Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

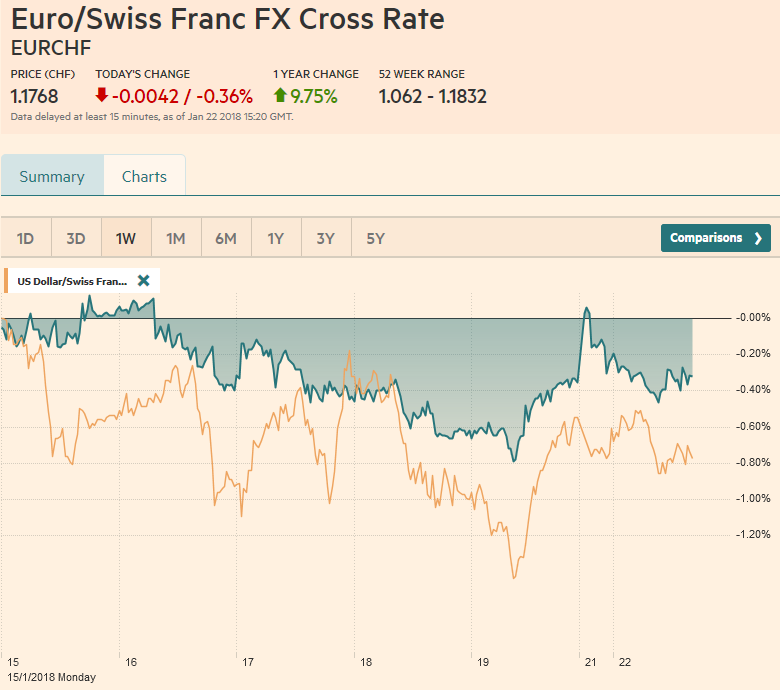

Swiss FrancThe Euro has fallen by 0.36% to 1.1768 CHF. |

EUR/CHF and USD/CHF, January 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar closed last week on a firm note, but it has been unable to build on its gains to start the new week. News that Germany’s SPD agreed to enter formal negotiations with Merkel’s CDU/CSU alliance saw the euro open in Asia around a half a cent higher. However, sellers emerged near $1.2275 but seemed to lose their nerve as the pre-weekend low near $1.2215 was approached. It requires a break of $1.2165 to be of technical importance. On the upside, the market may be reluctant to extend gains much above $1.2300 ahead of the ECB meeting later this week. The US government shutdown enters its third session. Half of the government shutdowns since 1977 have lasted three days or less. It is mostly about political theater and less about principles. It is a peculiar expression of the US presidential system and the idiosyncratic fiscal process. The direct economic impact of is thought to be minor, but of course, the more protracted the shutdown, the more disruptive. The next step may be a procedural vote in the Senate near midday. One impact of the government shutdown may be on the US economic data schedule. Fortunately, the week begins off with private sector data reports. However, reports later in the week, including the advanced look at durable goods orders and Q4 GDP could be postponed. For the record, the Atlanta Fed’s GDP tracker is looking at a 3.4% annualized paced, spurred by a 4% rise in real consumption. The New York Fed sees a 3.9% pace. Korean shares reacted to the MSCI warning about the capital gains changes being contemplated. The KOSPI and the KOSDAQ shed around 0.75% and bucked the regional advance. The MSCI Asia Pacific Index rose 0.15%. The Korean won is the weakest of the emerging market currencies with a 0.4% loss. Foreign investors were net sellers of Korean shares for the second consecutive session. The Taiwanese dollar briefly touched new five-year highs. The South African rand is the strongest of the emerging market currencies, gaining 1% against the US dollar and coming close to ZAR12.00. The ostensible impetus came from the ANC pressure on Zuma to step down. On the other hand, Turkey’s decision to pursue a ground offensive against US-support Kurds in Syria has spurred some modest lira losses (~0.20%). Following Fitch’s upgrade of Spain before the weekend, Spanish bonds are moving higher. The 2.5 bp decline in the 10-year yield, while core yields edged higher means that the Spanish premium continues to narrow against German Bunds. The premium is near 85 bp, the least since 2010. Greek bonds have not responded as favorably to the S&P upgrade, which was a catch-up move. Greek 10-year bond yields are up about two basis points. |

FX Daily Rates, January 22 - Click to enlarge |

| The Eurogroup of eurozone finance ministers meets today under the new head, Portugal’s Centeno. Two issues may draw the most attention. The first is the approval of a new tranche payment to Greece under its assistance program that is due to end in August. A decision on debt forgiveness, which is due after the completion of the current program, is unlikely to forthcoming yet. However, Greece is planning a bond offering soon as part of its preparation for the exit later this year.

The second issue is the start of the formal process to find a successor for ECB Vice President Constancio, whose term is up May. The selection of Centeno as the head of the Eurogroup begins a two-year process that is going to see a change in many European institutions including the EC and 2/3 of ECB. Spain’s de Guindos is seen as the likely leading candidate to be the next Vice President of the ECB. If de Guindos, or another candidate from the periphery, gets the nod, it would reinforce the understanding that Draghi’s replacement will come from a core creditor country. Germany is the obvious choice. It was ostensibly Germany’s turn after Trichet, but Weber quit in frustration over the ECB’s balance sheet. Weidmann is an obvious candidate, but it is not clear if he is a sufficient consensus builder. While the dollar is trading within the pre-weekend ranges against sterling and yen. However, against the yen, the greenback is straddling unchanged levels in early European turnover, while sterling has pushed back above $1.39. There are $1.1 bln in options struck at JPY110.70-JPY110.75 that expire in NY today and another $1.275 bln struck at $111.50-JPY111.60. The dollar-bloc currencies activity began slowly and gradually picked up. The shallow pullback has been seen as a new opportunity. Still, the pre-weekend high in the Australian dollar near $0.8040 seems distant. The US dollar traded above CAD1.25 but stopped shy just in front of last week’s high before sellers emerged. Retail sales and CPI from Canada are due later in the week and are the main economic reports this week. |

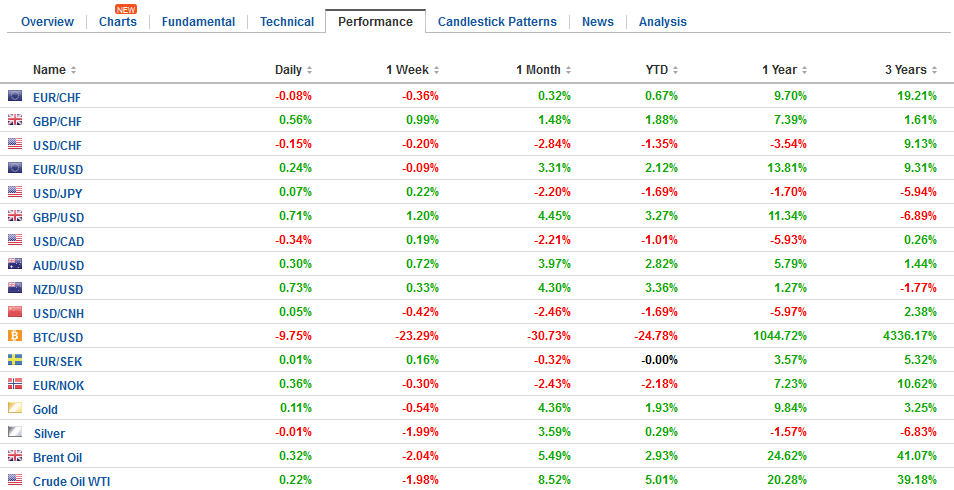

FX Performance, January 22 - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,newslettersent,USD/CHF