Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

In January 2016, just as the wave of “global turmoil” was cresting on domestic as well as foreign shores, retired Federal Reserve Chairman Ben Bernanke was giving a series of lectures for the IMF. His topic wasn’t really the so-called taper tantrum of 2013 but it really was. Even ideologically blinded economists like Bernanke could see how one might have followed the other; the roots of 2016 in 2013.

Though Janet Yellen declared it “transitory”, by early 2015 it was clear to most that there was something to this. Not even the “cleanest dirty shirt”, as the US economy was described, was going to just speed through it unscathed. After the events of that summer and their repeat later in the year, it seems pretty clear why Bernanke was lecturing on the topic to begin 2016. |

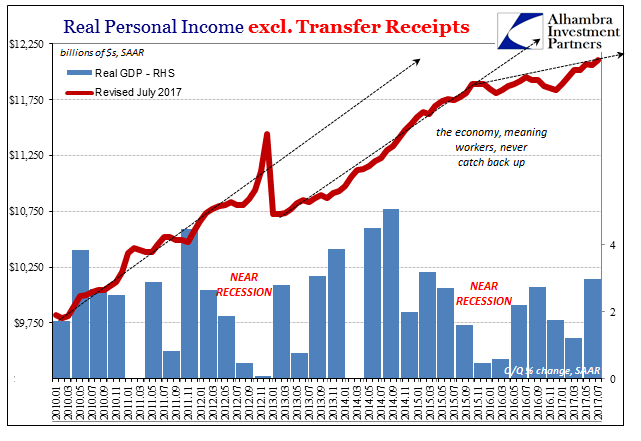

US Real Personal Income, Jan 2010 - Jul 2017(see more posts on real personal income excluding transfer receipts, ) - Click to enlarge |

Translation: “we” don’t really know what caused the mess, so don’t blame me. The first part was and remains especially true, but that actually doesn’t absolve the Fed from responsibility. It lies much deeper than in the taper tantrum of 2013. Even Bernanke had to concede there was surely a relationship that maybe fell within his former domain.

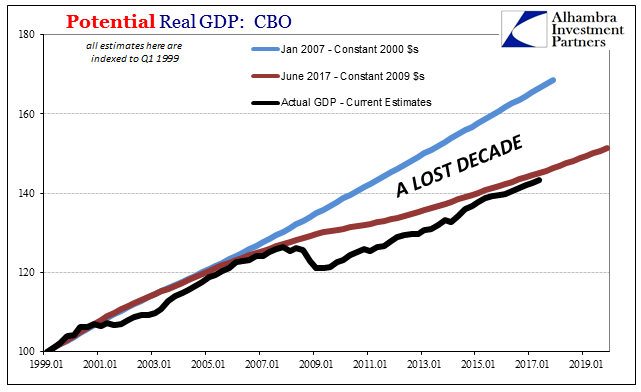

This is a fundamental problem, perhaps the fundamental problem of the last lost decade. After ten years, authorities who have every reason to know better are only recently catching up on the 1980’s (they’ll be blown away when they get to the nineties, whenever that might be). That was the small positive effect of the “rising dollar.” And it’s not like they can see clearly what has gone on all this time, it’s even one step further back as the events of 2014-16 merely opened their closed minds to the possibility of this “other” thing; the international nature of money and economy. The reason this is more than an academic exercise is equally obvious; it’s not over with yet. Since 2007, the global economy has been captured not by a single depressionary instant dragged out in time. It has experienced instead repeating cycles of variable monetary dysfunction. Nothing ever goes in a straight line, though the stretching of time to its current ridiculous proportions can make it seem that way; the events of 2011, for example, have blurred in memory with those of 2013 or 2009. |

