Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

There seems to be a broad consensus on the trajectory of policy in the remaining weeks of the year. Barring a major shock or surprise the Federal Reserve will hike rates next month. The ECB’s course is set until at least the middle of next year when the current policy will begin to be debated in earnest.

The BOJ’s Kuroda has made it clear that the BOJ will continue to pursue Quantitative and Qualitative Easing (QQE) and Interest Rate Targeting as the inflation target continues to be pushed out in time. The Bank of England and the Bank of Canada previously raised interest rates but left little doubt in investors’ minds that there is no urgency to do so again in the coming months.

US interest rates (five years and beyond) bottomed on September 8. The 10-year yield is up 40 basis points since then, as is the 2-year yield. The rise in US yields completely accounts for the 37 bp increase in the two-year premium over Germany, which we find, despite the talk of new divergence, a good guide to the euro-dollar exchange rate. The US 10-year premium over Japan has widened nearly 35 bp over the same period.

The dollar bottomed against the euro, yen, Swiss franc and Canadian dollar on September 8 as well. Sterling is a notable exception. It bottomed at the start of the year. The Australian dollar’s low for the year, like sterling, was also set at the very start of the year. The New Zealand dollar by contrast, recorded its low in May and recently retested the level as investors (over?) reacted the change in the New Zealand government and policies, including changing the central bank’s remit.

The economic data scheduled for release in the coming days are unlikely to have policy implications. Or, to the extent that the data impacts expectations, it may simply reinforce existing views.

United StatesThe US data is likely to show an economy recovering from the impact of the storms, and the stability of price pressures somewhat above the troughs seen earlier this year. Both the St. Louis and NY Fed GDP trackers are estimating growth in Q4 at a little more than 3%. While the quarter is nearly half over, and there is much data still to come, the take away is this appears another quarter of above-trend growth. Headline October CPI may ease on softer gas prices, but the core rate is likely stable at 1.7% for the sixth consecutive month. Frankly, given the base effect, it may be difficult the year-over-year measure to head much higher over the next three months. Headline retail sales soared 1.6% in September as nature (storms), and rising prices conspired to flatter the data. However, a flattish report should be surprising in October. On the other hand, the GDP measure is expected to be a solid 0.3% after a 0.4% rise in September. Industrial output is expected to rise 0.5%, lead by a similar rise in manufacturing. |

Economic Events: United States, Week November 13 - Click to enlarge |

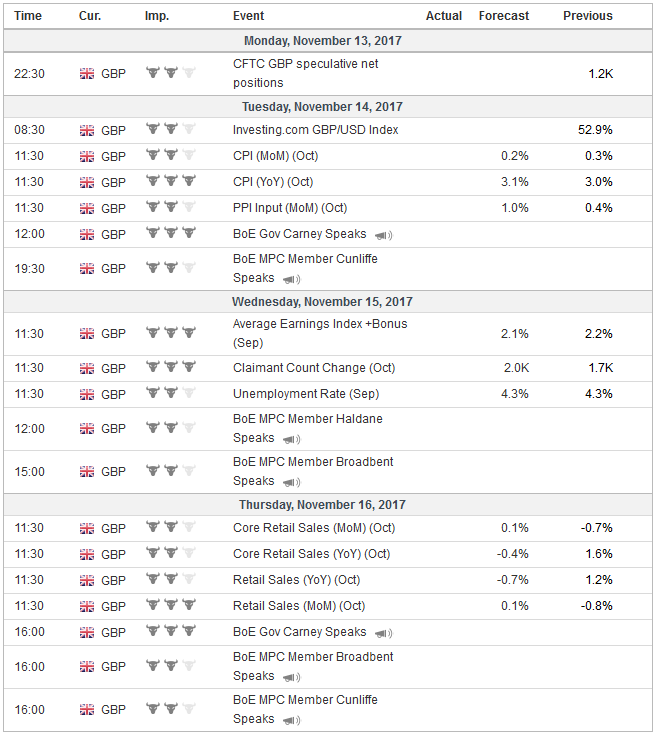

United KingdomThe UK reports inflation, employment and retail sales in the week ahead. Consumer prices may not have peaked yet in the UK, but they seem close. The quarterly inflation report released earlier this month suggested inflation will move above 3% in October and this will ostensibly lead to a letter from Carney to Hammond to explain. Yet, with a little luck, inflation would have already begun easing by the time the letter must be delivered. Although the UK enjoys what economists consider full employment, wage growth has failed to keep pace with inflation. Earnings are reported with an extra month lag from the employment data. Earnings growth, excluding bonuses, rose 2.4% in the three months (annualized) in September 2016, and is expected to have risen 2.2% in the three months (annualized) through September 2017. Meanwhile, consumer prices (CPIH) has risen from 1.3% in the year through September 2016 to 2.8% through September 2018. UK retail sales are expected to have stabilized after sharp falls in September. Excluding auto fuel, retail sales may be flat after a 0.7% decline in September. The year-over-year pace is likely to post its first contraction in 4 1/2 years. It may prove temporary as the base effect will be favorable over the next couple of months. However, the squeeze on household finances may not improve much until the spring. |

