Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

ECB may take a baby step toward the exit of extraordinary monetary policy by confirming rates are unlikely to be cut further and the risks are roughly balanced.

UK election is coming down to the wire.

In the US, former FBI director Comey is set to testify, and leaks of two Fed appointments overshadow mostly second-tier economic data.

This week’s two main events, the ECB meeting and the UK national election have drawn investors intentions in recent weeks. The ECB may take a baby step on what promises several quarter exit path from its extraordinary monetary policy.

UK Prime Minister May’s call for a snap election was seen as a strong move, taking advantage of the apparent weakness of her domestic rivals and strengthen her hand in negotiations with the EU. At the same time preventing an election that would have complicated the conclusion of the Brexit negotiations. May used the reaction to the US decision to pull out of the Paris Accord as an opportunity to put some distance between the UK and the German, French and Italian response. In recent weeks, the initial Tory lead has been whittled away to the point that YouGov is projecting it will be 18 seats shy of a majority.

A combination of energy prices, the past depreciation of the euro, and higher prices of some vegetable prices pushed up headline and core inflation in the euro area. It is acceptable for central banks to look through some economic developments if the impact is thought to be transitory This is what the Fed has repeatedly done, and the Bank of England is doing it now, with inflation running a bit hot.

Over the past year, generally speaking, developments that favored what is arguably an ill-defined soft Brexit often was seen as positive for sterling. Developments that were seen as tilting the odds in favor of a hard Brexit were often sterling negative. Now that Article 50 has been triggered this may change. Ostensibly, formal negotiations will begin shortly after the election. Much of the initiative now is in Brussels’ hands. Perceptions of a weak leader at 10 Downing Street may be harmful to the investment climate at precisely when circumstances require more.

United KingdomIn the UK the need for a coalition government is often referred to as a hung parliament. If the election does result in a hung parliament, a coalition will be particularly tricky. The tightening of the polls is not so much driven by the loss of Tory support, despite some seemingly electoral gaffes. Rather what appears to have happened is that the Labour Party is increased its support primarily at the expense of the Liberal Democrats and the UK Independent Party. The Scottish Nationalist Party may unexpectedly find itself in a position to shape Brexit, with knock-on implications for a second referendum on independence (and staying in the EU). The economy slowed more than expected in Q1 and did not appear to be reaccelerating in Q2. Inflation is expected to peak in the coming months when oil’s recovery and the impact from sterling’s steep losses fade. The Bank of England meets the middle of June again but is widely understood to be on hold for a considerable period. The Brexit negotiations are going to be fraught with tensions and harsh words, especially in the beginning of this two-year process for which the clock is already ticking. The liberal global trading system that has evolved over the last 70 years is being challenged from within at the same time that terrorism is threatening from without. A third terrorist strike in the UK this year took place on Saturday. If May’s call for an election in the first place, which contravened the previous Tory government’s attempt to set fix schedules for elections, was unexpected, the relative success of Labour, led by Corbyn, is a complete and utter surprise. A Labour-led coalition government would like to scare many investors, and the first instinct may be to sell-off UK assets if this became a distinct possibility. The FTSE 100 reached new record highs before the weekend. There seemed to be an interesting logic at work. If the election outcome was favorable than equity market would rally and the FTSE 100 would go for the ride. If the election outcome were unfavorable, sterling would be sold and this would cushion the downside of the FTSE 100 where foreign earnings are so important. |

