Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

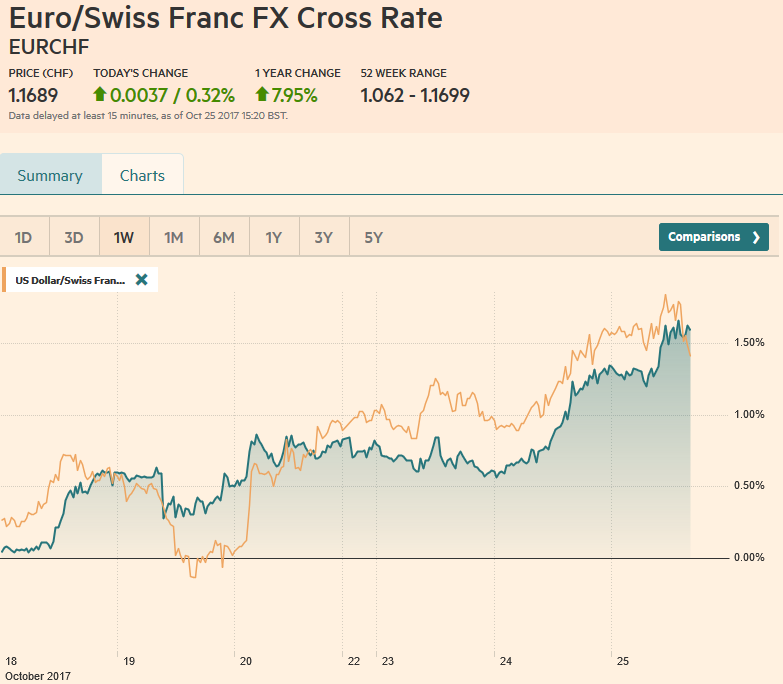

Swiss FrancThe Euro has risen by 0.32% to 1.1689 CHF. |

EUR/CHF and USD/CHF, October 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesMost participants seemed comfortable marking time ahead of tomorrow’s ECB meeting, and an announcement President Trump’s nominations to the Federal Reserve. However, softer than expected Australian Q3 CPI and a stronger than expected UK Q3 GDP injected fresh incentives. Australia reported headline CPI rose 0.6% in Q3. The market had been looking for a 0.8% increase. The year-over-year rate slipped to 1.8% from 1.9%. The Bloomberg median had forecast an increase to 2.0%. The trimmed mean and weighted median measures also eased. One of the important factors in the undershoot was electricity prices about 2/3 of what was expected. The Reserve Bank of Australia is on hold and today’s report simply underscores this fact. |

FX Daily Rates, October 25 - Click to enlarge |

| The Australian dollar was sold off immediately and was continuing to trend lower in Europe. It is set for its fourth consecutive declining session. It has only risen in one session, according to Bloomberg data since October 13. It is currently testing the $0.7700 area (the 200-day moving average is a few ticks below there), which it has not seen in three months. A break here targets $0.7630-$0.7645.

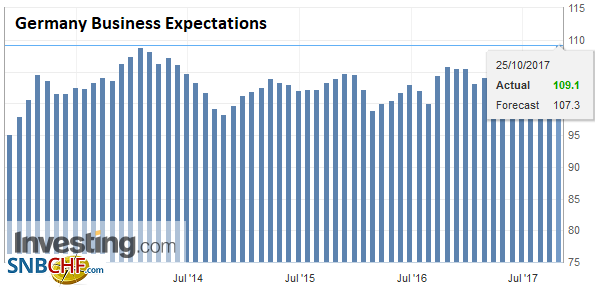

The US dollar is advancing against the Canadian dollar for the fifth consecutive session, and it is now at two-month highs near CAD1.2700. The low for the year was set in early September near CAD1.2060. The two-year rate differential is at 12 bp, a level which has not been seen for three months. The CAD1.2725 area corresponds to a retracement objective (38.2%) of the greenback’s decline since year’s high in May (just below CAD1.38). A move through there targets CAD1.29. The euro has been confined to less than a quarter cent range today. The stronger than expected German IFO series is not so surprising, except perhaps that it shows no concern about the changing coalition following last month’s election. The flash PMI already showed job creation and rising prices. The DAX is sitting near record highs set a week ago. It is up nearly 3.5% this month and 13.25% year-to-date. |

FX Performance, October 25 - Click to enlarge |

Germany |

Germany Business Expectations, Oct 2017(see more posts on Germany Business Expectations, ) Source: Investing.com - Click to enlarge |

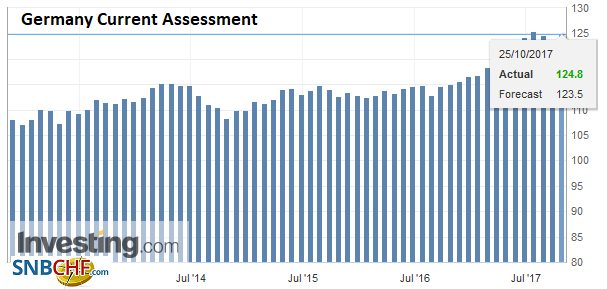

Germany Current Assessment, Oct 2017(see more posts on Germany Current Assessment, ) Source: Investing.com - Click to enlarge |

|

Germany Ifo Business Climate Index, Oct 2017(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

|

United Kingdom |

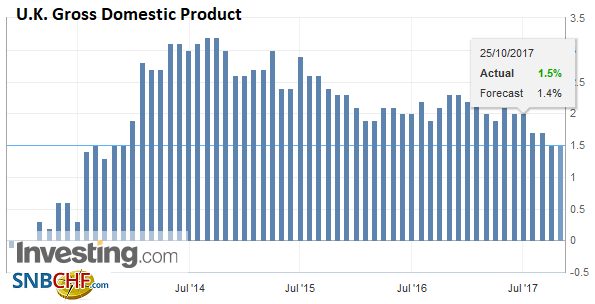

U.K. Gross Domestic Product (GDP) YoY, Q3 2017(see more posts on U.K. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

