Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.16% to 1.1602 CHF. |

EUR/CHF and USD/CHF, October 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThis has been a good week for the US dollar. The Dollar Index’s 1.25% gain this week is the largest of the year. The driver is two-fold: positive developments in the US and negative developments abroad. The positive developments in the US include growing acceptance that the Fed will raise rates in December and that there will be more rate hikes next year. The Fed says three. The market now accepts at least one hike and has begun factoring in another. Also, the necessary steps toward tax reform have been taken. The first important step was the passage of the FY18 budget. The House passed the Senate version. The next step will come next week when the Chair of the House Ways and Means Committee releases his tax reform plan. It will then be marked up in committee. |

FX Daily Rates, October 27 - Click to enlarge |

| Meanwhile, the buzz is that it is down to Powell and Taylor for Fed appointments. We think there is a reasonable chance that both are appointed. In any event, our general view that in normal times, there is a large technocratic function rather the ideological. The chief difference may lie in how the individuals respond to a crisis. The FOMC meeting next week will be the first that the new governor Quarles participates. Reports of a longstanding personal rivalry between Quarles and Warsh may have hep explain why Warsh’s prospects have gradually dimmed. We estimate that fair value for the December Fed funds, assuming no chance of a hike next week, is 1.295%. The implied yield currently is 1.275%.

Sterling is the weakest of the majors today, sliding 0.5%, which is the bulk of its loss for the week (~0.7%). It fell to $1.3070 in the European morning, its lowest level since October 9. It trended lower but lagged behind the euro’s slide yesterday. The idea was that the prospects for a BOE rate hike next week was lending it support. That may still be true, but there was a bit of catch-up today. There is also recognition that the BOE rate hike is unlikely to be the start of a normalization cycle, but rather a one-off adjustment, taking back the post-referendum cut. |

FX Performance, October 27 - Click to enlarge |

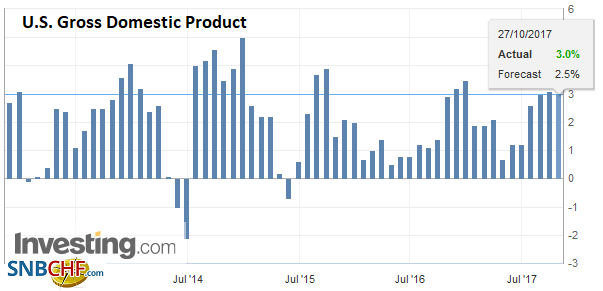

United StatesIn addition, the US economic data suggest it is borne the record storms and California fire fairly well. Corporate earnings have been strong. Today, the first look at Q3 GDP will be reported. It is unlikely to match the 3.1% annualized pace in Q2, but will still be well above trend which is seen a little below 2%. The composition of the growth may be a bit disappointing. It appears that consumption slowed but inventory growth accelerated. |

U.S. Gross Domestic Product (GDP) QoQ, Q3 2017(see more posts on U.S. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

| We sense that 1) investors may put more weight on GDP than the Fed and 2) officials may put more emphasis on real final domestic demand–excludes inventory and trade–as signals for the domestic growth impulses. |

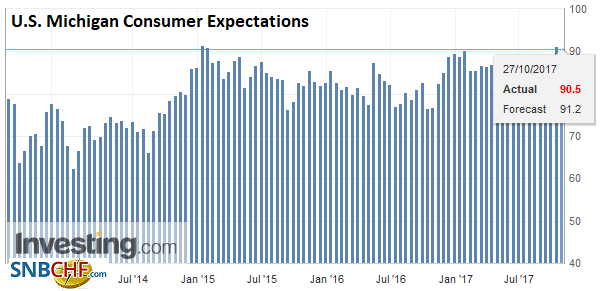

U.S. Michigan Consumer Expectations, Nov 2017(see more posts on U.S. Michigan Consumer Expectations, ) Source: Investing.com - Click to enlarge |

| Looking further afield, at the end of next week, the US will report October employment figure. Non-farm payrolls are expected to jump by more than 300k as they bounce back from a storm-inflicted decline in September. |

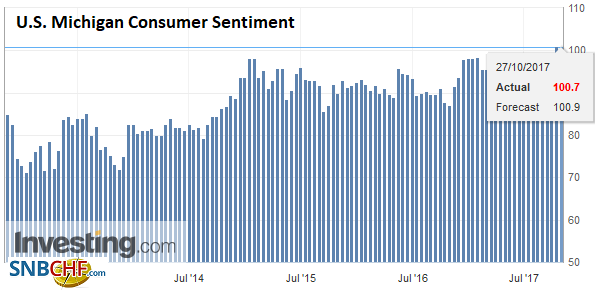

U.S. Michigan Consumer Sentiment, Nov 2017(see more posts on U.S. Michigan Consumer Sentiment, ) Source: Investing.con - Click to enlarge |

