Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The consensus narrative is that with rising inflation it is understandable that next week’s meeting is live and that the confirmation of such has lifted the euro to ten-day highs, dragging the dollar broadly. However, to accept this is to accept the debasement of language. Until now, we dubbed central bank meeting that could result in action as “live.” For example, given that the Fed has not changed interest rates since the hiking cycle began in December 2015 outside of a meeting with a pre-scheduled press conference. Hence last months meeting in May was not live.

The ECB meeting is not “live” in that sense. The ECB is not about to stop its asset purchases, which will run through September, and possibly tapered further in Q4. It is not about to raise interest rates, which even the consensus sees at least a year off. How is the ECB meeting live? It is now said to be live in the sense that the ECB will formally debate what happens after September.

Moreover, this is not really news. ECB executive member Sabine Lautenschlaeger, who incidentally, would likely have to resign from the Board if Weidmann succeeds Draghi at the helm, was clear last month that such a debate was likely in June. Those of us that expected an announcement at the July 26 meeting had assumed a debate would take place before it.

ECB’s Praet speech today did not contain any new color. He told investors what they already knew. After the Easter distortions drop out, it is clearer that price pressures are moving toward the ECB target. And given what has happened to the euro and oil, it is not difficult to connect the dots and recognize the likelihood that the staff upgrades its forecasts for inflation. The last staff forecasts in March assumed the euro would average $1.23 this year and oil would average $65. The weaker euro and stronger oil prices point to upside pressure on measured inflation.

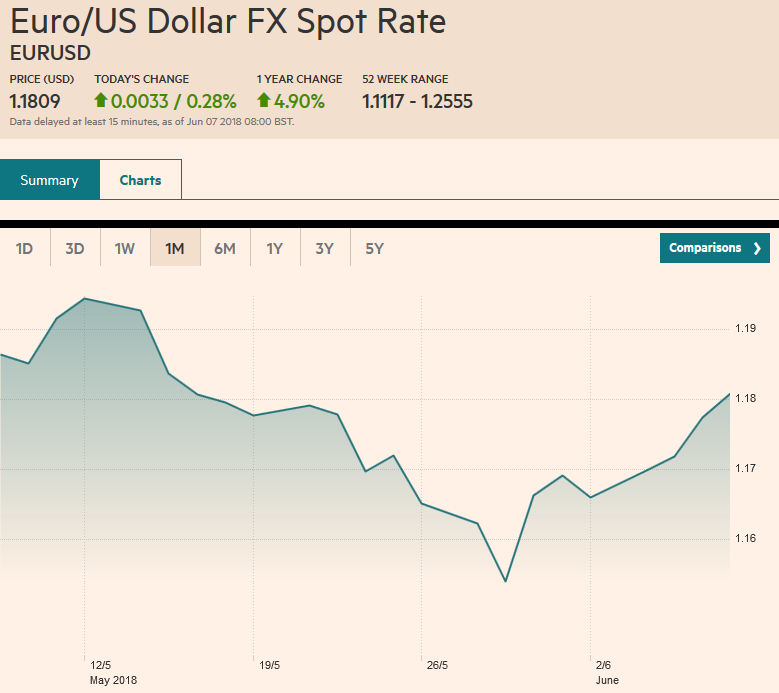

| Instead, let us offer a different interpretation. After a strong run over the past several weeks, the dollar’s technical indicators had been stretched, and some bearish divergences appeared. The two-year interest rate differential between the US and Germany peaked on May 21, suggesting that some of the fuel of the dollar’s rally was spent. We have also noted that in the futures market, speculators added to their gross longs for four of the past five weeks. The euro bulls made their stand ahead of $1.1500. Our reading of the technical condition suggested potential into the $1.1750-$1.1800 area.

The euro reached $1.1770 early in the European session. That is a ten-day high. The 20-day moving average, which the euro had not seen since April 20 is found near $1.1750 today. There is a $1.1760 option for 542 mln euros that will be cut in NY today, and 1.8 bln euros struck at $1.1800 that will also expire. The day before the ECB meets, the Federal Reserve will most likely raise interest rates and tweak the statement to recognize that it anticipates the need to raise rates past neutral. Also, the new Italian government’s clash with the EC has yet and begin in earnest. After what we see as a technical correction in the euro runs its course, we expect the downtrend to resume. |

EUR/USD, Jun 2018(see more posts on EUR/USD, ) - Click to enlarge |

Sterling caught a bid yesterday after the stronger services and composite PMI. It has extended those gains today. There is also an interest rate adjustment that has taken place. The implied yield of the December short-sterling futures contract has risen a dozen basis points since May 29. The market feels more comfortable with a BOE rate hike in Q3. We had been looking for a corrective bounce into the $1.3400-$1.3430 area, and it reached the upper end of that target today. There is a GBP304 mln option struck at $1.3425 that expires today.

