Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Over the past few weeks, the markets have come to accept the likelihood of a December Fed hike. US interest rates have adjusted. The pricing of December Fed funds futures contract is consistent with around an 80% chance of a hike. The two-year yield is trading at the upper end of what is expected to be the Fed funds target range at the end of the year, after slipping below the current range a month ago. The Dollar Index formed a bottoming pattern.

Paradoxically, therein lies the challenge. The anticipation of a hike is now well priced in, and the question is what. The Dollar Index has met the initial technical target. The 10-year yield is has moved into the upper end of its six-month range.

Where will the fuel come from for the next leg up for the dollar? One important source may come from a reassessment of US monetary policy. The critics complain that the Fed had anticipated a more aggressive pace of tightening than it delivered. But this old news. It is the echo of a cry from 2015 and 2016. The Fed will likely deliver three hikes this year as it had indicated, and the market had doubted. The issue is 2018.

With a Fed funds target range of 1.00% to 1.25%, the effective average rate is steady at 1.16%. The anticipated hike in December will likely lift the effective average to 1.41%. That means that a hike in 2018 would lift the effective average to 1.66%. The implied yield of the December 2018 Fed funds contract is 1.64%, suggesting the market remains profoundly skeptical of the three hikes that most Fed officials see as likely to be appropriate next year.

We fully accept that the September employment data was distorted by the storms. There is no reason to doubt that the underlying strength and improvement of the labor markets has ended. Nor do we think it has accelerated. While the headline was distorted to the downside by the most amount of people unable to go to work due to the weather in 20 years, the hourly earnings were flattered.

Workers in food and drinking establishments, mostly lower pay, were particularly hard hit by the storm. At the same time, there appears to have been an increased demand for some higher-paid professionals. However, we can be confident that the upward revision to the August hourly earnings to 2.7% from 2.5%, was not skewed. This is the strongest pace since 2009.

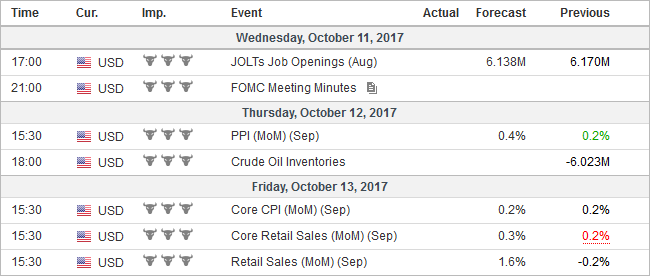

United StatesThe US data highlight from the week ahead will be the CPI and retail sales report on October 13. To be sure, the data will not be clean in the sense that some components will be distorted by the storms. The distortion will likely be on the upside. Gasoline prices surged, which will help flatter the headline, but there is more. The market for products, like household appliances and the like, that are necessities in the storm-ravaged areas, appear relatively tight in terms of inventory/sales ratios. That said, the transitory headwinds that some Fed officials had noted dampening inflation, are in fact subsiding. Also, related to this is the fact that the breadth has been increasing. Investors already know that US auto sales surged in September. This, and the rise in gasoline prices, will lift the headline, possibly by the most in a couple of years. The economic dynamics of what we discussed above will spill over and help accelerate the gains in the measure used for GDP purposes, which excludes, autos, gasoline, building materials. The average of this core measure of retail sales this year has been a 0.23%, identical to last year’s average. The median forecast in the Bloomberg survey is for a 0.4% increase after a 0.2% decline in August. The consensus narrative under-appreciates the importance of politics in driving the euro higher this year. Consider that through Q1, the dollar was consolidating its Q4 16 gains. It was not until it became clear that the populist-nationalist moment that supposedly connected Brexit with Trump was coming home to roost in Europe. The euro gapped higher on April 24; jumping above $1.08 not seeing it again. |