US Potential Real GDP, Jan 1999 - 2019 - Click to enlarge |

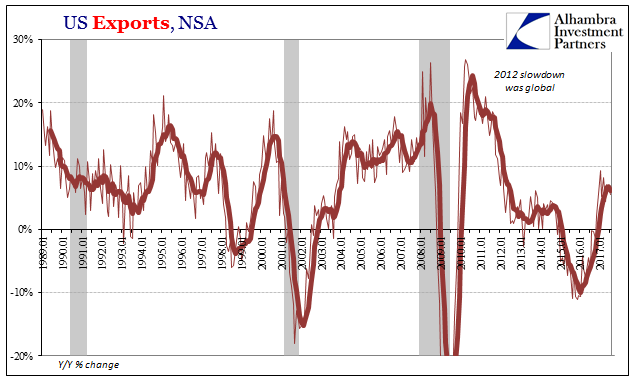

| The common factor behind it all has been the eurodollar system (using the term “eurodollar” I mean much more than just dollar deposits on account offshore; it is a more complete term adding in all the modern wholesale facets of what is really an non-reservable currency, where even the word currency is fabulously incomplete in this context). If the first episode (2007-09) was more so American experience trying to detach from it, and the second (2011) more so European, then the last so far (2014-16) was clearly Asian or EM more broadly.

The results of the “rising dollar” were felt most drastically in those places, only a near-recession here in the US but often chaos in and well beyond what Bernanke recognized as the fragile five. The point of contagion was global trade which only makes sense when factoring global money as the source of trouble. |

US Exports, Jan 1989 - 2017 - Click to enlarge |

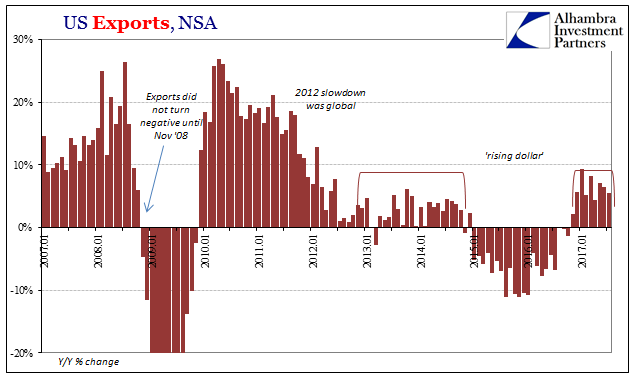

| Despite an abatement of those problems, global trade in 2017 remains suspiciously subdued. The Census Bureau reported today that US trade with the rest of the world has almost certainly repeated 2014 and in all likelihood will go no farther; and that is a bad sign for the world. Exports rose just 5.5% year-over-year, while US imports of foreign goods increased by a similar 5.6%. Though better than the string of minuses that forced Bernanke to finally talk about them, these pluses are nowhere near a sufficient advance to suggest a possible end to the whole thing. |

US Exports, Jan 2007 - 2017 - Click to enlarge |

| The oil price “reflation” of late last year has now almost completely faded, with imports nearly equalized with and without counting crude oil. |

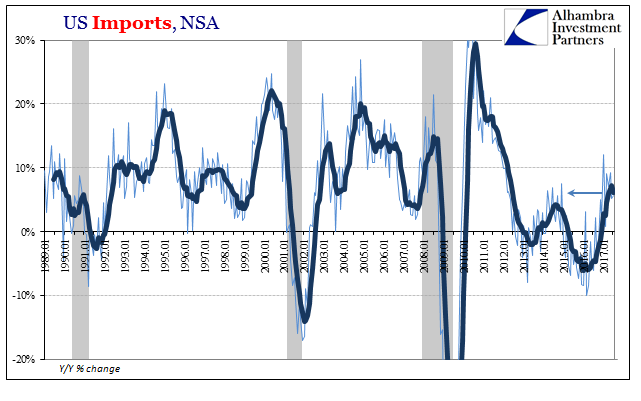

US Imports, Jan 1989 - 2017 - Click to enlarge |

| Ex-petroleum, however, you can more clearly see the lingering weakness in US demand for foreign products especially this year. |