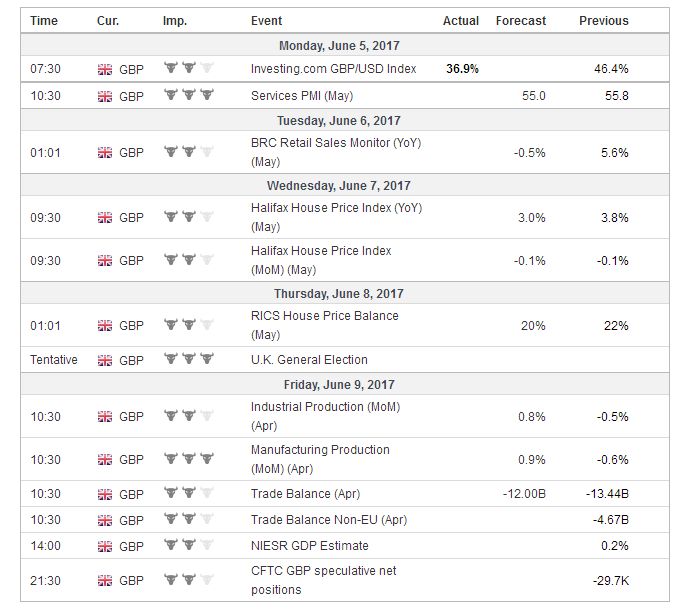

Economic Events: United Kingdom, Week June 05 - Click to enlarge |

United StatesThe Lib-Dems may be reluctant to enter into a new coalition with the Conservatives. They were decimated in the last election, and may not win sufficient seats to give a coalition a majority. The Tories had been loath to formally enter a coalition with UKIP, but post-referendum, and given the political realities, it may be reconsidered. In foreign exchange market, the US dollar’s weakness is masking political anxiety in sterling. However sterling has lost about 4.5% against the euro in a slide over the past six consecutive weeks. It has fallen nearly 3% against the yen in the ongoing four-week drop. On a trade-weighted basis, sterling fell throughout May, losing 2.75%, before recovering a little last week. Volatility has increased (three-month implied) for the past three weeks, and the skew in the risk reversal (puts and calls) has moved sharply in favor of puts. There is little technical or fundamental reason to expect the euro to reverse lower in the week ahead. The US economic data calendar is light. The non-manufacturing ISM, durable goods orders and consumer credit will not alter investors minds about the trajectory of Fed policy. Fed officials enter their quiet period ahead of the next FOMC meeting so they will not be able to try to shape the investors’ understanding of the recent news that included the third successive decline in the core PCE deflator, weaker auto sales (which may have knock-on effects on retail sales and future impact manufacturing output), and a tepid employment report. Not only will European events overshadow US economic news, but so will the US politics. First, there are press reports claiming to have identified President Trump’s first two appointments to the Federal Reserve’s Board of Governors. Rather than commenting on the candidates themselves, we share a caveat. Investors may want to look past some partisan claims. There are few dissents from Governors in recent years. It is difficult to tell based on voting records which Governors were appointed by a Republican President and which by Democrat Presidents. The second important US political development is the testimony of former FBI Director Comey before the Senate Intelligence Committee investigating the alleged involvement of Russia in last year’s election. It is important for investors because the more protracted the imbroglio, the more investors may question the Administration’s ability to legislate its economic program that had included corporate tax cuts, and tax reform, deregulation and a large infrastructure initiative. Ironically, a distracting political crisis would likely be bullish US bonds, on slower growth and inflation ,and less demand for capital. That decline in interest rates may weaken the dollar while lending support to equity prices. As it turns out, Governor Powell is currently the only Republican appointee. His voting record and demeanor suggest great continuity if the speculation is true that he replaces Yellen as Chair early next year. That said, Volcker, Greenspan, and Bernanke were each appointed by the President from one party and reappointed by the President of the other party. |

