Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

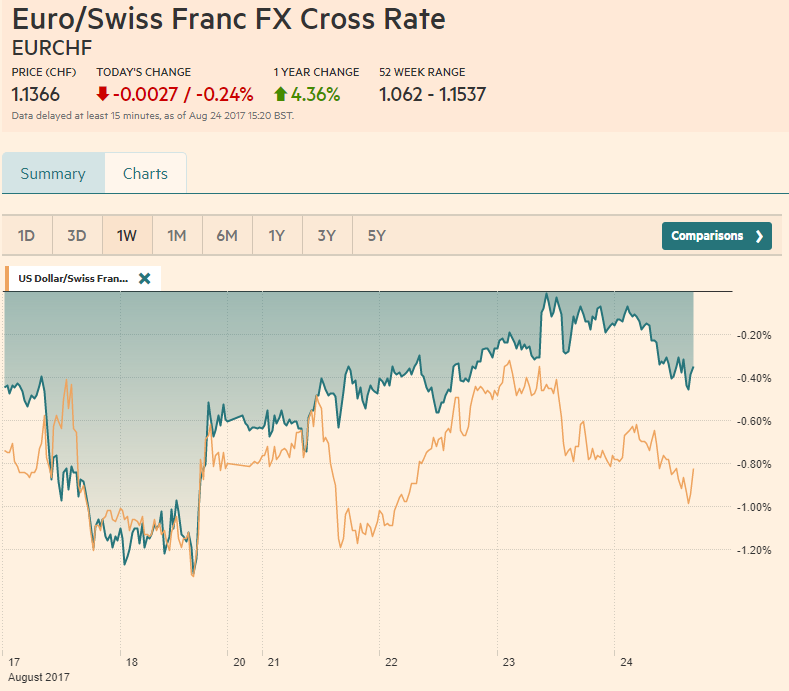

Swiss FrancThe Euro has fallen by 0.24% to 1.1366 CHF. |

EUR/CHF and USD/CHF, August 24(see more posts on #USD, $CHF, EUR/CHF, ) Source: markets.ft.com - Click to enlarge |

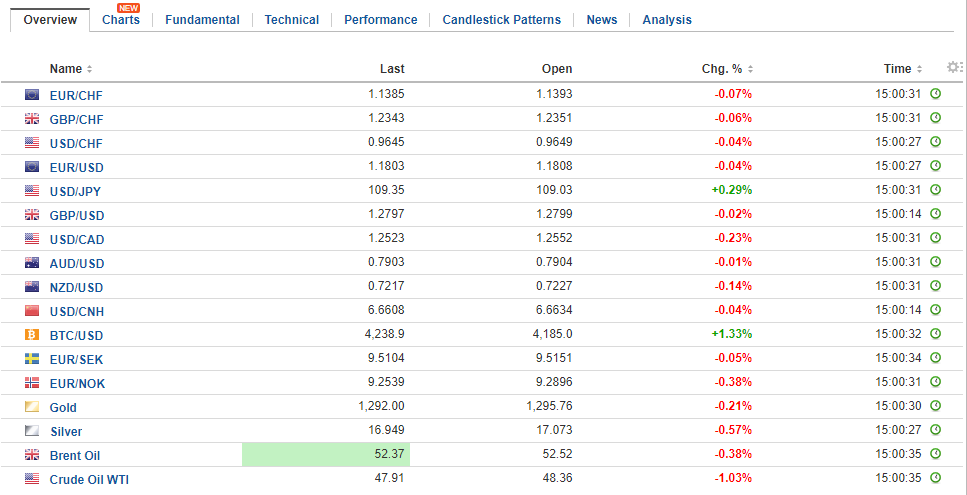

FX RatesThe US dollar is enjoying a firmer tone in quiet. Sterling is stabilizing after grinding down to its lowest level since late June. The Mexican peso, which had dropped in thin trading in Asia and Europe yesterday following Trump’s threat to exit NAFTA and force Congress to fund the Wall or face a government shutdown recovered fully and is now slightly higher on the week. The dollar continues to chop around in well-worn ranges against most of the major currencies. The euro has been confined to a little more than 15 pips on either side of $1.18. The dollar fell to almost JPY108.80 in early Asia, but recovered and at pixel time is knocking on JPY109.40. Sterling made a marginal new low at $1.2775. It may have looked like it was breaking out, but is recovering back toward $1.2820. A move above $1.2835 would stabilize the tone. The dollar-bloc currencies are stabilizing–the Aussie with a softer bias and Canada with a slightly firmer bias. The New Zealand dollar briefly wss pushed below $0.7200 for the first time since mid-June but also recovered. |

