Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Last week’s developments will continue to shape the investment climate in the week ahead, and at the same time, new inflation readings from the US, EMU, and Japan will add incrementally to investors’ information set.

We do not expect the results of the German election to have much market impact. The most likely result is a strong signal of continuity with a return of the Grand Coalition. At the same time, French President Macron’s speech next week is to herald a new post-Brexit, post-financial crisis, phase of the European Project, which a fourth-term Merkel may warm up to if Macron can truly reinvigorate the French economy and reduce its deficit and debt.

The New Zealand election is a different story. The status quo was challenged more than in Germany, and this political uncertainty may have held back the New Zealand dollar. The Nationals and its current ally looked two seats shy of a majority. This makes the New Zealand First Party a bit an of a kingmaker. It may take a couple of weeks to sort out things. The technical indicators remain constructive, especially against the Australian dollar. Perhaps, the election uncertainty or comments coming from the RBNZ meeting can knock the Kiwi back, offering a new opportunity.

It looks increasingly likely that Japan’s Prime Minister Abe will call for snap elections, probably slated for October 22, which is nearly a year early. It is a politically astute move. Public support had waned over various scandals and allegations, which may have contributed to the LDP’s stunning defeat in Tokyo elections a few months ago. Abe responded by a reshuffling of his cabinet, while the tensions with North Korea gave him an opportunity to lead. Support for Abe and the LDP has risen. Meanwhile, main opposition party, Democrat Party of Japan, is in disarray and divided. The election may be too soon for Tokyo Governor Koike to consolidate the new movement.

The likely re-election of Abe speaks to the continuity of policy, and this means Kuroda or at least Kuroda-esque policies. Kuroda’s term expires next year, and Japan’s tradition is for a governor to have a single term. Many suspect Kuroda could be reappointed, but are not particularly confident.

The broader issue is whether the next Governor is in line with an activist stance associated with Kuroda (whose name means black rice paddy) or a reversion back to the traditional stance represented by Kuroda’s predecessor Shirakawa (whose name means white river). This is also supported by the dissent from the BOJ’s decision not to change policy. It was a call to do more, unlike previous dissents, to do less.

