– Sovereign wealth funds investing in gold for long term returns – PwC

– Gold has outperformed equities and bonds over the long term – PwC Research

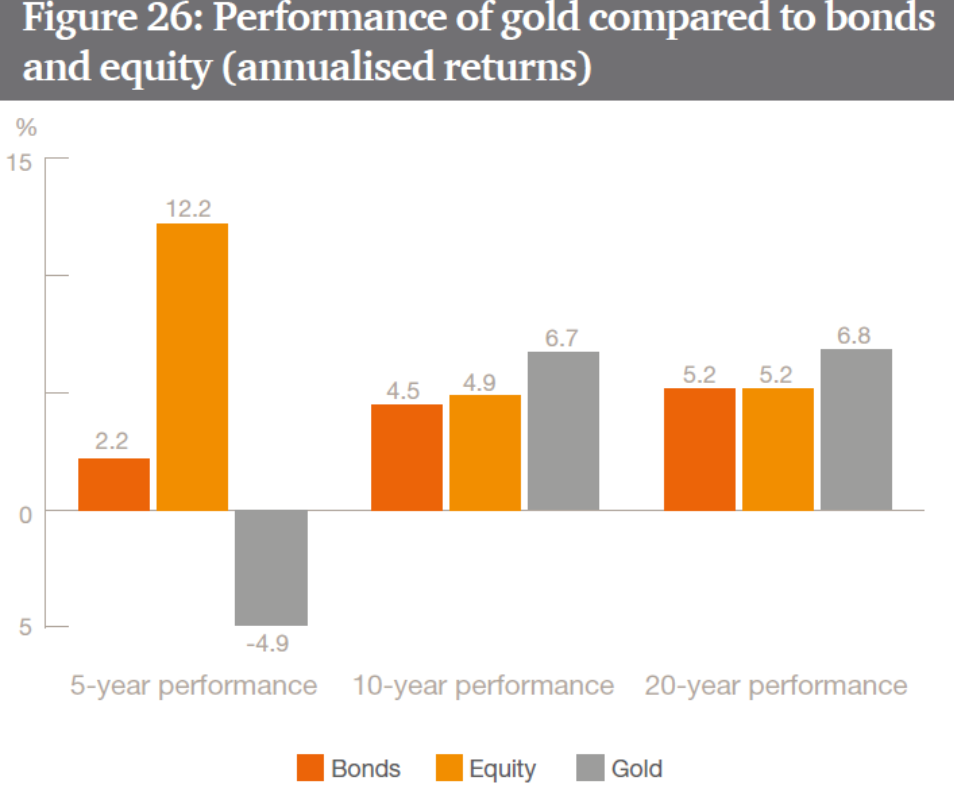

– Gold is up 6.7% and 6.8% per annum over 10 and 20 year periods; Stocks and bonds returned less than 5.2% respectively over same period (see PwC table)

– From 1971 to 2016 (45 years), “gold real returns were approximately 10% while inflation increased 4%”

– Gold also valuable due to lack of correlation and hedge against inflation, currency devaluation and uncertainty

– Sovereign wealth funds investing 23% of assets under management to alternative investments including gold

– Gold being diversified into by HNW, family offices, institutions, pensions, sovereign wealth funds and central banks

| In new research, entitled ‘The rising attractiveness of alternative asset classes for Sovereign Wealth Funds‘ PwC explain how gold is viewed as an important diversifier by sovereign wealth funds, as both an important hedge and for long term returns.

