Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The investment climate is being shaped by two powerful forces. First is the very accommodative policy stance. This includes the United States, where despite delivering the fifth rate hike in the cycle, adjusted by headline CPI, remains negative. The balance sheet has begun being reduced, financial conditions in the US are easier now than a year ago.

The ECB’s bond purchase program, which has been cut in half to 30 bln euro a month starting now, is only the most visible part of its extraordinary monetary policy. Other elements include the minus 40 bp deposit rate, the full allotment of fixed rate refi operations, and the quality of the assets and collateral.

There are also roughly 750 bln euros of Targeted Long-Term Repos outstanding. Banks will begin to be able to pay back these borrowing early starting around mid-year. Given the absence of strong borrowing demand, and the negative rates at the ECB, it is not far-fetched to suspect that some banks will take advantage of the opportunity to return funds.

Even allowing for a conservative estimate that 10% is returned, it would offset 2.5 months of ECB buying in terms of the ECB’s balance sheet. It would be causing the ECB’s balance sheet to shrink at the same moment that officials will be considering what to do in September when the current program has a soft end date.

Around the same time, Greece may exit the multilateral assistance program. Some partial debt forgiveness will likely be debated again. This time Germany’s protagonist Schaeuble is the Speaker of Parliament rather than Finance Minister.

BOJ extraordinary policy remains intact. The shift to yield curve targeting, which meant capping the 10-year yield in a +/- 10 bp range around zero, alongside charging 10 bp for some deposits, ended up requiring fewer purchases of JGBs. It has a number of different lending facilities whose terms are also accommodative.

In addition to the accommodative monetary policy, fiscal policy is also supportive. The US just announced significant tax cuts even as the economy showed signs of accelerating. The first official read of Q4 GDP is due at the end of the month, and a three-handle would be the third consecutive such quarter, the longest streak since H2 2004 and Q1 2005. Even though it does not make it into the headlines often, the deregulation efforts by the federal government are significant. On top of this, an infrastructure initiative is expected to be unveiled shortly.

Overshadowed by the unprecedented monetary policy, Japan’s fiscal policy has also helped fuel the economic expansion. To be fair, the budget deficit has steadily, albeit slowly, fallen The 5% deficit in 2017, was the smallest since 2008. Japan’s budget deficit has averaged 6.7% over the past five years.

European fiscal policy is less supportive. Of the four largest EMU countries, only Spain had a deficit last year more than 3% of GDP. Deficits are projected to fall this year. Germany ran a budget surplus last year for the fourth consecutive year. The UK deficit appears to edged down last year from around 2.9% to 2.5% and is projected to remain near there this year.

The other major element of the global investment climate is the response by investors to the incentives partly created by the combination of monetary and fiscal policy. Equities are favored. The S&P 500 and NASDAQ posted their largest weekly gains in a little more than a year. Japan’s equities are levels not seen for a quarter of a century.

The MSCI Emerging Markets Index rose by a little more than 34% last year, the most since 2009. It extended the six-year high set last year with a nearly 3.7% advance last week. Brazil and Turkish benchmarks reached new record highs. Hong Kong’s market is at a 10-year high.

European shares lagged, measured in local currency terms. The Dow Jones Stoxx 600 rose 7.7% last year and rose 2.1% last week. German, Spanish, and Italian benchmarks all rose more than 3% last week.

For the past two years, the central banks have bought all the new government bonds issued by the G10. This year, they will buy around 40%. The private sector will make up the financing gap.

In the foreign exchange market, the dollar fell broadly from mid-April last year through early September, and then again in November, and the last two weeks of December. It fell further last week, but the sellers could not do much with the slightly disappointing headline optics and the distraction of a new book claiming to portray inside the Administration in an unflattering way. Technically, the dollar appears to be over-extended, and we anticipate that a consolidative or correction phase is near.

Speculative market positioning in the futures complicates the dollar-bearish consensus narrative. Speculators are net long the euro, sterling, the Canadian dollar, and the Mexican peso. They are net short the yen, Swiss franc, and the Australian and New Zealand dollars. To some extent then, the US dollar is at the fulcrum rather than on either side of the financial teeter-totter. And to the extent the US dollar structurally is widely used as a funding currency, it appears to have been joined by the yen and Swiss franc.

