Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

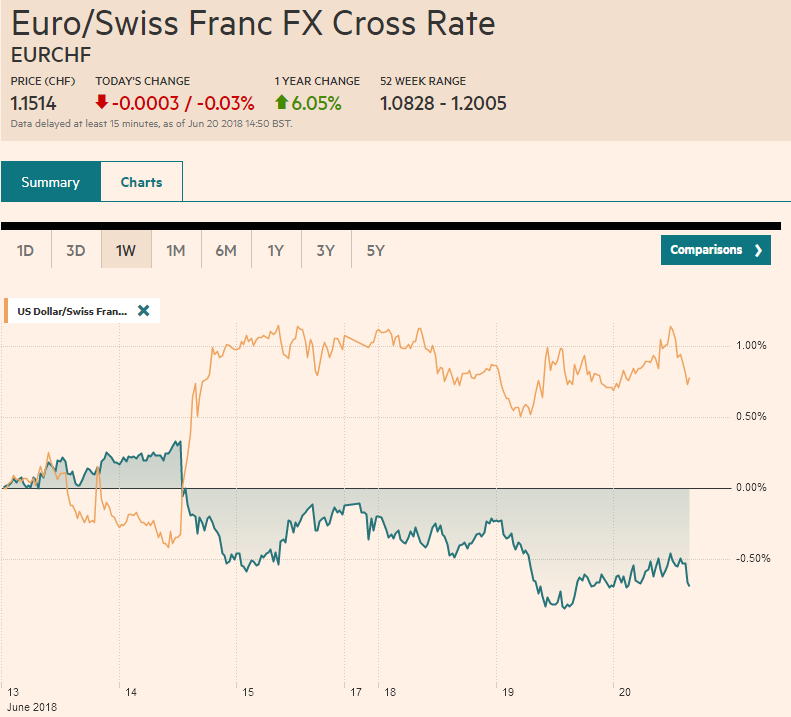

Swiss FrancThe Euro has fallen by 0.03% to 1.1514 CHF. |

EUR/CHF and USD/CHF, June 20(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe day began out with equity losses in Asia before a sharp recovery, perhaps initiated in China. The MSCI Asia Pacific Index was up a little more than 0.5%. The Shanghai Composite fell more than 1% before closing 0.25% better. Market talk suggests retail accounts followed the so-called national team of the large state-owned banks, following comments by PBOC Governor Yi Gang that some took as a hint that another cut in reserves requirement could be forthcoming shortly. Foreign investors returned to Korea for the first time in seven sessions. Foreign investors bought almost $241 mln of Korean shares today, after selling $1.43 bln since the start of last week. The KOSPI was up 1% while the KOSDAQ was up 3%. Foreign investors were not so keen about Taiwanese shares. They were net sellers for the sixth session. Over this period they sold $1.88 bln. The Philippines central bank hiked the overnight deposit rate by 25 bp to 3.0%, the second hike in the cycle. The equity market fell 0.7%. The positive tone carried into Europe, and the Dow Jones Stoxx 500 has recouped yesterday’s loss, rising 0.7% in the morning, led by materials and consumer staples. All industry sectors were moving higher. The news stream is light. The market is digesting Merkel and Macron’s proposals ahead of next week’s EU Summit While details are of course light at this stage, the general sense is that it provides for an evolutionary step toward greater integration, but falls short of the bold initiatives that Macron has previously presented. At the same time, it is clear that Merkel needs something from Europe to help defend her from a domestic challenge on asylum seekers. Merkel needs to take a tougher position on refugees and a more cooperative arrangement with Europe is essential. The challenge is that under EU rules the first country that registers an asylum seeker is responsible for their welfare. Geography dictates it is southern Europe–like Greece, Italy, and Malta, among the least that can afford it. |