Japan reported disappointing April labor cash earnings, but the yen’s weakness seems to be more a function of cross activity and the appetite for risk. April cash earnings were 0.8% above year-ago levels. This is down much more than expected from the 2.1% pace seen in March, and adjusted for inflation, it is flat year-over-year.

The dollar had not traded above JPY110 since May 24. If the euro and sterling’s advance stalls, we suspect so will the dollar’s rise against the yen. There is a $361 mln option struck at JPY110.50, and another $502 mln struck at JPY110 that expire today.

Perhaps the risk appetite has been bolstered by favorable news stream that includes a stronger than expected Australian GDP and a generous add of liquidity by the PBOC. Australia reported Q1 GDP rose 1.0%, following an upward revision to 0.5% (from 0.4%) in Q4 17. The 3.1% year-over-year pace is the strongest since Q2 16, which itself was the best since Q3 2012. The Australian dollar has recouped yesterday’s losses and edged its highest level since April 23 (~$0.7675).

China announced last week that was liberalizing the collateral acceptable for its medium-term lending facility (MLF). Today it lent CNY463 bln, easily exceeding the nearly CNY300 bln that was maturing today. This is seen as confirmation that the PBOC is proceeding with the effort to encourage deleveraging at a very gradual pace.

Moving in a different direction, the Bank of India hiked its repo rate (6.25% form 6.00%) for the first time since 2014. It is responding to price pressures and external factors, chief among these identified by the central bank governor in an op-ed piece earlier this week in the Financial Times. He argued that the Fed should slow its pace of unwinding its balance sheet because between its tightening and the huge fiscal stimulus announced, that dollar liquidity is evaporating, putting more pressure on emerging market countries (i.e., India).

The irony lies in the fact that when the Fed was engaged in QE, the former governor of the Bank of India complained, and fanned the talk of currency wars. Now that the Fed is unwinding QE that too is subject to criticism. Fed Chief Powell, like his predecessor, pushes back at the idea that the US policy drives global capital flows. The US is a current account deficit country. It must import savings from other countries. Moreover, it is difficult to imagine a more transparent Fed policy. Though we advocate a press conference after every Fed meeting, it is more for operational flexibility than improved transparency.

Italian bonds are leading the European bond market sell-off. Italy’s new Prime Minister Conte was approved by the Senate via a confidence vote yesterday and is before the Chamber of Deputies today. While redenomination risk (i.e., Quitaly or simply exIT) appears to have lessened, the cost of the fiscal initiatives–sharp cut in taxes and a new transfer program–is estimated to cost around 125 bln euro. That alone could be expected to bolster Italian interest rates. Italy’s two-year yield is up 28 bp today to 1.29%. Last week it reached 2.80%. The 10-year yield is up 13 bp today at 2.93%. Last week it reached 3.44%.

Reports suggest US Treasury Secretary Mnuchin has urged President Trump to exempt Canada from the tariffs on steel and aluminum. However, given the President’s focus on the bilateral balances, and nearly half of the US steel imports come from Canada, an exemption seems unlikely, no matter how much the meaning of national security needs to be debased to consider it a threat. Still, this could be an inducement, if Trump’s’ druthers for bilateral agreements and may attempt to return NAFTA to its roots, which is a US-Canadian free-trade agreement. A year ago, Canada’s Trudeau seemed more willing to consider such a course than he appears to be now.

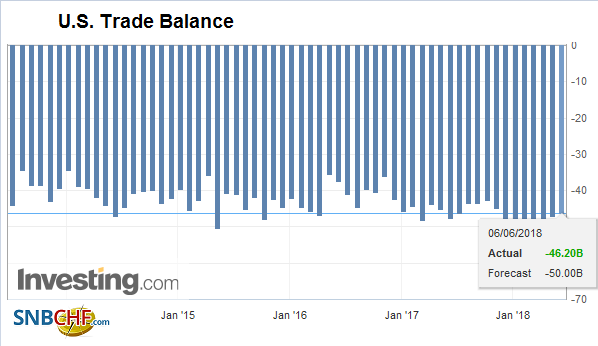

| The US reports the final productivity and unit labor costs for Q1. The revisions follow GDP and hence the risk that productivity is shaved to 0.6% from 0.7% and unit labor costs edged up to 2.8% from 2.7%. Unit labor costs, more than average hourly earnings and the employment cost index show a more complete picture by putting the wages/benefits in the context of output (productivity). The US also reports the April trade balance. In March it fell to $49 bln from $57.7 bln. The median forecast is for little change, though we suspect it may have risen on the back of growth differentials and stronger US consumption. |

U.S. Trade Balance, Apr 2018(see more posts on U.S. Trade Balance, ) - Click to enlarge |

Canada also reports its merchandise trade balance and building permits for April. The IVEY PMI for May is also on tap. Although the uncertainty around NAFTA continues, we continue to think a Bank of Canada rate hike as early as next month cannot be ruled out.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/USD,newslettersent,U.S. Trade Balance