Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

There were no celebrations; no horn or trumpets, nary a sound, but an important shift took place last week. The shift was signaled by two events. The first was the US strike on Syria, and the second was investors’ willingness to look past Q1 economic data.

The US missile strike on Syria was significant even if it fails to change the dynamics on the ground. It undermines the Trump Administration’s ability to “reset” the US relationship with Russia. What the new Administration recognized last week is that the tension in the US-Russian relationship was not a function of personalities or leadership styles but a genuine and fundamental difference of national interests. Russia supports the Assad regime as it supported his father’s. It is the key way Russia can project its power and influence into the Middle East.

The G7 finance ministers meetings understandably are important for investors. The meeting of foreign ministers hardly draws much notice. However, their meeting on April 10-11 will attract interest. Many have labeled the Trump Administration as isolationist due to its criticism of the WTO, the UN, and other multilateral arrangements. However, we have argued this misunderstands the thrust of the Trump Administration. It is unilateralist, not isolationist.

An isolationist may argue that there is not a direct national interest at stake, and killing people (including children) with missiles from the sky to punish a government who killed people (including children) with gas does not make sense. A multilateralist would have allowed UN investigation and international law to run its course. The US, arguably, has a vested interested in the international rule of law. What Kremlin has called a significant blow to US-Russian relations may allow a new convergence of US and Europe perceptions of the threat Russia poses, but whether diplomats can work it out is a different matter.

Nevertheless, the Russian ruble will likely yield to the changing circumstances. It has been the strongest currency in the world since the US election, gaining 11.4%. It had made new highs for the year last week prior to the US missile strike (as the US dollar fell to almost RUB55.80). It would not be surprising to see the ruble unwind a good part of these gains, giving the dollar scope to rise toward RUB60-RUB62. The dollar-rouble exchange rate and oil prices typically are inversely correlated. On a rolling 60-day basis, the correlation of the percent change in the exchange rate and the Brent prices is -0,34, which is among the least over the past year.

EurozoneIn Europe, the aggregate February industrial production will be reported. In the national reports, German surprised big on the upside, while France and Spain disappointed. Italy reports an hour before the aggregate figure. The median Bloomberg forecast is for a 0.1% gain. The risk is on the downside. There are two important points to be made. First, the survey data in Europe, like in the US, appears to be running ahead of actual performance. The key question is how will these realign. How much does growth improve? We are more confident that below trend Q1 US growth will yield to stronger growth in Q2 than we are that eurozone growth can accelerate much from the current pace. Sentiment indicators may also soften in the months ahead. The second point is that for the ECB’s reaction function, the real sector is not the driver of policy. It is to boost consumer prices toward the ECB’s target of near but less than 2%. However, there are now numerous case experiments, and it is not clear that expanding the central bank’s balance sheet through the purchase of debt has a very high success rate it boosting the basket of goods and services that make up the CPI. The rise in inflation that raised the ire of the Bundesbank and a few other European central banker was a mirage caused primarily by the recovery in energy prices. Core inflation bottomed in early 2015 at 0.6%. The ECB’s balance sheet has expanded by more than a trillion euros, and the initial estimate suggests that core inflation stood at 0.7% last month. Meanwhile, the EU and Greece appears to be nearing an agreement that will free up another payment tranche that will allow Greece to make a large debt payment to its official creditors that comes due in a few months. Greece’s 10-year bond yield fell 19 bp to 6.86% last week. The yield peaked two months ago near 8.10%. It began the year near 7.10%. However, one key piece of the puzzle is missing: The IMF. |

Economic Events: Eurozone, Week April 10 - Click to enlarge |

GermanyThe IMF’s role is important because both the German and Dutch parliament say it is a prerequisite for their continued participation. The IMF has comes under criticism from many of its non-European members, including the US, for overruling its own internal policies and overexposing the multilateral lender to Greece. The US continues to enjoy a sufficient quota (votes) at the IMF to be able to veto a commitment of new funds. Blocking the IMF from participating in new lending to Greece could come at an awkward time for Germany given the national election in less than six months. Also, while there is awareness of the French presidential contest, few have focused on the legislative election in June. Neither of the leading candidates (Macron and Le Pen) commands a bloc in the current legislature. The French premium over German is elevated even if stable in recent weeks, but it is likely to persist for much of the second quarter. |

Economic Events: Germany, Week April 10 - Click to enlarge |

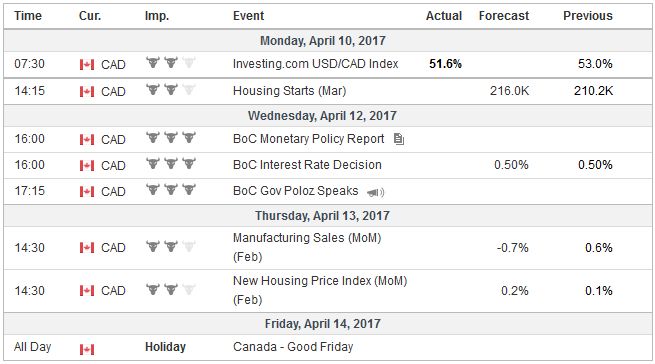

CanadaThe week ahead is short. After Wednesday, April 12, full liquidity will not return until April 18, following Easter Monday. The Bank of Canada is the only major central bank that meets. There is little doubt that policy is on hold. Under Governor Poloz, the central bank is very cautious despite a strong rebound in the last two quarters of 2016 (2.8% annualized pace in Q3 and 2.6% in Q4). The economy expanded by 0.6% in January, which was twice the pace expected. The labor market has been firm, even if exaggerated, which should help underpin demand going forward. The central bank expects the output gap to take another year to close (mid-2018). Bringing it forward could spark investors to anticipate a rate hike sooner. Uncertainty about US policy (trade and fiscal) may discourage a significant change in rhetoric. Even though the Federal Reserve does not meet, