Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

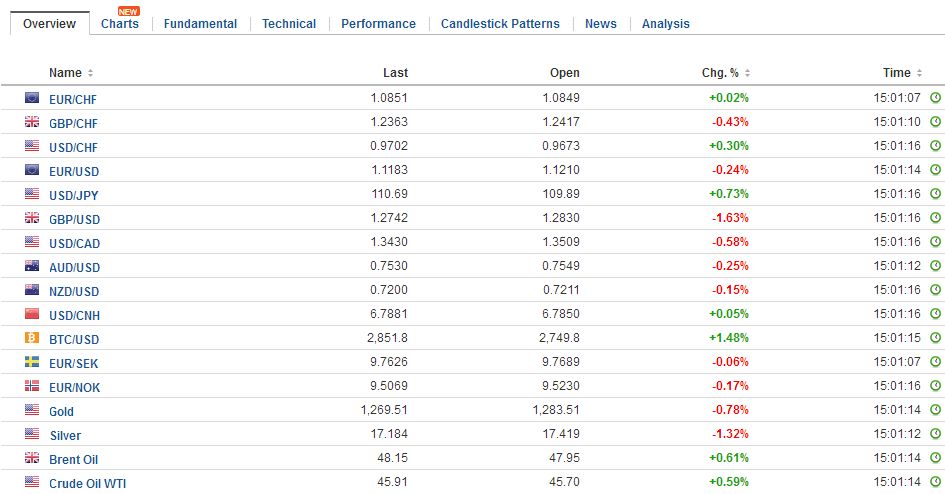

Swiss FrancThe euro is up by 0.02% to 1.0851 CHF.

|

EUR/CHF - Euro Swiss Franc, June 09(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesWhat looked like a savvy move in late April has turned into a nightmare. Collectively, voters have denied the governing Conservative party a parliamentary majority. The uncertainty today does not lie yesterday with the known unknown, but with the shape of the next government and what it means for Brexit. The thinking now is that the Tories could form a coalition with the Irish Unionists, who also favor Brexit. Contrary to expectations, Prime Minister May has not offered her resignation and insisted that she will stay. Our concern pre-election was even in victory May would be a weaker leader. Some are concerned that another election may have to be held later this year. The squeeze apparently engineered by Chinese officials that effectively, intended or otherwise, strengthened the yuan after Moody’s downgrade, appears to run its course. If offshore investors thought so, the place to look is the offshore yuan. This week it snapped a four-week advance. The onshore yuan extended its streak to five. The US data consists only of April wholesale inventories. An input for GDP calculations, but it is not a market mover. Canada reports May jobs. It lost 31k full-time positions in April and gained 3.2k jobs overall. A better employment report is expected. The Canadian dollar is off about 0.2% this week. The greenback spiked to CAD1.3540 earlier today, but the Canadian dollar has recovered. The US dollar is flirting with the 20-day moving average near CAD1.3510. It has not closed above that moving average since May 15. A close above CAD1.3550 would be a very constructive technical development. |

FX Daily Rates, June 09 - Click to enlarge |

| Sterling had appreciated for four consecutive sessions before yesterday minor decline. It had risen eight of nine sessions. The sharp sell-off, the bulk of which took place in the immediate reaction to the exit polls that pointed to a hung parliament as soon as voting ended, took sterling to about $1.2635 from around $1.2955. In effect, sterling retraced, almost to the tick, the 38.2% of the rally from the year’s low just below $1.20 in mid-January. The next target is the $1.24-$1.25 area, and that seems to be a reasonable objective in the coming weeks.

It is understood that UK rates will be lower for longer. There is a slight bullish steepening move in the debt market (debt instruments have rallied across the curve with the short-end rallying more). UK equities are mixed. The FTSE 100, with its currency sensitivity, has rallied a little more than 0.6%, but the real performance is mixed, as the FTSE250 is down 0.8%. US rates edged higher this week, and European rates edged lower. The euro was capped at $1.1285 at the end of last week and the first half of this week. It recorded the low for the week near $1.1170 in early European turnover. Look for the $1.1200-$1.1220 area to now offer resistance. Last week’s low was just above $1.1100. The turning of interest rate differentials and the loss of upside momentum may make for a cautious activity. The first round of the French legislative election will be held Sunday. Macron’s new party is expected to do very well. The dollar is finishing the week on a firm note against the yen. After falling to almost JPY109 in the middle of the week, the dollar clawed its way back to nearly JPY110.50 today. Rising US yields and the prospect of a Feb rate hike next week may encourage some re-positioning. The next target is near JPY110.70, but it may take a move above JPY111.20 to give confidence that a low is in place. We had noted that some investors had seen the FTSE 100 as a way to position for the election. If the Tories had expanded their mandate, UK stocks would have rallied. If the Tories did not do so well, the rally in FTSE 100 would blunt some of the impacts from a weaker sterling. Some would have hedged the currency. |