FX Daily Rates, August 24 - Click to enlarge |

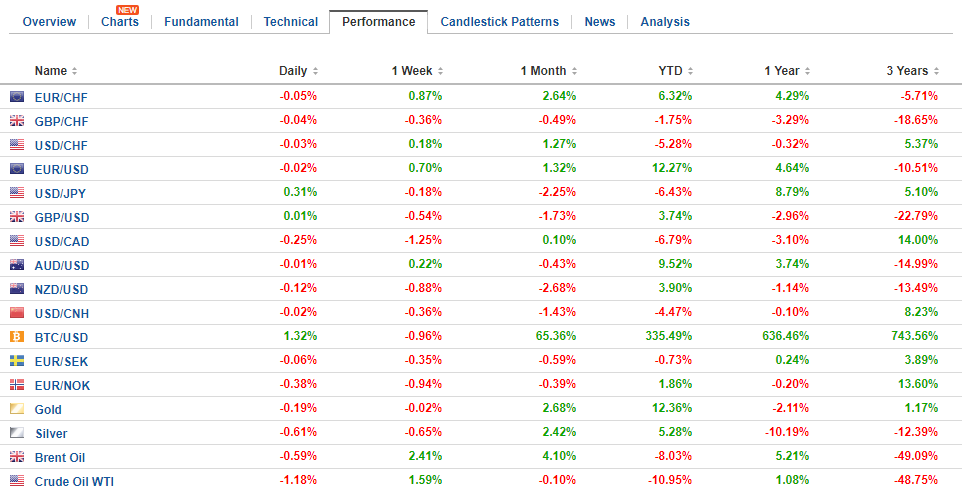

| Benchmark 10-year yields are mostly firmer but at low levels. The US 10-year yield is up a single basis point and remains below 2.2%. It peaked near 2.40% in early July. Similarly, the yield on the 10-year German Bund peaked in mid-July near 62 bp and is below 38 bp today. Inflation appears to have converged. The Fed’s preferred measure, the core PCE deflator stood at 1.4% in June. The ECB’s preferred measures, headline CPI was 1.3% in July (core at 1.2%). However, the similar rates of change disguise the fact that the quantities (the baskets of goods and services) that are measured are not the same. To avoid the problems associated with this discrepancy is why there is a common methodology (HICP) in Europe, while many countries also track their own metric. |

FX Performance, August 24 - Click to enlarge |

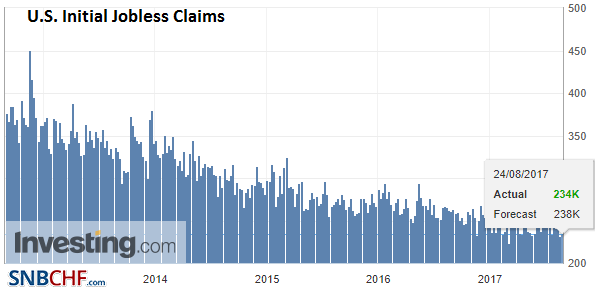

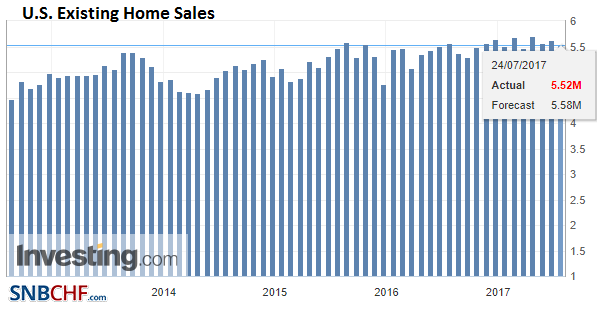

United StatesThe North American economic calendar turns more active today, but it is not the stuff that moves the market, and this seems doubly true in the current environment. Investors know that the US labor market continues to move in the right direction, so jobless claims offer little new. We note that the four-week average is about 5k above its cyclical low reached in mid-May. Existing home sales may attract somewhat better attention after yesterday’s unexpected weakness in new home sales. |

U.S. Initial Jobless Claims, 24 August 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

| Since last September, existing home sales have alternated between rising and falling on a monthly basis. Sales fell 2.9% in June and are expected to have risen by around 0.5% in July. The Kansas City Fed’s manufacturing survey attracts little interest, but it is likely to be consistent with a pick up in US economic activity in H2. |

U.S. Existing Home Sales, Jul 2017(see more posts on U.S. Existing Home Sales, ) Source: Investing.com - Click to enlarge |