The economic data in the days ahead might not pose much more than brief headline rise. Data from Q4 does not matter much now. Or perhaps, more to the point, at the start of the of the New Year investors are especially looking forward, and the data is important only to the extent they provide some measure the economic and price momentum at the start of 2018.

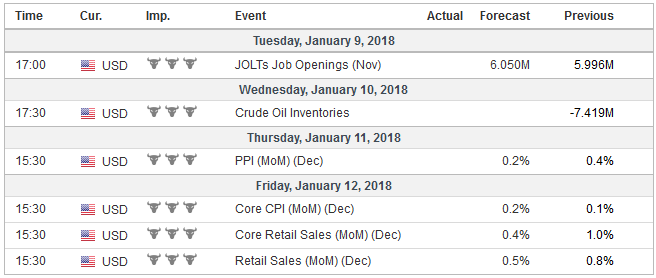

United StatesIn the US, the decline in gasoline prices in December (~3%) will dampen the headline CPI, while the core needs to rise 0.2% to keep the year-over-year pace steady at 1.7%. Some of the short-run factors that the Fed cited last year are beginning to fade and this is most evident in the service prices. At the same time, it will be difficult for December retail sales to match the outsized 0.8% rise in November (headline and “control” or GDP components). Nevertheless, real consumer spending is running 3% (annualized rate). In this context, it is noteworthy that consumer credit appears to have slowed in 2017 from 2016. Consider that the monthly average in 2016 was about $19 bln a month. In the first 10 months of 2017, it averaged about $15.7 bln. The November report will be released at the start of the week. If the pace does not pick up, it 2017 could be the slowest pace in the extension of consumer credit in three years. |

Economic Events: United States, Week January 08 - Click to enlarge |

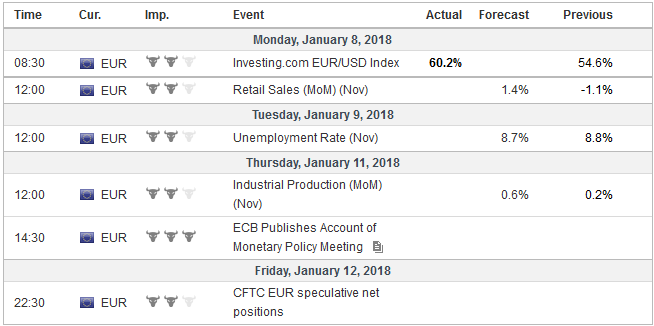

EurozoneThe eurozone reports employment, retail sales, and industrial production. The unemployment rate is gradually falling. It peaked at 12.1% in 2013. It finished 2016 at 9.6% and stood at 8.8% this past November. It is expected to have eased to 8.7%. It may finish this year near 8.0%. Retail sales are expected to fully recover from October’s 1.1% fall. Using averages to smooth out the volatility, we note that in 2016, retail sales rose on average 0.1% a month. This year through October, they have retained that average. Industrial production is expected to have risen 0.8% in November, but due to the base effect, the year-over-year pace will slow to 3.0% from 3.7%, which would be the slowest annual pace since June. |

Economic Events: Eurozone, Week January 08 - Click to enlarge |

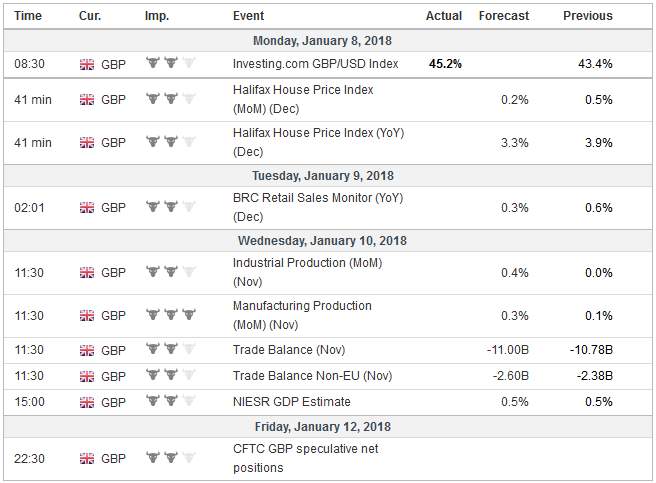

United KingdomThe UK reports industrial production, construction, and trade. Industrial output and construction appear to be slowing, while the trade balance improved markedly in 2017. The shortfall ran a little more than GBP3 bln a month in 2016 and 2017, through October, averaged a little less than GBP2.2 bln a month. Separately, political issues return. There is speculation of a cabinet reshuffle. Sterling will likely be sensitive to the perceived outcome in terms of hard or soft Brexit (with the latter seen as more supportive). |