United States |

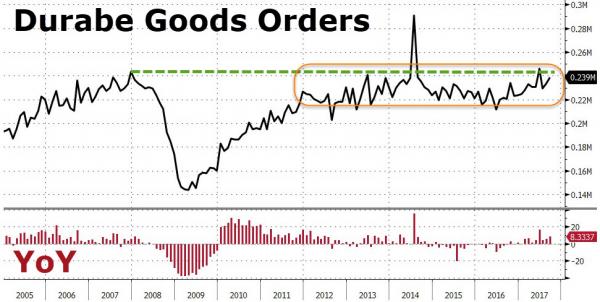

US Durable Goods Orders, 2005 - 2017(see more posts on U.S. Durable Goods Orders, ) Source: Investing.com - Click to enlarge |

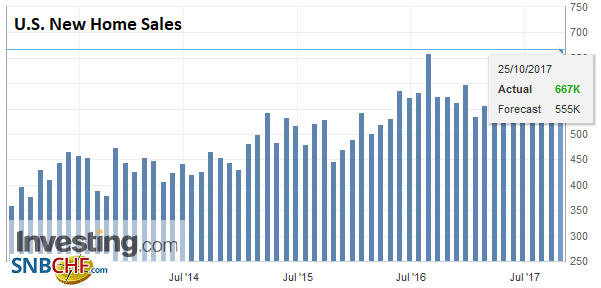

U.S. New Home Sales, Sep 2017(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

|

U.S. Crude Oil Inventories, Sep 2017(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

Separately, the New Zealand dollar remains under pressure. It also has only posted one advancing session since October 13. However, the driver here is the new government. We have just completed an unusual 12-month period in which all the G5 countries held national elections, and there has generally been a shift to the right. New Zealand appears to have shifted to the left with a Labour-led government. It will seek to hike the minimum wage and change the central bank’s mandate to include, as the US does, a full employment goal, alongside price stability.

However, the significance of these measures for global investors does not seem particularly salient, though some object to what they see is a return to demand management. We suspect such ideological considerations will lead to an overshoot. While we monitor prices for a reversal pattern, we see it moving toward the lower end of this year’s range (~$0.6800-$0.6845), with a break signaling $0.6675.

We note that both the Nikkei and the New Zealand stock market snapped a rally today with modest losses. The NZX 50 fell less than 0.1% to snap a 15-session advance that began on October 3. The Nikkei broke a 16-session rally with nearly a 0.5% pullback. The MSCI Asia Pacific Index was off fractionally for the second session and for the sixth time in the past seven sessions.

The Aussie and Kiwi are the weakest of the major currencies today. Sterling is the strongest. The stronger than expected Q3 GDP renews speculation, which had been softening, of a rate hike next week as part of Super Thursday, when the BOE inflation report will also be issued. Growth ticked up to 0.4% from 0.3% in Q2. The market had expected an unchanged pace. The year-over-year rate was steady though at 1.5%. The upward revision to July services, showing a smaller decline in services spending offsets the slightly softer than expected August services.

The case for a hike is clear. Growth in Q3 was a little better than the MPC expected, inflation is above target, and the unemployment rate is slightly below what the MPC sees as sustainable. The market (OIS), according to Bloomberg calculations has an 87% chance of a hike discounted. The case against a hike is that inflation appears poised to peak shortly, the economy is softening, real wages are falling, which may be already squeezing households, where an increase in the base rate quickly is passed through to households.

That said, a hike would likely be a one-off. Taking back the post-referendum rate cut is not the same thing as a sustained normalization cycle, such as the one the Federal Reserve is engaged. We would not be surprised to see sterling, that is bought on speculation of a hike is sold on the fact.

For today, sterling is bid, though it is trading within yesterday’s ranges. A move above $1.3230-$13240 is needed to lift the technical tone. The 20-day moving average is found a bit lower at $1.3220, and sterling has not traded above this average for three weeks.

The Bank of Canada meets today. Expectations that it would hike rates for a third consecutive meeting has faded with the combination of softer data and official comments. We are not persuaded that what Finance Minister Morneau called a “doubling down” of on its fiscal support challenges Bank of Canada policy, though Bank of Canada Governor Poloz has recognized the Child Benefit Program as helping boost consumption (close output gap?).

Widening interest rate differential should exert downward pressure on the single currency. The two-year differential now at 2.31%, the highest in nearly 20 years. The US 10-year premium is pushing toward 2.00% and is the highest in four months today. Many participants are concerned about a hawkish response to the ECB’s announcement tomorrow that is widely expected to re-scale (taper) its purchases while extending them well into next year (six-to-nine months). Because the market thinks it knows how much more assets the ECB can buy, without changing its self-imposed rules, many still see the euro appreciating.

Our concerns now are more with the US. The market may be getting ahead of itself on how much more hawkish the new Fed leadership (assuming Powell and Taylor) would be than the Yellen Fed. Also, the tension between President Trump and several senators seems to undermine the tax reform prospects. That said, the US 10-year yield is not only holding above 2.40% but is pushing through there (now nearly 2.45%). The rising rate differential may not be helping the dollar much against the euro, but it is helping lift the greenback against the yen. The dollar is approaching the July high near JPY114.50. Above there the March high beckons (JPY115.50).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Germany Business Expectations,Germany Current Assessment,Germany IFO Business Climate Index,Interest rates,newslettersent,NZD,U.K. Gross Domestic Product,U.S. Crude Oil Inventories,U.S. Durable Goods Orders,U.S. New Home Sales,USD/CHF