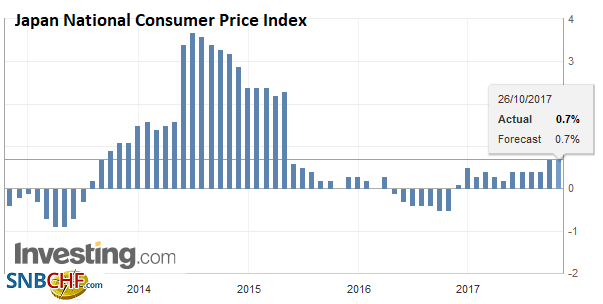

JapanJapan’s CPI was in line with expectations, with a 0.7% year-over-year increase in September, the same as in August. The core rate, which excludes fresh food, was identical. With the LDP victory last week, BOJ Kuroda’s chances of the second term appear to have risen according to surveys. The point is that as slow as the ECB’s exit strategy may be, the BOJ’s is even slower. We would say the same thing about the Swiss National Bank: it is a laggard. The US dollar is testing CHF1.00 for the first time in five months today, while the euro is consolidating its gains against the franc that carried it to the best levels since that fateful SNB decision in January 2015. |

Japan National Consumer Price Index (CPI) YoY, Sep 2017(see more posts on Japan National Consumer Price Index, ) Source: Investing.com - Click to enlarge |

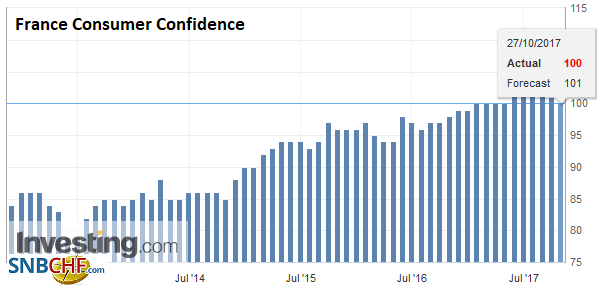

France |

France Consumer Confidence, Oct 2017(see more posts on France Consumer Confidence, ) Source: Investing.com - Click to enlarge |

Developments abroad also helped the dollar. The ECB’s open-ended asset purchases, with the forward guidance is encouraged the market to push further out the first rate hike. Draghi’s push back against tapering is not simply a game of semantics. The asset purchases are only one element of its extraordinary monetary policy. Other components include the full allotment of the fixed rate repo, the negative deposit rate, and the TLTROs. The only thing that is being adjusted is the asset purchases. Monetary policy is not being tapered. The asset purchase component is being re-scaled.

Divergence is very much intact. Starting this month, through September 2018, the ECB’s balance sheet will expand by 450 bln euros, while the Fed’s balance sheet will shrink by $300 bln. Conservatively, the Fed can raise interest rates say two to four times before the ECB goes once.

It seems like a cascading effect. Emerging market currencies turned. The dollar-bloc currencies followed. The majors are participating. The euro has held below the neckline at $1.1660 that was violated yesterday for the first time since late July. Bolstered by the rise in the US 10-year yield to seven-month highs has pushed the dollar above JPY114.00. The yen has held up the best among the majors against the dollar this week, partly perhaps as short yen cross positions, against euro, sterling and the dollar-bloc have been bought back as those currencies were liquidated.

There are a few new developments that are rivaling yesterday’s ECB meeting and US tax a prospects and Fed appointment speculation as talking points today. A court ruling disallows Australian’s Deputy Prime Minister from being a member of parliament due to his New Zealand citizenship when he was elected. This is important because the government had a one-seat majority in parliament, and that was it. The market may not have needed a new excuse to take the Aussie lower after the Q2 CPI disappointed earlier this week. A close below $0.7640, the 50% retracement of this year’s advance, would point toward $0.7530 as next target.

Spanish stocks and bonds are underperforming today as the Catalan-Madrid confrontation intensified. There was a movement toward having new regional elections as a way to avoid the implementation of Article 155. However, there may have been some tactical miscues, but there was no guarantee, apparently, and in any event, Puigdemont, after fanning the popular passions, was politically unable to back down. There seems to be a trilemma of sorts here. The solution to the crisis must be either on the regional level, with the secessionist backing down and perhaps being replaced, a crisis in Madrid, where the minority government collapses, which seems unlikely, or a constitutional crisis. The latter also seems unlikely at this juncture.

Graphs and additional information on Swiss Franc by the snbchf team.

Are you the author?Tags: EUR/CHF,France Consumer Confidence,Japan National Consumer Price Index,newslettersent,U.S. Gross Domestic Product,U.S. Michigan Consumer Expectations,U.S. Michigan Consumer Sentiment,USD/CHF