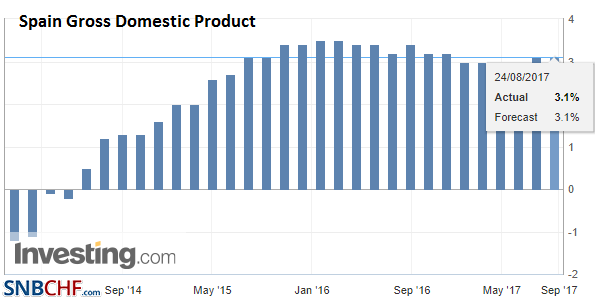

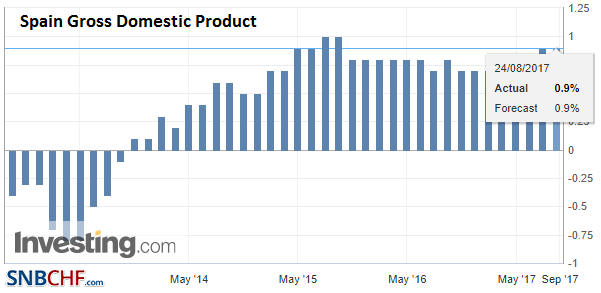

Spain |

Spain Gross Domestic Product (GDP) YoY, Q2 2017(see more posts on Spain Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

Spain Gross Domestic Product (GDP) QoQ, Q2 2017(see more posts on Spain Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

|

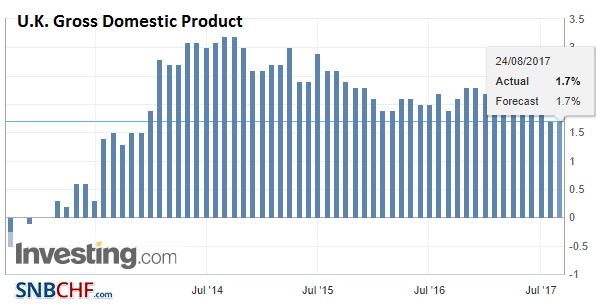

United Kingdom |

U.K. Gross Domestic Product (GDP) YoY, Q2 2017(see more posts on U.K. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

Equities are mixed. In Asia, Japan and Chinese markets fell, but most other equity markets gained. Nevertheless, the MSCI Asia Pacific Index slipped marginally for the first time this week. Of note, Japanese steelmakers fell as Toyota reported is forcing suppliers to cut prices. European bourses are mostly higher, and the Dow Jones Stoxx 600 is up about 0.4% in subdued turnover, led by utilities, materials, and financials.

The highlight of what has been a quiet week is at hand. The Jackson Hole Symposium begins today, but the keen interest is on tomorrow’s speakers. Yellen is scheduled to speak at 10:00 am ET and Draghi at 3:00 pm ET. Expectations appear quite modest going into the confab, and for a good reason. Reuters reported earlier that Draghi would not address monetary policy. The consensus narrative in the market is that the ECB will be taking a step toward the exit. Some see that exit also being forced by the limits of country exposure.

We gently disagree. We see the glass as more than half full and increasing. That is to say, that ECB’s balance sheet has not peaked, and the divergence between its balance sheet and the Fed’s has also not peaked. At the current pace,the ECB will buy 240 bln euros of assets between Sept 1 and the end of the year. The announcement we expected from the ECB in early September is that it will extend its purchases but at half the pace for the first half of 2018. This would add another 180 bln euros to the ECB’s balance sheet.

Meanwhile, few now doubt that the FOMC has reached a consensus to begin letting its balance sheet shrink. Remember in this process; the Fed will not sell a single note or bond. What it will do is simply not rollover the full amount of Treasuries or MBS that are maturing. It is meant to be the least disruptive as possible. There has been some suggestion in light of Trump’s threat to close the government that such an event would delay the Federal Reserve.

Given the congressional calendar and what are still contentious issues, the FOMC meeting that concludes on September 20 will likely make its decision before the debt ceiling is lifted and new spending authorized. The implementation of the FOMC’s balance sheet operation is very small and, unless there is a protracted shutdown, which is not the most likely scenario, the vagaries in Washington should have little impact.

The Korean won is the strongest of the emerging market currencies this week, rising 1.2% as the bellicose rhetoric has ceased, though extensive US-Korean military exercises are ongoing. Last year, North Korea launched a ballistic missile from a submarine during the annual exercises. The Kospi is one of the strongest equity markets this week in Asia, and foreign buying has returned, though even with the roughly $225 mln of equities they bought, still leaves than with about $1.1 bln of Korean shares that they own at the beginning of the month.

Graphs and additional information on Swiss Franc by the snbchf team.

Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CHF,$EUR,$TLT,EUR/CHF,EUR/CHF and USD/CHF,Korea,newslettersent,Spain Gross Domestic Product,U.K. Gross Domestic Product,U.S. Existing Home Sales,U.S. Initial Jobless Claims