Economic Events: United States, Week October 09 - Click to enlarge |

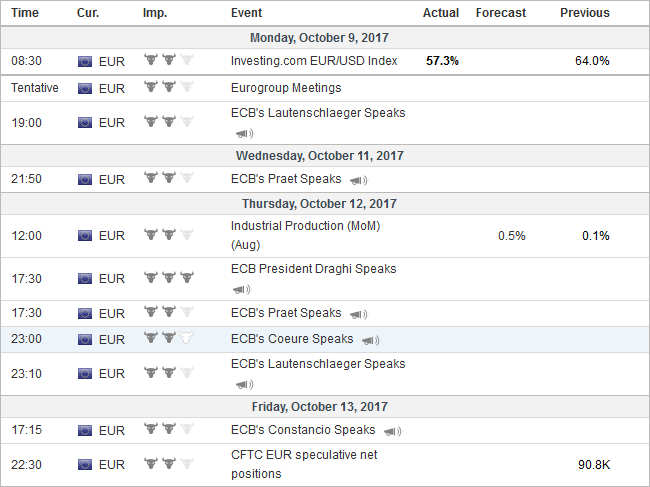

EurozoneIf Macron’s election marks the euro’s bottom, Merkel’s re-election help mark the top. The implications of the changed coalition, a new cabinet, including a new finance minister, are far from clear. The formal negotiations for the new government are just beginning, and it will likely take most of the rest of the year, if not longer, to reach an agreement. Merkel will also have to close ranks with the Bavaria-based CSU, which had considered running a candidate against her. The CSU and Merkel’s right-flank have been critical of her immigration policy as leaving them vulnerable to the AfD. The AfD drew their support heavily from the former eastern states that had less exposure to immigrants. At the same time, Spanish and UK politics are also impacting investors. The under performance of Spanish assets is clearly tied to the anxiety over Catalonia’s push for independence and Madrid’s response. The meeting of Catalonia’s regional government was supported to take place on October 9, but the meeting was suspended by the Spain’s Constitutional Court. The effect of the suspension is not clear. Presently, it almost feels like both Catalonia and Madrid are taking a collective deep breath and reconsidering the options. The Catalonia leaders may have bitten off more than they can chew. A declaration of independence, which they have given their followers reason to expect, but we a declaration of war. Madrid would have little choice to resist, which could take different forms, including the suspension of the local government. It could include occupying Catalonia and arresting the leaders as traitors. An independent Catalonia would be an economic challenge. Yes, it is true that Catalonia accounts for about a fifth of Spain’s economy. But severed from Spain, it would likely shrink. Press reports indicate that several companies, including banks, are or considering registering outside of Catalonia. As Montreal can tell Catalonia, even if secession does not take place, the mere threat can have far-reaching effects. There are many issues that may not have been thought out. Catalonia’s leaders have threatened to declare independence. What currency would they use? How would they service their debt? What is their responsibility for the federal debt? There are countless moving pieces, and they require time and institutional capacity. It is not the same as running a region. Catalonian officials have ultimately fanned unrealistic expectations, and there will be an economic and political price to pay. The ECB meeting is approaching. The market is expecting a slowing of the asset purchases and an extension through the end of H1 18. The ECB’s chief economist and board member, Praet suggested a trade-off between the length of the program and its duration. In the early phase, during a crisis, the size of the program is important, but later, the duration considerations eclipse it. That assessment would seem to suggest a compromise with some creditor interests by a larger cut in purchases than the 20 bln euros that the consensus had expected (we thought 30 bln cut would maximize the central bank’s options), and a longer run period (we had thought six months, but there is some talk now of a 12-month extension). |