Economic Events: United Kingdom, Week January 08 - Click to enlarge |

JapanThe markets are typically not particularly sensitive to Japan’s high frequency data, but the labor cash earnings at the start of the week may be interesting. Even though the headline may be unchanged at 0.6% in November, inflation is again rising faster. This results in real cash earnings likely falling again after rising slightly in the year to October. |

Economic Events: Japan, Week January 08 - Click to enlarge |

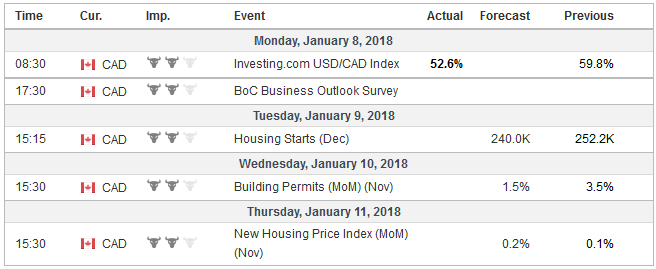

CanadaCanada reported another strong employment report before the weekend. The Canadian dollar was sent sharply higher as investors priced in a strong (82%) chance of a rate hike when the central bank meets next (January 17). Canada created more full-time jobs last year (394.2k) than in the past three years combined (363.8k). Although Canada’s housing data (December starts and November new house price index) may atract some attention, the central bank’s senior loan officer survey is more important. Another negative reading would be disappointing, and could dampen speculation about the rate hike and some Canadian dollar sales. |

Economic Events: Canada, Week January 08 - Click to enlarge |

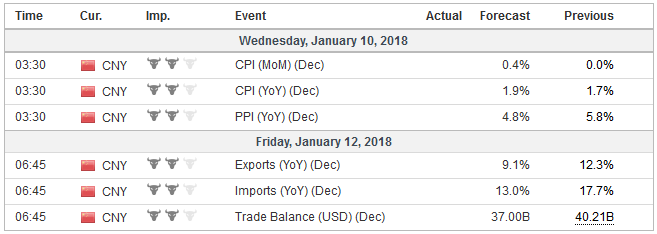

ChinaOver the weekend, China reported that its reserves jumped by $20.7 bln in December. It is the third largest monthly increase since April 2014, wand more than twice what the market had expected. China’s reserves have been rising since January 2017. They rose by $129 bln in last year, bolstered by the appreciation of non-dollar currencies and assets, and facilitated by the captial controls that discourage outflows. The US TIC data suggests Chinese buyers may have bought almost $131 bln of US Treasuries through October. China is due to report PPI and CPI in the coming days. The former is expected to slow to 4.8%, which would be the slowest in a year. The latter is expected to have risen to 1.9% from 1.7%. China’s year-over-year pace of CPI has been below 2% since February last year. |

Economic Events: China, Week January 08 - Click to enlarge |

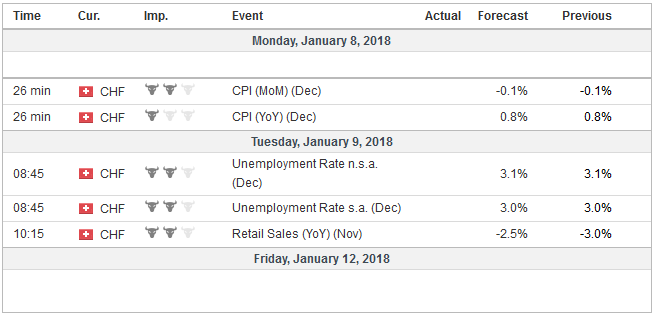

Switzerland |

Economic Events: Switzerland, Week January 08 - Click to enlarge |

Full story here Are you the author?

Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,newslettersent