Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Following strong Q2 GDP figures, risk is that Bank of Canada’s rate hike anticipated for October is brought forward.

ECB’s guidance to that it will have to extend its purchases into next year will continue to evolve.

Among Fed officials speaking ahead of the blackout period, Brainard and Dudley’s comments are the most important.

Four central banks from high income countries hold policy is making meetings in the first full week of September. They are the Reserve Bank of Australia, Sweden’s Riksbank, the Bank of Canada, and the European Central Bank. Investors focus on the latter two.

To be sure, no one expects the ECB to change rates or policy. At most, some guidance into its intentions after current buying commitment is fulfilled at the end of the year. The Bank of Canada is the only major central bank that could raise rates.

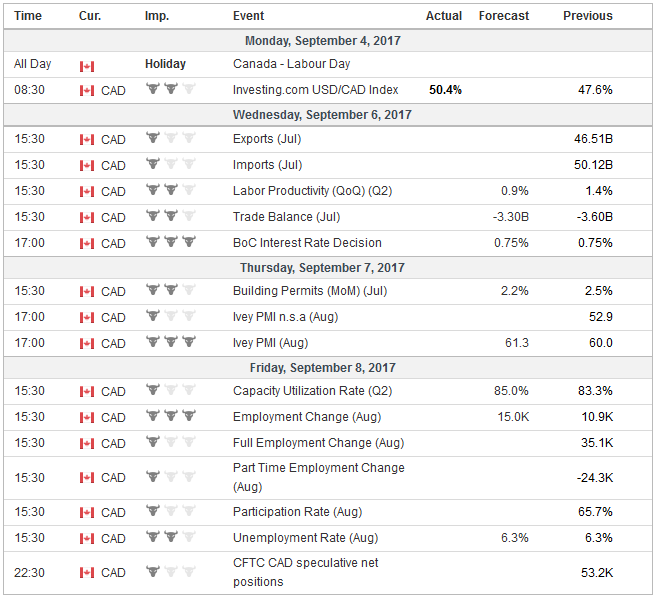

CanadaSince early June, the Bank of Canada put the market on notice that it no longer judged that the economy warranted the level of accommodation that in did in 2015 when it cut rates twice. It took one of those cuts back in July and was expected to take the other one back in October. News last week that the Canadian growth continued to accelerate in Q2 spurred speculation that the rate hike can be brought forward to Wednesday, September 6. Growth in Q2 unexpectedly increased to 4.5% on an annualized basis from 3.7% in Q1. Economists were looking at an unchanged rate, while in July, the Bank of Canada suggested a modest slowing to 3% was likely. Consumption rose 2.6%. This is not to suggest that the Canadian economy is firing on all cylinders. It is not. The housing market remains a concern for policymakers. The effects of the macroprudential efforts to rein in excess in the housing market in Vancouver seem to be wearing off, warning of similar results in the Greater Toronto area that more recently implemented analogous policies. Non-energy exports are struggling to find traction, they fell in June, though are up from a year ago. The July merchandise trade balance will be reported the same day as the Bank of Canada meeting. The impact of the storm that socked Houston and the Gulf of Mexico may encourage caution. There is also uncertainty surrounding the future of NAFTA after Trump renewed this threat to withdraw. The second round of NAFTA negotiations began on September 1 in Mexico City and will continue through September 5. US businesses have begun pushing back against some of the demands by the Trump Administration, especially on changes in the domestic content rules and the push to jettison the trade tribunals. This latter point was a red line for Canada. The Bank of Canada’s meeting on September 6 will not be followed by a press conference or a Monetary Policy Review. The Canadian dollar rallied 2.6% against the US dollar after the strong GDP reported, and pushed the US dollar below CAD1.24 for the first time in two years. Speculative positioning in the futures market is extended. The net long position in August reached it highest level in a little more than four years, while the gross long speculative position moved is holding above 80k contracts for the first time in five years. Interpolating from indications from Overnight Index Swaps, the market has a slight lean in favor of a hike next week. That said, we suggest that the Canadian dollar may weak regardless of when the Bank of Canada does. A rate hike may spur selling on the fact after the rumor was bought. Standing pat would see the Canadian dollar weaken on disappointment. We suspect that the failure to hike rates would produce a better buying opportunity. Confidence that a hike will be forthcoming will bring in new demand on the pullback. A hike, ironically, will leave the market unsure if the Bank of Canada intends to simply reverse the 2015 cuts or will it continue to hike. |