Economic Events: Eurozone, Week October 09 - Click to enlarge |

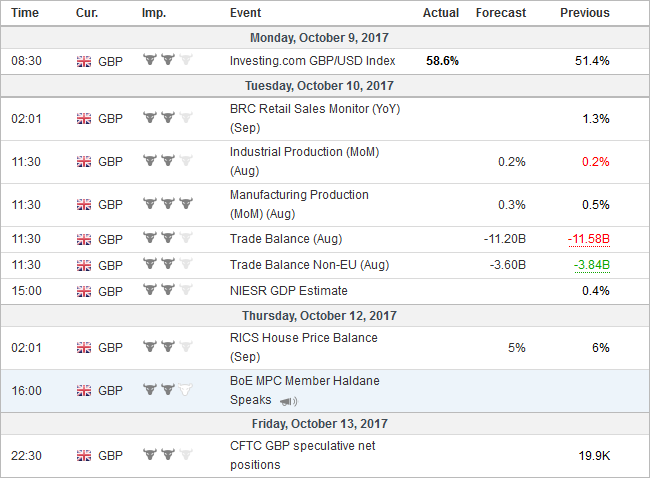

United KingdomUK Prime Minister May had a bad fortune in delivering a poor speech to the Conservative Party conference last week. Ignore a cough, the distracting falling letter of the backdrop, and the prank. Her two main proposals, boosting social housing spending and capping household energy bills, were lifted from the opposition. Since losing the Tory majority in the general election a few months ago, May has struggled to rebuild the confidence that had been shaken. Tory Party rules governing a leadership challenge have changed. Essentially, the rules require 15% of the Tory members of parliament ( or 48 MPs) to call for a leadership contest. Shapp, a former head of the Tory Party appears to comparable to “stalking horse” previously, and collecting the letters advocating a leadership challenge. Reports suggest he has around 30 such letters. There is no time limit for the other 18. Sterling has dropped six cents since September 20 to approach the psychologically important $1.30 level. There are two sources of vulnerability. First, the decline in sterling has not been accompanied by a shift in interest rate expectations. Drawing from the OIS, Bloomberg calculates a 76% chance of a hike in November and a nearly 80% chance of a hike before the end of the year. The implied yield on the December short-sterling futures contract slipped from 56 bp on September 20 and closed at 52 bp before the weekend. If the sterling’s first vulnerability is a downgrade of the perceptions of the likelihood of a BOE hike, the second is speculative market positioning. The CFTC latest reporting period covered through October 3. Over the five-session period ending on October 3, sterling fell two cents, but in the futures market, speculators reduced their gross short position by 20% or nearly 15k contracts. The net long speculative position rose to nearly 20k contracts, the largest in three years. |

Economic Events: United Kingdom, Week October 09 - Click to enlarge |

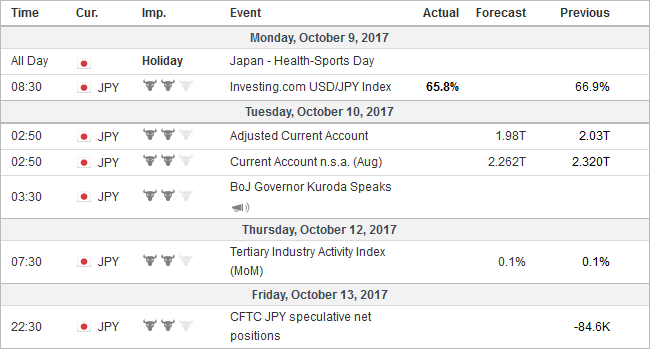

JapanLastly, polls suggest that the LDP will remain the largest party after the October 22 election. That would suggest that Abe will remain as Prime Minister. The Governor of Tokyo and head of the main opposition party now, the Party of Hope, Koike, has until Tuesday to decide if she will run for a parliamentary seat, which would give her standing to be Prime Minister. All indications suggest she will not abandon her newly elected position as Governor of Tokyo. In the context of Japanese politics, it also matters how many seats the LDP loses. If it loses more than 58 seats, it will lose its simple majority. This could set up a leadership challenge to Abe at the 2018 party conference. With little change in Abenomics, the yen seems to remain at the mercy of the US 10-year yield. |

Economic Events: Japan, Week October 09 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week October 09 - Click to enlarge |

Our broader point is that the fact that America elected an unorthodox president is well appreciated; what is not is the deterioration of European politics. Many narratives link the dollar’s weakness this year to Trump’s weak public support. This strikes us as exaggerated, and our expectation for a dollar recovery after bottoming a month ago is not predicated on a marked improvement in Trump’s support.

The Gallup Daily tracking poll shows that 39% approve of the job Trump is doing as President. He drew 46.4% of the popular vote last November. Consider that Merkel’s CDU/CSU coalition secured a little less than 33% of the popular vote in recent German elections. Recent polls see the UK Tories with public support of 39%. In the snap election in June, the Tories garnered almost 42.5% of the vote.

France’s Macron rounds out the three-M’s (Merkel, May, and Macon). The once-Socialist Economics Minister is pursuing a neo-liberal agenda of labor forms making it easier to hire and fire workers, public spending cuts, and tax cuts, and antagonizing various constituencies. Six months ago, he was elected with a 60 percentage point support. It was halved by late September, before recovering to 32% in early August.

Full story here Are you the author?

Tags: #GBP,#USD,$EUR,$JPY,$TLT,Angela Merkel,newslettersent,Politics