PwC now class gold as a ‘re-emerging asset class’ on the basis of its long-term out performance of stocks and bonds, low correlation with traditional assets, resilience and high liquidity. Gold along with private equity, real estate and infrastructure now accounts for 23% of a total $7.4 trillion of assets under management by sovereign wealth funds. The report notes that from a peak of 40% in 2013, sovereign wealth funds’ investment into fixed income instruments such as government bonds declined to 30% by 2016. Due to record low bond yields, the funds decided to turn their attention to alternative assets to enhance returns. The report notes the impressiveness of both gold’s long-term performance and low correlation to other assets in the long-term, compared to other alternatives. In the short-term the benefit of gold’s liquidity is noted: “[It] has one of the highest rates of daily volumes exchanged and can provide protection against short and medium term market corrections.” The 23% allocation is expected to increase going forward, despite slight increases in rates recently and because of the likelihood of continuing very low interest rates. This report comes at a time when we are seeing a growing interest by both large institutions and family offices in gold investment. Like sovereign wealth funds, they are encouraged by gold’s long-term returns, high liquidity and resilience against economic shocks. |

Performance of Gold Compared to Bonds and Equity Source: PwC Research via Bloomberg and WGC data - Click to enlarge |

Long term outperformance to traditional asset classes

As we have seen in recent years gold, like all assets, has periods when it underperforms. This has been in the short-term in the last 3 to 5 years, but in the long-term – such as a 10, 20 or 40 year period, it is an entirely different story.

Indeed, gold’s recent underperformance, makes its long term outperformance all the more impressive.

The report shows that in the last ten years, gold delivered returns of 6.7% per annum, outperforming equities and bonds which returned just 4.9% and 4.5% respectively. This return was slightly greater over a 20-year period when gold returned 6.8% per annum, compared to equities and bonds which returned just 5.2% and 5.2%.

Over the long term, gold is one of the top three performing assets along with real estate and private equity.

“Gold’s long-term performance is attributed to three factors: increased demand from emerging markets, central banks becoming net buyers, and the emergence of new products, such as gold-based ETFs, which have simplified investing and made the material more accessible.” – PwC

PwC also note the importance of gold when it comes to protecting against currency devaluation:

“By introducing alternatives into the portfolio, the value of investments can be protected against a possible decrease in purchasing power of the currency the investments are denominated in. This can be done through instruments whose returns are somehow linked to inflation or have perceived intrinsic value. Assets with perceived intrinsic value, such as commodities, should increase in price alongside CPI. In cases of extreme inflation for example, gold has historically performed well, outpacing that inflation by 10%…gold performed well during inflationary periods. For example, from 1971 to 2016, gold real returns were approximately 10% while inflation increased 4% year-over-year.”