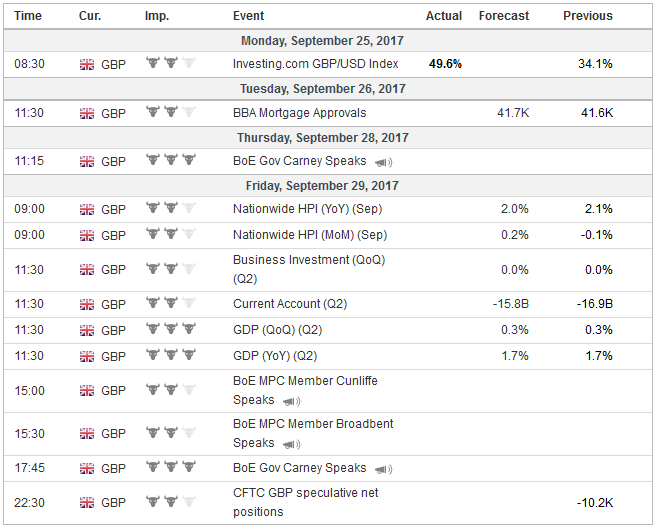

United KingdomUK optics are poor. The same day that Prime Minister May gave her most important speech on Brexit in a year, Moody’s cuts the UK’s sovereign rating. The substance of the developments was considerably better than what it appears. First, since the start of the year, Moody’s identified September 22 as the date that it would announce its rating review of the UK, which it had put on negative outlook following the referendum. Either May’s office was not aware of this, or it did not matter. The bad optics could have been avoided. Second, Moody’s downgrade is a catch-up move, not a leading move. That is to say, Moody’s new Aa2 rating simply brings it into line with the other two major rating agencies, S&P and Fitch, both of whom had cut the UK’s rating following the referendum. Moody’s only changed its outlook then. Both S&P and Fitch have negative outlooks on their UK ratings, while Moody’s credit cut was followed by a return to a stable outlook. May’s speech itself points in the other direction. It may not have been a major turning point, but May’s speech was a step forward. The evidence is that that is what the chief EU negotiator, Barnier, said (“constructive spirit”). It is important that the first step is followed up by another at the new round of negotiations that begin on September 25. The Tory Party Conference begins October 1. It could be harder for May than the negotiations with the EU. Sterling is consolidating the gains scored in the adjustment to the more hawkish than expected Bank of England. A shelf was carved last week near $1.3450. A break may signal another cent loss. Recall that the $1.3430 area corresponded to the 50% retracement of sterling’s decline since the referendum. With the convincing break, the next retracement objective is near $1.3800, and other technical levels come into play near $1.3880. On the other hand, the euro has carved out a shelf in the GBP0.8775 area as well, as the pullback from GBP0.9300 seen in late August runs out of steam. A move above GBP0.8900 is needed now to signal anything important. The euro needs to retake the GBP0.9100 area, but ideas the BOE could hike rates as early as November, while the ECB signals a gradual, cautious tapering next month (for 2018) may stand in its way. Madrid is stepping up its resistance to Catalonia’s planned referendum on October 1. The Supreme Court has ruled the referendum illegal. It appears that some local government funds were used to facilitate the referendum, a violation of the law. Madrid has offered some measures that would grant the region more financial independence. Spanish assets have under-performed Italian assets in recent weeks. A resolution may see a bit of catch-up. |

Economic Events: United Kingdom, Week September 25 - Click to enlarge |

United StatesIn the US, there are two important political tracks. The first is in Washington, where healthcare returns, as the Republican Party negotiates with itself and still appears to have fallen short of a solution. More broad details of tax reform are expected, but the harder questions, like offsets, are unlikely to be presented. It may be enough to fan the embers of hope but still fall short of providing much light. We suspect it is more a 2018 story than 2017. The second is the special Senator election in Alabama to fill Attorney General Session’s vacated seat. The contest will give some sense of the battle for the Republican Party, which could be as important as the 2018 midterm elections. Strange, who was appointed earlier this year, is running as the incumbent. He is running against Moore, who is supported by the Freedom Caucus. President Trump came out to support Strange, but he also expressed misgivings. A victory for Moore may demonstrate the vulnerability of the centrist Republicans associated with the party’s elite and intensify the challenge to incumbents in the primaries early next year. The Fed’s monetary decision is still being absorbed by investors. The market has moved to increase the likelihood of a December rate hike, and the two-year interest rate differential is the widest in six months, but the dollar has not much much traction. The euro briefly traded above $1.20 for the seventh time before the weekend. Important support is pegged in the $1.1800-$1.1825 area. A convincing break could open the door to a two-cent move initially. However, on balance, the technical indicators suggest another run to the highs (or toward the 50% retracement target of the decline since mid-2014 that is found near $1.2165). The US 10-year yield neared 2.0% earlier this month and moved to almost 2.30% last week. It may struggle to rise much further. The December note futures contract appears to have carved a bottom ahead of 125-16 after peaking near 127-28 (September 8). Initial resistance is seen in the 126-05 to 126-10 band. For its part, the two-year note yield set a new nine-year high last week of almost 1.45%. The yield still seems low considering that the Fed currently pays 1.25% on all reserves, and the next hike will lift it to 1.5%. Of the 16 current Fed officials (regional presidents plus governors), 12 will speak in the week ahead. Not all will address monetary policy or inflation. The highlight is Yellen’s speech on September 26, which will, in fact, discuss monetary policy, uncertainty, and inflation. The market may put less emphasis in a known hawk, like George, or dove-like Kashkari, staying true to form than if there is a change in views. In the week ahead, the US, EMU, and Japan will provide inflation updates. The US reports the August reading of the Fed’s preferred measure the core PCE deflator on September 29. If the median forecast of 0.2% materializes, it would be the largest monthly increase since January. However, due to the base effect, it is not enough to lift the year-over-year rate from 1.4%. In our view, which is informed by the July FOMC minutes and comments by the Fed’s leadership, there is greater emphasis on financial conditions that blunt part of the implication of the softer inflation figures in shaping the policy debate. The US and EMU preferred inflation measures are not expected to show much movement, but Japan’s may be a different story. Inflation is slowly rising in Japan. The BOJ targets the core rate, which excludes fresh food from the headline. It has steadily, albeit slowly, rising this year. It finished last year at minus 0.2%. It stood at 0.5% in July and is expected to have risen to 0.7% in August. The headline rate is also expected to have risen to 0.7% (from 0.4%). The firmer price pressures, coupled with stronger domestic consumption (look for a strong household spending report) and foreign demand (18% year-over-year increase in August exports), puts the world’s third-largest economy in a sweet spot that has been so elusive. If anything, a snap election may bring forward some new spending initiatives (though the real new spending may be limited). That is the fiscal arrow of Abenomics. |