Economic Events: United States, Week June 05 - Click to enlarge |

EurozoneIn contrast, most developments on the Continent have gone rather swimmingly. The eurozone economy continues to expand at a solid and steady rate of about 0.4% a quarter. The political threat posted by the (among other things) anti-EMU populist-nationalism has been turned back at every opportunity. The threat of an Italian banking crisis subsided. An index of Italian bank share prices is up more than 10% year-to-date. Italy seems to be moving toward a precautionary recapitalization of Monte Paschi, and could also include addressing Veneto banks as well. Although Greece’s debt burden has not been lifted, the risk of another crisis seems to have been put off until at least until toward the middle of next year when the current aid package ends. In the meantime, Greece’s 10-year yield has fallen 100 bp this year already, and it has practically all happened in the March and April. Greek stocks have also rallied strongly this year. The 22% gain of the Athens’ Stock Exchange is the most in Europe. Some of the creditor nations in the eurozone have never been wholly supportive of many of the unorthodox measures, and seem to seek the earliest possible exit. As economic conditions have evolved, the ECB collectively has modified its forward guidance and is preparing to do so again on the same day as the UK goes to the polls. Specifically, the ECB is expected to modify its language on the outlook for interest rates and its risk assessment. The ECB has told investors that interest rates will remain at present or lower levels if needed. It can drop the downside bias. The market has effectively done this already. The ECB would be validating what the market has done. The ECB has indicated that downside risks have diminished, and the ones that exist stem from exogenous factors (maybe Brexit, US trade policy, China’s economy). It could say the risks are fairly balanced, and it would be a small incremental change. The ECB’s staff will update its forecasts. Growth forecasts may be revised a little higher. What would reinforce Draghi’s message that inflation is not yet on a sustained path toward the target despite the recent elevated readings would be driven home if the staff trimmed this year and/or next year’s inflation forecast. Medium-term averages of the euro have risen around 5% since its March forecasts, and a medium-term average of the Brent has fallen by about 5%. Buy the rumor, sell the fact type of activity could be seen in response to the ECB, but sentiment toward the euro may not change unless US rate premium grows. The euro finished last week on its highs of the year, within striking distance of $1.13, last seen in the early response to the US election last November. A potential trendline is drawn off the August 2015 high (~$1.1715), and May 2016 is found near $1.1450 by the end of June. (~$1.1615). |

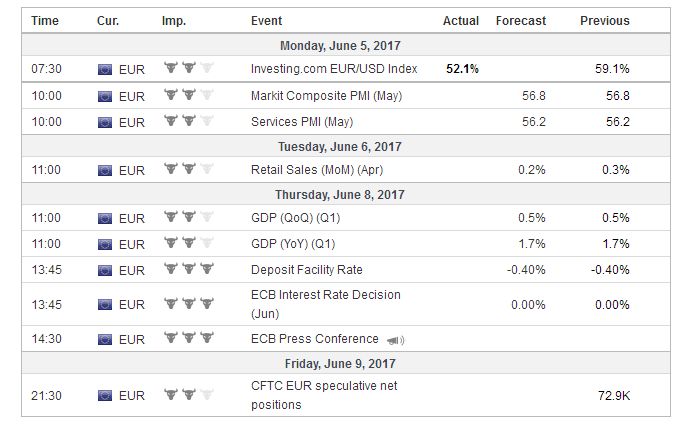

Economic Events: Eurozone, Week June 05 - Click to enlarge |

Switzerland |

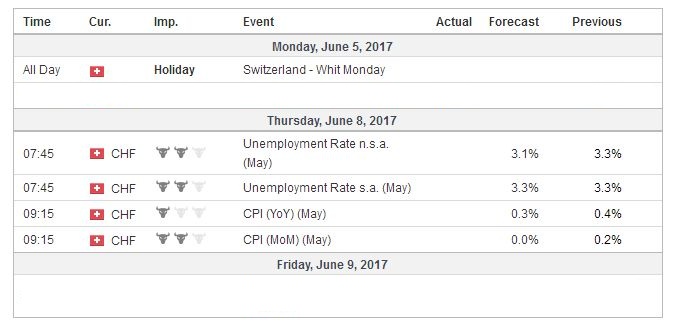

Economic Events: Switzerland,Week June 05 - Click to enlarge |

Tags: #GBP,#USD,$EUR,newslettersent