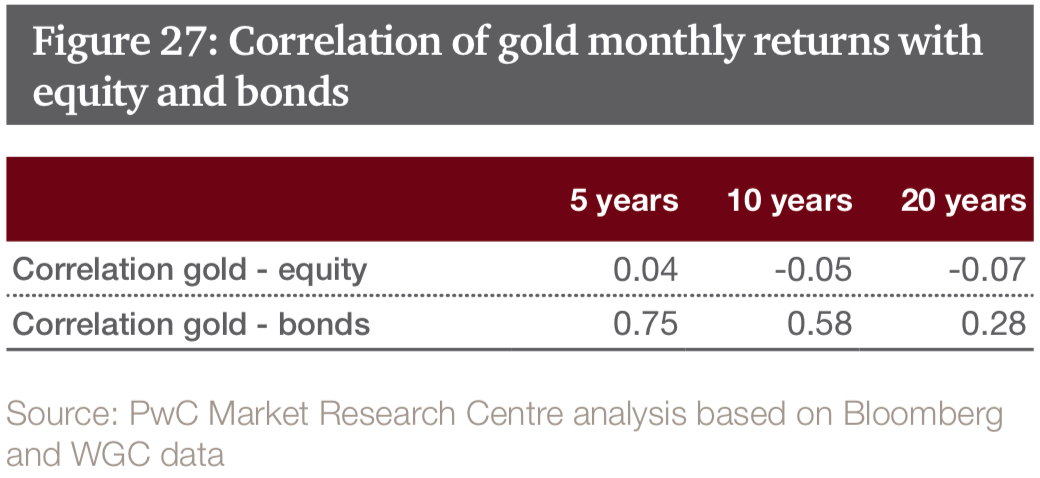

Gold doesn’t follow: Low correlation with traditional asset classes“Gold can be a useful addition to investment portfolios compared to other commodities, due to lower correlation with traditional asset classes. Between June 1997 and June 2017, the correlation between gold and equity returns was close to zero (-0.07), thus showing its diversification benefit. The asset class maintains only a negative correlation over a ten-year period as well, standing at -0.05. Gold is more correlated with bond returns, standing at 0.58 on a ten-year basis, and at 0.28 on a twenty-year correlation (see Figure 27)…Gold has, over all considered time periods, no statistically significant correlation with hedge funds, private equity, infrastructure, and real estate.” As with the other factors discussed by PwC this is pertinent for all considering investing in gold, from retail and pension investors, larger institutions and family offices. Much of gold’s low correlation is due to the fact that it is less affected by economic cycles and geo-political risks than other financial assets. This means it shows resilience at times when others are showing weakness. This has been seen in recent days when stock markets saw massive volatility and very sharp corrections and gold was essentially flat. Year to date in 2018, gold is nearly 1.7% higher while many stock indices are down sharply – Euro Stoxx 50 is down more than 4% year to date. |