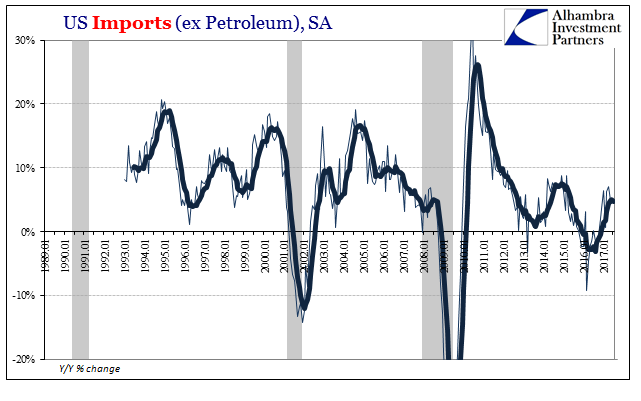

US Imports, Jan 1989 - 2017 - Click to enlarge |

| It is once again broadly based, meaning that the global economy is still in the same condition overall as when Bernanke declared taper more than four years ago. |

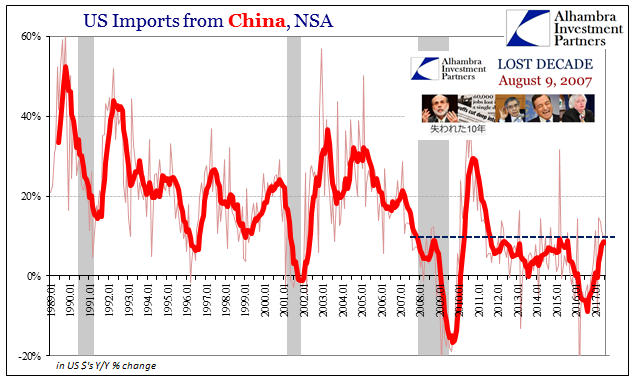

US Imports from China, Jan 1989 - 2017 - Click to enlarge |

| It wasn’t really his utterance of the word taper that did it so much as the fatal blow to the system in 2011 that produced the 2012 slowdown (and forced him reluctantly to QE3 and then QE4 first before he could taper anything). |

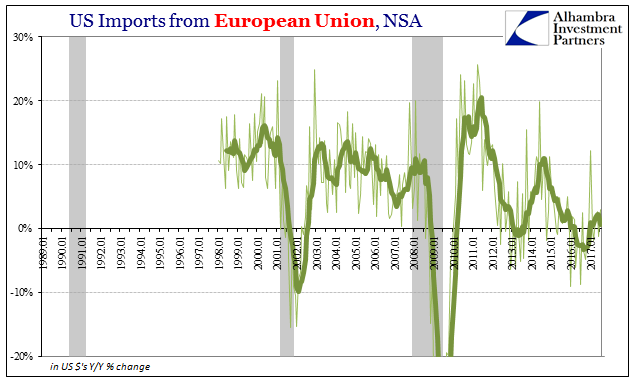

US Imports from European Union, Jan 1989 - 2017 - Click to enlarge |

| Where we are in 2017 is back facing (as noted yesterday) more and more the downside risks again. |

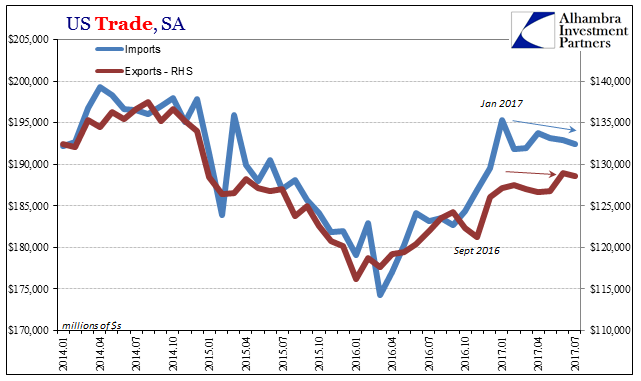

US Trade, Jan 2014 - 2017 - Click to enlarge |

| Whatever little economic momentum, as monetary momentum in “reflation”, was evident last year it almost certainly didn’t survive long into this one. |