Economic Events: Canada, Week September 04 - Click to enlarge |

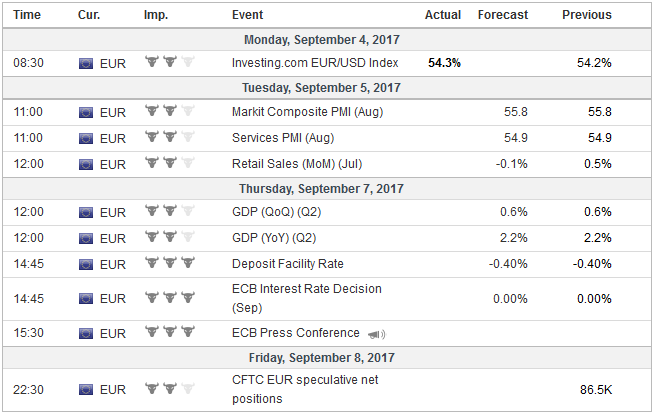

EurozoneThe ECB is facing a similar dilemma. Growth is strong, but price pressures remain subdued, and not yet, convincingly moved onto a sustainable path toward the ECB’s target for the headline rate of near but less than 2%. The rise of the euro and backing up of market rates have tightened financial conditions that in turn will, if anything, serve to dampen price pressures. The ECB’s language has evolved in recent months. The downside risks to the economy have disappeared in the wake of persistently high growth at levels that are sufficient to absorb excess capacity. The risk of deflation has disappeared. This has been an important factor driving the euro and interest rates higher. European equities have been a different story. Money may still be flowing into European equity funds, but the Dow Jones Stoxx 600 peaked nearly four months ago. German’s DAX peaked in mid-June. France’s CAC peaked in early May. There is an under-appreciated irony here. The French stock market peaked shortly after Macron was elected President. The euro gapped higher after it became clear he would win, and it has not looked back. There are three components of the ECB meeting that have to be considered. First, are the staff forecasts. These are not simply an academic function. It is tied to policy in a way that the Fed’s dot plots, for example, do not. The market will be more sensitive to a cut in the inflation forecast than an increase in the growth forecast. Projecting lower inflation would be understood as a dovish signal, and point to modest policy adjustment. |

