4 see a 25 bp hike to 1.0%. If not this week, then the bank will likely hike at the next meeting August 2. MexicoMexico reports May trade Wednesday, and a -$700 mln deficit is expected. Higher oil prices in the wake of the OPEC meeting should boost exports going forward. Banco de Mexico hiked 25 bp last week, due in part to the weak peso. Despite the ensuing bounce, we think weakness will resume as the July 1 election approaches. PolandPoland central bank releases its minutes Thursday. While Czech has already started hiking and Hungary has tilted more hawkish, Poland stands out for remains ultra-dovish. At that meeting, officials hinted at steady rates into 2020, extending beyond current forward guidance of steady rates through 2019. Next policy meeting is July 11, no change expected then. KoreaKorea reports May IP Friday, which is expected to be flat y/y vs. 0.9% in April. The economy appears to be slowing, even as price pressures remain low. We believe the BOK will remain on hold for much of this year. Next policy meeting is July 12, no change expected then. TurkeyTurkey reports May trade Friday, which is expected at -$7.7 bln. If so, the 12-month total would rise to -$87 bln, the highest since June 2014. As of this writing, the election results are not yet in but the political outlook will be key for monetary policy going forward. Next policy meeting is July 24. South AfricaSouth Africa reports May trade, budget, money, and private sector credit data Friday. Data is expected to confirm that the economy remains weak. Despite lower inflation, the SARB cannot cut rates due to the rand’s vulnerabilities. Next policy meeting is July 19, no change expected then. ColombiaColombia central bank meets Friday and is expected to keep rates steady at 4.25%. CPI rose 3.2% y/y in May, near the 3% target and within the 2-4% target range. Even though the economy remains sluggish, we think the easing cycle is over for now due to the weak peso. ChinaChina reports official June PMI Saturday, which is expected at 51.8 vs. 51.9 in May. This will be the first snapshot for June, with most of the data deluge coming around the middle of this month. May data showed some slowing, and so markets will be keen on seeing if that weakness carried over into June. Over the weekend, the PBOC cut reserve requirements for some commercial banks. |

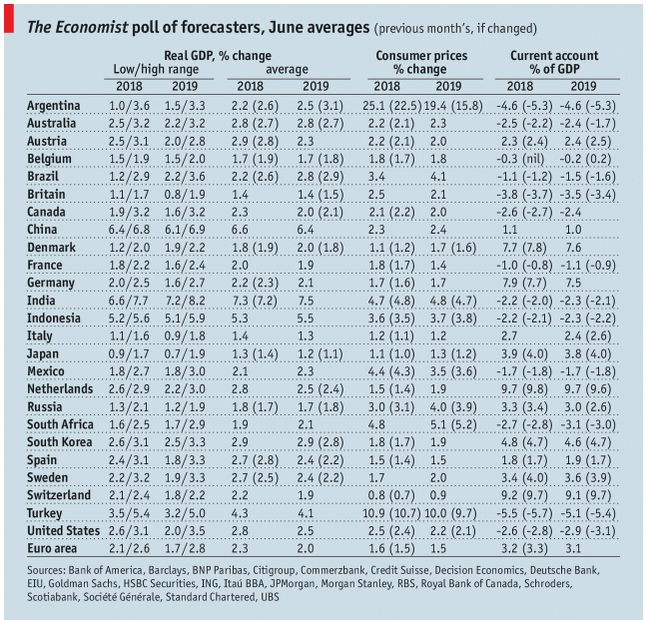

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, June 2018 Source: economist.com - Click to enlarge |

Full story here Are you the author?

Tags: Brazil,China,Colombia,Czech Republic,Emerging Markets,Indonesia,Korea,Mexico,newslettersent,Poland,Singapore,South Africa,Turkey,win-thin