Economic Events: United Kingdom, Week November 13 - Click to enlarge |

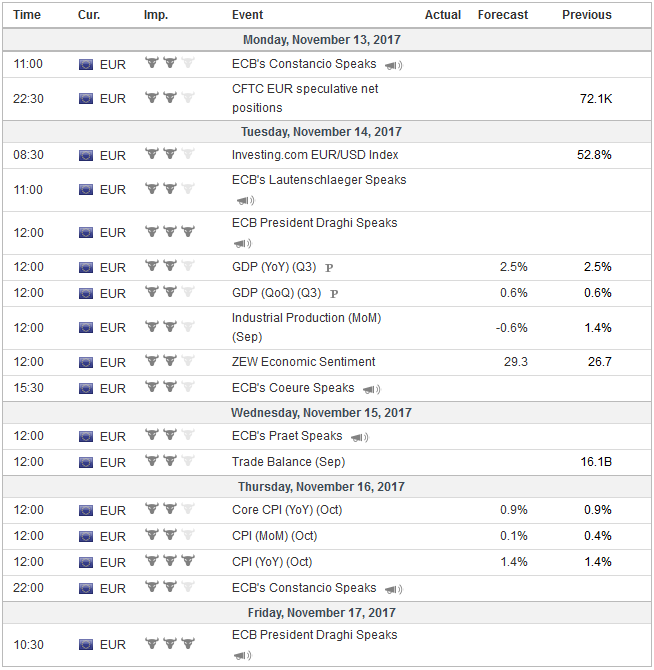

EurozoneFor the eurozone, investors will get more details about data that have already been reported, like the estimate for Q3 GDP and the flash CPI. The September industrial production data that are new are embedded in the GDP figures. The take away is that the eurozone economy continues to operate a strong pace. The unexpected drop in the core CPI (from 1.1% to 0.9%) may be explained by quirks that do not reflect the general price level, like holiday packages, and some administered prices. |

Economic Events: Eurozone, Week November 13 - Click to enlarge |

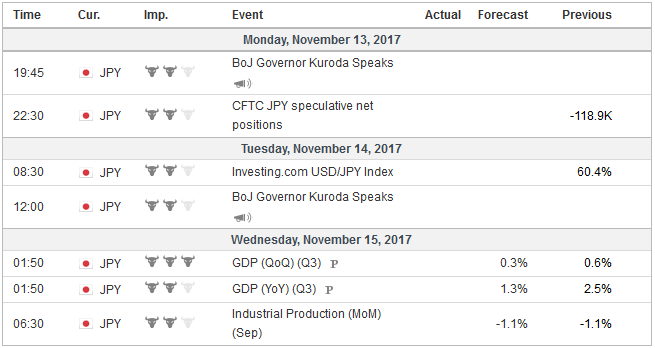

JapanJapan reports its first estimate of Q3 GDP. After a robust Q2 (2.5% annualized) the Japanese economy appears to have slowed considerably. However, the 1.5% median forecast in the Bloomberg survey would still be well above trend growth. The risk may be on the downside, with consumption and housing being a drag, partly blunted by export growth. Of note, the GDP deflator may turn positive, albeit barely, for the first time since Q2 2016. There are three political issues, which will likely shape the investment climate. The most important is US tax reform. Optimists still think a vote by both houses can be held by the middle of next month, ahead of the winter recess. We are skeptical, and the point we have made that is worth repeating is that, like health care reform, the key debate is not between the two main parties, but within the Republican Party. |

Economic Events: Japan, Week November 13 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week November 13 - Click to enlarge |

Despite months of leaders of both houses working with the Trump Administration, the bills are dramatically different on several key issues and note that the scoring still places the evolving House version more than the agreed-upon $1.5 trillion addition deficit over the next ten years. There are also conflicting incentives for House Republicans, who will face voters next year, that herald from states that Trump lost in 2016. It appears that prospects of fiscal reform a remote.

In Europe, the negotiations over the UK’s exit from the EU continue to be an important talking point. New wrinkles appear to have emerged, including the Irish border, that seems as intractable as any challenge of the divorce/amputation. There is speculation that Prime Minister May will shortly make a more detailed commitment of the sums the UK will pay to fulfill its obligations. This is in the hope that next month, the negotiations can turn to the post-separation relationship. It is by no means a done deal, and there is a certain pessimism that seems to be growing.

Lastly, we note the apparent progress in the formation of the next German government. It appears that the Merkel may soon concede the coveted finance ministry portfolio to its new coalition partner (likely the FDP). However, Merkel may strip the international (e.g., Europe) responsibilities from it and transfer them to the Economic Ministry. The Finance Minister’s remit would cover the domestic economy. The Economic Minister would attend the Eurogroup and G7 meetings, for example. Such considerations may be important as investors attempt to assess the policy implications of the new coalition government.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,$TLT,newslettersent