Economic Events: Eurozone, Week September 04 - Click to enlarge |

GermanySince the forecasts were made in June, the euro’s rise has largely offset the rise in oil price, and while 10-year German bund yields are higher, French, Italian and Spanish benchmark yields have declined. The PMIs suggest that regional economy may have lost a bit of momentum in Q3, though it continues to operate at a high level. In the coming days, the Eurostat will report July retail sales (likely fell) and industrial production (likely bounced back after sharp 0.6% decline in June). The second component is the ECB’s next policy step. We had expected that the ECB would take advantage of the new staff forecasts to announce that it will extend the asset purchases next year but at a slower pace. However, the strength of the euro, which briefly traded above $1.20 last week (and approached the 50% retracement objective of the depreciation that began in mid-2014-~$1.2165), has increased the risk that the ECB waits a little longer to announce its decision. It must ultimately extend the purchases or make a potentially destabilizing hard stop (except for the reinvestment of maturing issues that are estimated to run at a little more than 10 bln euros a month). Instructing the relevant committees to review the issue, in the context of a lower inflation forecast would be seen a dovish development, but we don’t think it changes the outcome. There is two aspects of the policy that is important to investors, assuming that no new assets are added to the mix or taken away (though we would not rule out stopping buying ABS, which has seen low and diminishing interest): the length of the extension and the amount to be purchased. The current extension was for nine months (until the end of this year). We suggest a six-month extension now maximizes the flexibility that policymakers need. It would also cover the period of the run-up to the Italian election next spring (the date and rules have yet to be determined). At its peak, the ECB was buying 80 bln euros of assets a month. This was reduced to 60 bln since March. If the ECB were to reduce the purchases to 40 bln euros a month as a majority of the Reuters poll would have it, this would imply the ECB would be expanding its balance sheet for nearly all of 2018. This is too big a commitment, which despite the program’s flexibility, will be seen by such an announcement. We suggest that a 30 bln reduction (to 30 bln euros) would maximize the ECB’s flexibility. Having made a 30 bln euro adjustment, it could do so again in after H1 and end the purchases. On the other hand, if needed it could taper further at mid-year. It would also allow continued broadly adhering to the capital key, which is an important principle in Europe beyond its use in QE. The third-factor investors need to grapple with is the euro and market psychology. After moving above $1.20 on August 29, the euro could not sustain the momentum, and it has slipped lower. The disappointing US core PCE deflator and employment growth saw the euro make another run at $1.20 before the weekend (~$1.1980) before selling off on reports of the ECB’s cautiousness next week. The euro finished just off session lows. At the start of this year, many were concerned about the extreme long dollar positioning. Dollar sentiment seems as extreme now but in the opposite direction, and the euro is the un-dollar of choice. From March 2015 through June 2017, the euro was largely range-bound between roughly $1.05 and $1.15. The highs in August 2015 and May 2016 marked by similar price action as we saw last week-euro rally to new highs but finishing on its lows. We had linked our expectation of a better fourth quarter for the dollar partly to the idea that the lifting of the US debt ceiling will drain around $400 bln as the Treasury’s steps to maneuver around the ceiling are reversed. |

Economic Events: Germany, Week September 04 - Click to enlarge |

United StatesDue to the idiosyncrasies of the US political system, the emergency funds for the area devastated by the recent storm may be tied to lifting the debt ceiling. It is not clear, but this could take place in the coming days. Lifting the debt ceiling would ensure that the government does miss a debt payment. New spending authorization is a different matter. The failure to reach an agreement could lead to a temporary shutdown of what are regarded as unessential services. President Trump has threatened to allow the government to shut if funding for the wall with Mexico is not provided. That brings us to the third central bank that will draw investor attention. The FOMC does not meet until September 19-20. However, ahead of the blackout period (starts September 9), several Fed officials will speak. We think Governor Brainard and NY Fed President Dudley comments are the most important. Brainard previously seemed to lead the Fed’s concern about the international prospects, and more recently was among the first to flag the softening price pressures. Dudley part of the troika (with Yellen and Fischer) that seem most often expressing the policy signal. Dudley most recently suggested the balance sheet operation would begin shortly (announcement this month), and that he would be inclined to raise rates again provided there were no downside surprises. The impact of the storm could shave 1% off Q3 GDP and 0.5% of Q4 GDP to use rough and ready estimates. It will produce all kinds of distortions in the economic data. How will the Fed navigate those, on top of the drama in Washington? Can the Fed begin allowing the balance sheet to shrink in October even if the government may be shut? We look toward Brainard and Dudley to shed light on how the Fed is wrestling with these issues. |

Economic Events: United States, Week September 04 - Click to enlarge |

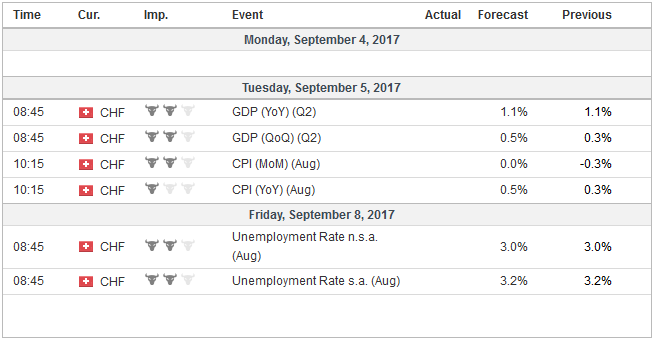

Switzerland |

Economic Events: Switzerland, Week September 04 - Click to enlarge |

Full story here Are you the author?

Tags: #USD,$CAD,$EUR,Canada,central-banks,ECB,European central bank,Federal Reserve,newslettersent