Economic Events: United States, Week September 25 - Click to enlarge |

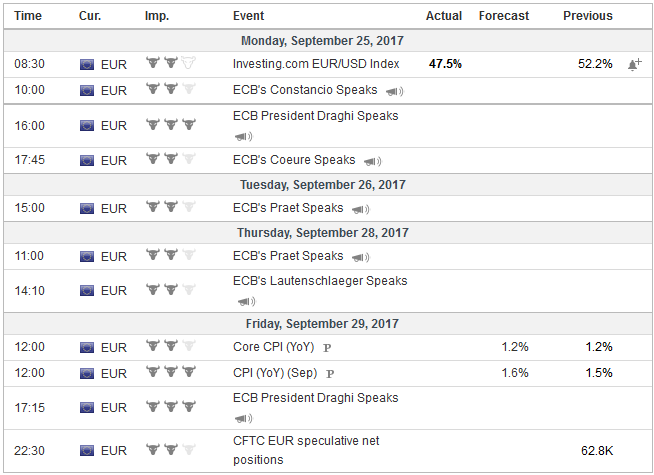

EurozoneThe euro may not be as sensitive to the interest rate differential has it has been, but the dollar-yen rate remains particularly sensitive. The 60-day correlation between the percent change in the 10-year US yield and dollar-yen remains near 0.80. Historically it rarely gets higher. The 30-day correlation is nearer 0.85. The eurozone provides a preliminary estimate of September consumer inflation. The headline rate is expected to have risen to 1.6% from 1.5%. It finished last year at 1.1%. The core rate is expected to be unchanged for the third month at 1.2%. It finished last year at 0.9%. In many ways, the debate about what the ECB does going forward has been decoupled by the short-term vagaries of CPI. Without knowing specifics, investors do know a few things. First, the asset purchases will not stop suddenly. That means the asset purchases will continue into 2018. Second, the first reduction was from 80 bln to 60 bln, many are thinking regarding bln of euros rather than in percentage terms. A reduction of another 20 bln seems to be the most favored scenario. Third, Draghi has indicated that rates will not be lifted until after the asset purchases are complete. The unknowns are with the devil in the details. |

Economic Events: Eurozone, Week September 25 - Click to enlarge |

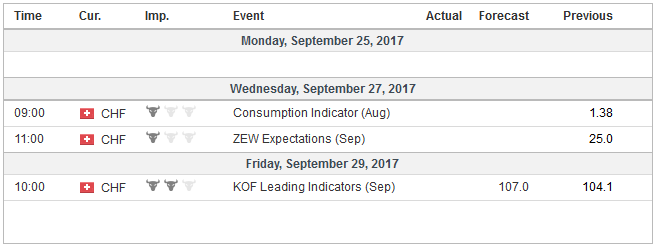

Switzerland |

Economic Events: Switzerland, Week September 25 - Click to enlarge |

Full story here Are you the author?

Tags: #GBP,#USD,$EUR,$JPY,$TLT,newslettersent,NZD