Correlation of Gold with Equity and Bonds - Click to enlarge |

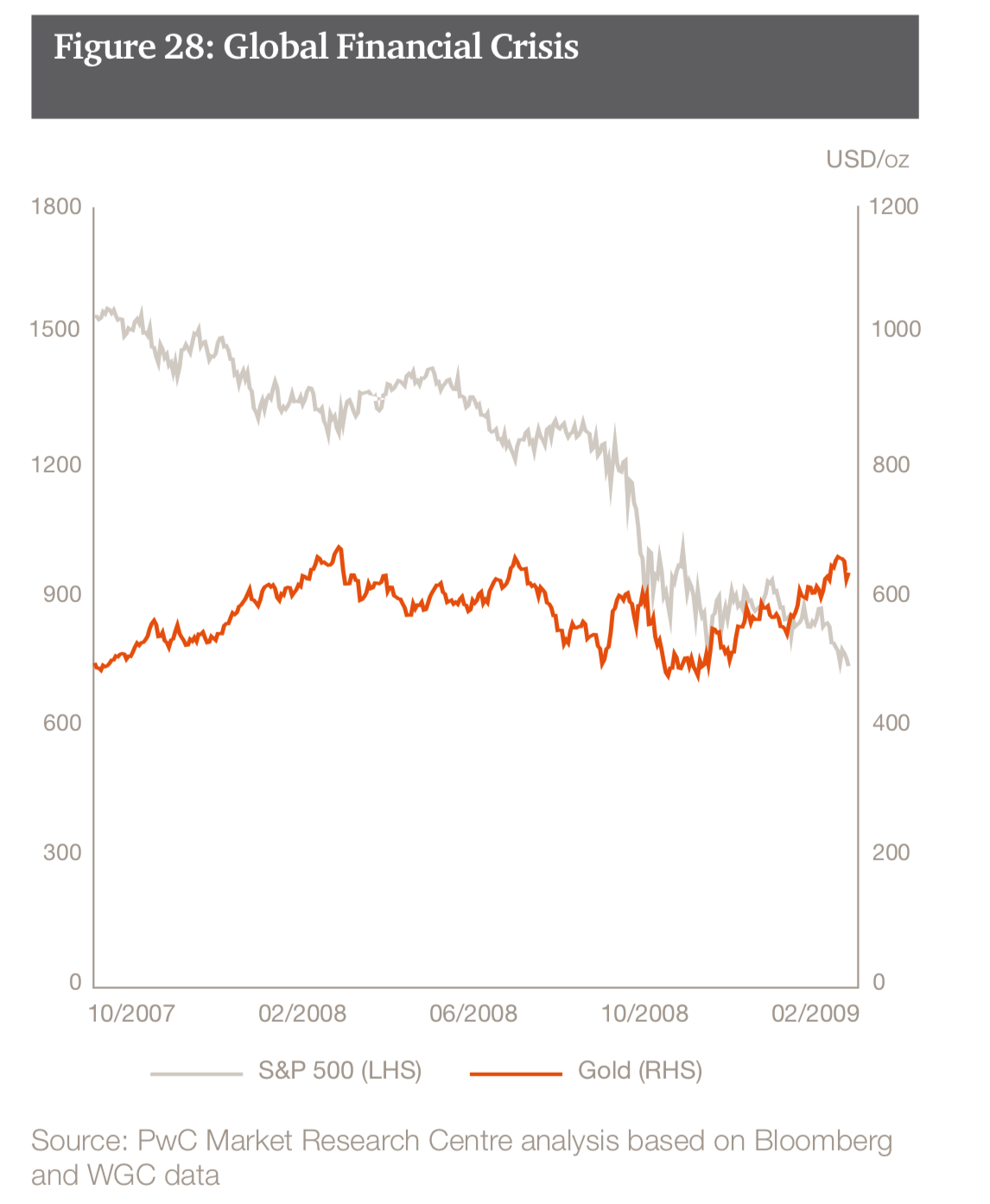

Resilient asset class during crises and instabilityThe gold price performs well in times of financial crises and extreme market events. During these times the correlation benefits become even more important, so it can provide portfolio insurance since it minimises portfolio losses. PwC explain that this is what distinguishes gold from other assets: “Gold has delivered negatively correlated returns when equity indices, such as S&P 500, have plummeted. Figure 28, 29, and 30 show gold’s performance during episodes of acute market crisis (GFC and the Sovereign Debt Crisis I and II). In these cases, the gold price started to rise significantly as the S&P 500 index decreased. Generally speaking, the gold price per ounce rose as investors perceived uncertainty in the stock markets, and decreased as these markets gave signs of normalisation.” |

Sovereign Debt Crisis, Jan 2010 - Nov 2011 - Click to enlarge |

| After the bloodbath of the last week, S&P500 investors will be interested to hear how gold correlates to the market”

“Among alternatives, when examining the correlation of returns with the S&P 500 index, gold is an excellent diversifier presenting the lowest correlation on a five-, ten-, and twenty- year basis (0.04, -0.05, -0.07 respectively).” |

S&P 500 and Gold Prices, Oct 2007 - Feb 2009 - Click to enlarge |

Liquid goldThe asset is particularly liquid in contrast to many of the other assets considered by SWFs, this is something very beneficial according to PwC: ” Stabilization funds may, in particular, benefit from adding gold among their holdings as they are required to hold highly liquid assets to counter the effects of sudden macroeconomic shocks. Gold has distinguished itself from other alternative asset classes as it has been more liquid, with USD 224 bn traded on average on a daily basis in 2016″. Conclusion: Investment and pension case for gold is strongPwC do not beat about the bush when it comes to their positivity towards gold as an investment. They synopsise and elucidate many of gold’s benefits which we have long been highlighting in recent years: “All these features suggest that gold as an investment class can offer reliable support, not only during uncertain market and political conditions, such as periods of high inflation, stock market crashes, and geopolitical instability, but also under normal market conditions.” They clearly see gold as playing a crucial role in the portfolios of sovereign wealth funds and indeed the majority of investors across the spectrum. “The investment case for gold, during periods of market uncertainty, has proven to be strong, with the price of gold having surged rapidly and having countered the negative effects of adverse market conditions. Hence, investors can consider gold for diversification and long-term performance.” |

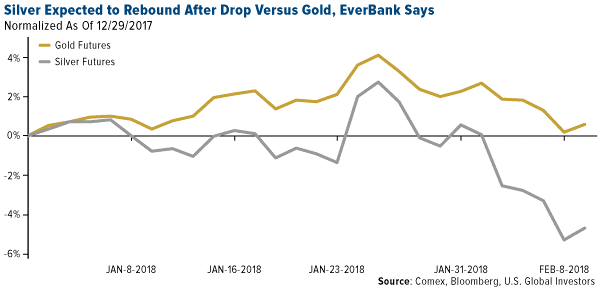

Gold and Silver Futures, Jan - Feb 2018 Source: Goldchartsrus via Goldseek - Click to enlarge |

Full story here Are you the author?

Tags: Daily Market Update,newslettersent