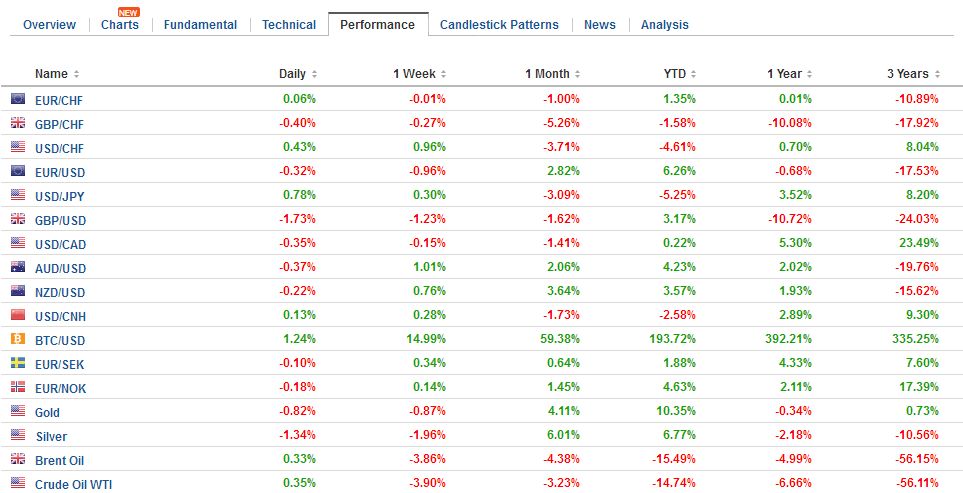

FX Performance, June 09 - Click to enlarge |

Germany |

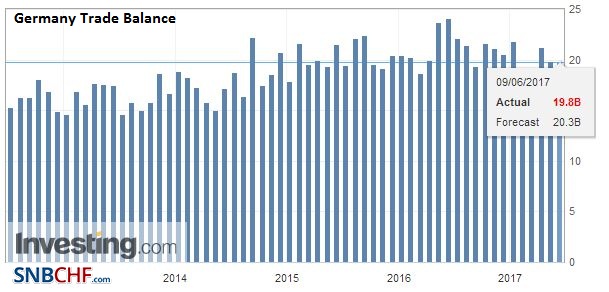

Germany Trade Balance, April 2017(see more posts on Germany Trade Balance, ) Source: Investing.com - Click to enlarge |

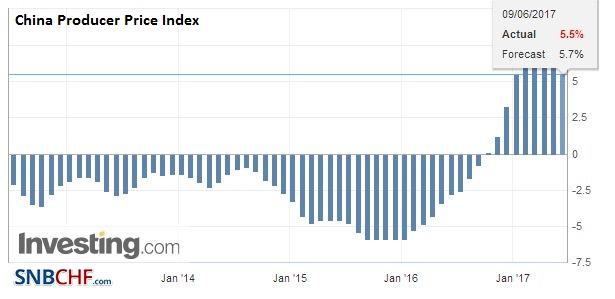

ChinaThe reaction to the UK events overshadowed the release of China’s May inflation figures. Producer price pressures eased for the third consecutive month, slowing to a 5.5% year-over-year pace, from 6.4% in April. This is mostly a function of lower commodity prices and base effect.

|

China Producer Price Index (PPI) YoY, May 2017(see more posts on China Producer Price Index, ) Source: Investing.com - Click to enlarge |

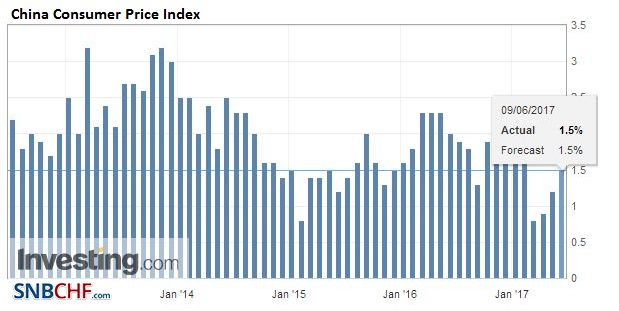

| Consumer prices rose in line with expectations. The 1.5% pace compares with a 1.2% pace in April.