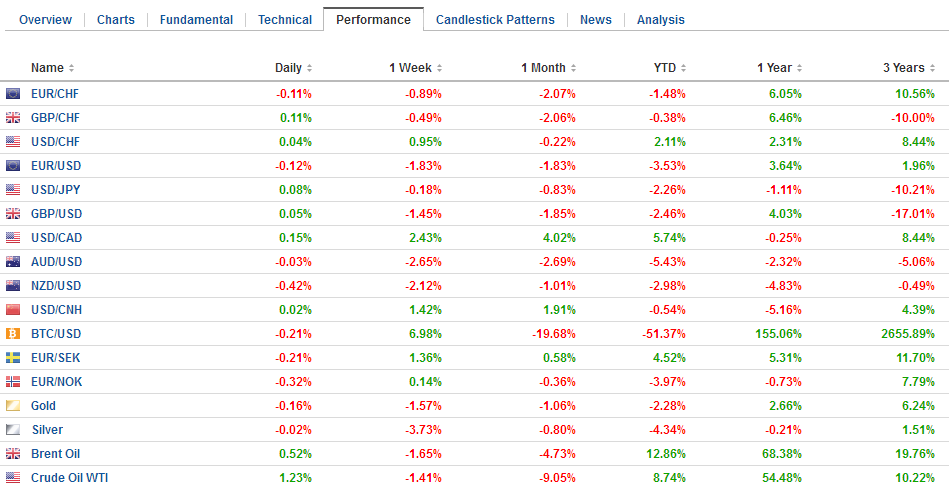

FX Performance, June 20 - Click to enlarge |

The ECB confab in Portugal draws interest today as the headline speakers include Draghi, Powell, Kuroda, and Lowe. Some think Draghi broke new ground last year and are especially attentive for a fresh tell. We suspect Draghi was as surprised by any by last year’s market reaction. Draghi just laid out the ECB course and pre-committed to not raising interest rates for another year. His caution, tempered by optimism in May, gave way to an optimism tempered by caution over the extended soft path.

The chief drama of the day is in the UK. Around the time of the US equity open, the House of Common is expected to begin voting on the Withdrawal Bill again. The key is the latest amendment by the House of Lords that gives parliament a “meaningful” vote on Brexit. This issue is partly over the terms of Brexit and partly a constitutional issue about the power of parliament. Even if May loses, it is not clear that the hardliners in the cabinet will challenge her. A palace coup would not resolve anything and could delay negotiations further.

After the summit, the next one is not until October, when ostensibly an agreement is necessary so it can go through the approval channels. Time is of the essence. The EC continues to complain that the UK is ill-prepared. Given the lack of substantial progress, the EC may urge members to step-up their contingency planning for a hard exit (no agreement).

The US economic calendar is light. It features Q1 current account and existing home sales. Existing home sales are expected to have recovered after the 2.5% fall in April. The current account deficit is expected to be little changed from the $128 bln deficit recorded in Q418. We share two observations. First, the TIC data shows the portfolio investment inflows of almost $131 bln covered the current account deficit. Second, the US current account deficit, driven by the trade balance, is most likely going to deteriorate. The fiscal stimulus runs counter to the more aggressive trade position of the Trump Administration.

Turning to the US stock market. There has been an interesting pattern in the S&P 500. For the past three sessions, the S&P 50 closed lower on the day but above the open. This leads to bullish candlestick formations. Yesterday the benchmark slipped below 2747.7, the 38.2% retracement of this month’s rally, but closed above it and on its highs. A gap higher opening is possible today, setting the stage for another attempt on 2800.

The dollar itself is little changed. The Australian dollar is the strongest of the majors, up a little less than 0.15% and the New Zealand dollar is the weakest, off 0.2%. The euro is consolidating in the lower half of yesterday’s range. So far it is the first session that the euro has not traded above $1.16. There are very large options expiring tomorrow: $1.1500-$1.1525 houses 2.5 bln euro options. $1.1550-$1.1600 holds another 2.5 bln euro, and at $1.1625 there are an additional 2 bln euros. The dollar continues to straddle the JPY110 level. There is a $540 mln option struck there that expires today and $600 mln at JPY110.45.

Sterling is lower for the third session. Today it has not been able to poke back through $1.32. On the other hand, it has only marginally penetrated $1.3150. Lastly, we note that the Canadian dollar is slipping to new lows for the year, with its fifth successive decline. The odds of a rate hike next month has eased, but remain the odds on the most likely scenario.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF and USD/CHF,newslettersent