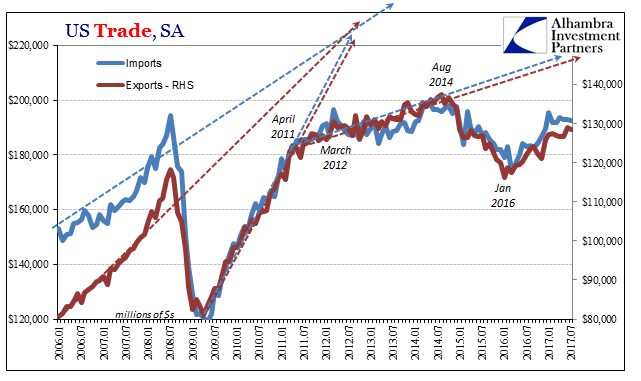

US Trade, Jan 2006 - 2017 - Click to enlarge |

| Seasonally-adjusted imports as well as exports show that beginning in January the trend changed, making it (possibly) the briefest upturn yet no matter how modest in total. |

US Trade, Jan 2014 - 2017 - Click to enlarge |

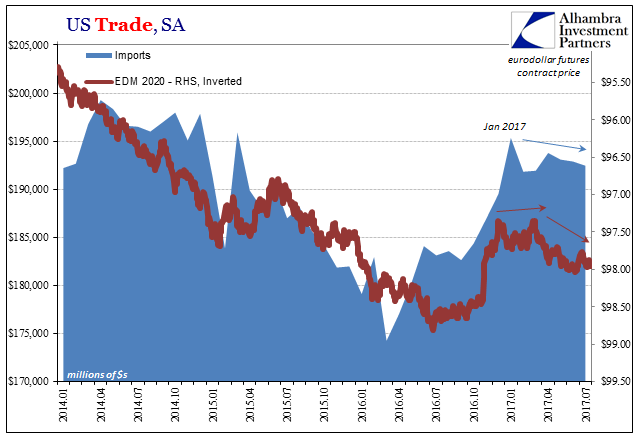

| For some, perhaps even Bernanke, they will see Fed “tightening” as the cause of 2017’s failure. The trade in eurodollar futures, however, should end any such notion (without ambiguity). The signal for monetary tightening indicated here is not at all consistent with “raising rates” as a matter of policy but instead as the all-too-familiar “consequences of the global financial cycle.”

Bernanke’s term is purposefully vague because he can’t say it (for now); there is right now no possible route from his position (consistent with the rest of orthodox Economics) to the eurodollar. He may not be able to admit it, but he doesn’t really have to. It’s right there behind all his words and his appeal to further investigation. As I wrote above, at some point he will discover the nineties and then the 21st century will start to make sense to him (and how embarrassing his “global savings glut” really was). The only question is how much damage, how large will the economic costs be when he and those like him finally get there? |

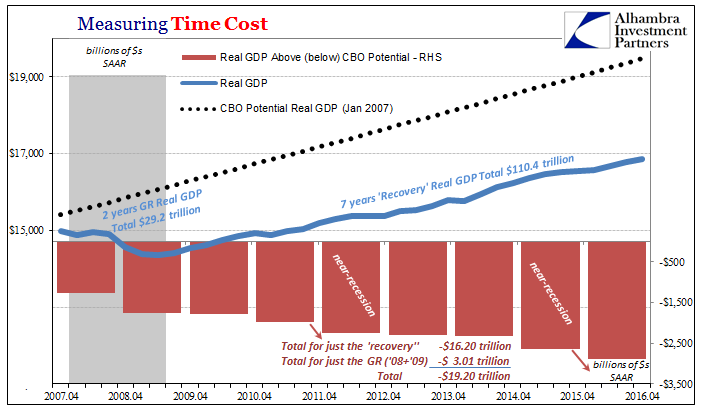

Measuring Time Cost, April 2007 - 2016 - Click to enlarge |

Tags: Ben Bernanke,currencies,economy,EuroDollar,eurodollar system,exports,Federal Reserve,Federal Reserve/Monetary Policy,global trade,imports,Markets,newslettersent,rate hikes,real personal income excluding transfer receipts,rising dollar,Trade Balance