The headline figure understates Chinese consumer inflation. The decline in food prices is ebbing. They have been negative on a year-over-year basis since February, but the pace is slowing. Excluding food, consumer prices were up 2.3% year-over-year–in the middle of the 2.0%-2.5% range seen since last 2016. A core measure that excludes food and energy would show consumer prices up 2.1% up from 1.9% last December. |

China Consumer Price Index (CPI) YoY, May 2017(see more posts on China Consumer Price Index, ) Source: Investing.com - Click to enlarge |

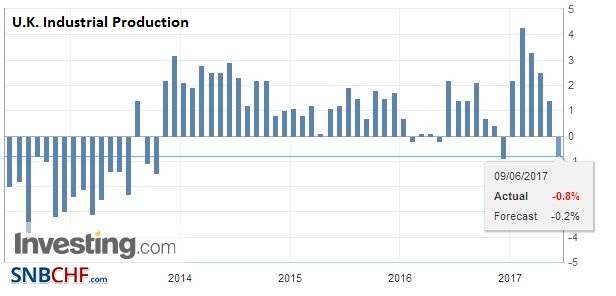

United KingdomAdding insult to injury, the UK reported softer than expected industrial production, manufacturing output, and construction. Industrial production rose 0.2% in April. It was a smaller bounce back from the 0.5% decline in March than the 0.7% median forecast had it. |

U.K. Industrial Production YoY, April 2017(see more posts on U.K. Industrial Production, ) Source: Investing.com - Click to enlarge |

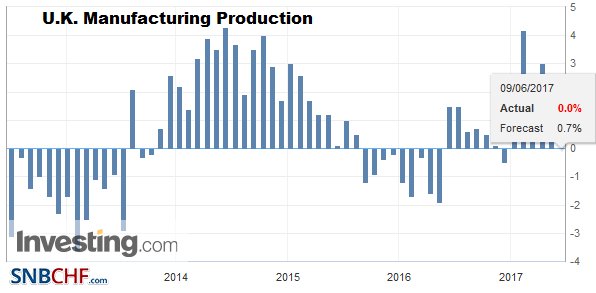

| Manufacturing rose 0.2%, rather than the expected 0.8%. Construction output fell 1.6%. The median had looked for a 0.4% increase. A saving grace was that the March series was revised to 0.7% from -0.7%. |

U.K. Manufacturing Production, April 2017(see more posts on U.K. Manufacturing Production, ) Source: investing.com - Click to enlarge |

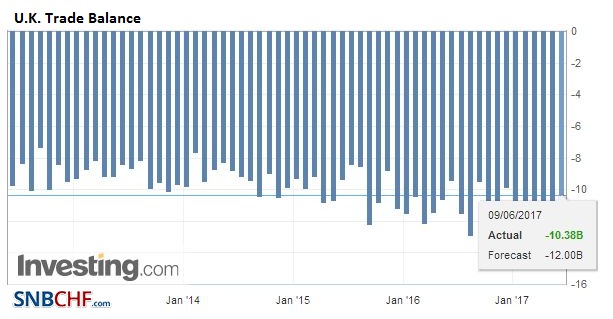

| The silver lining of today’s data was the trade balance, where the deficits narrowed, and revisions narrowed the March shortfall as well. |

U.K. Trade Balance, April 2017(see more posts on U.K. Trade Balance, ) Source: Investing.com - Click to enlarge |

The conceit is that a hard or soft Brexit will be determined by the next government. Once Article 50 was triggered, the initiative shifted from the UK to the EU. As long as the UK insists on asserting its sovereignty over its borders it cannot expect to share in the single market, where sovereignty has been abridged, on equal footing.

Besides the loss of the Tory majority and the unexpectedly robust showing for Labour, two other observations stand out in these early hours. First, the Scottish Nationalist Party did poorly, and this will undermine efforts for a second referendum. Second, young people had a very strong turnout–above 70%. It is not clear the extent that this was a due to Corbyn’s draw or the retaliation for the referendum where young people typically had voted to remain.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$JPY,China Consumer Price Index,China Producer Price Index,EUR/CHF,FX Daily,Germany Trade Balance,newslettersent,U.K. Industrial Production,U.K. Manufacturing Production,U.K. Trade Balance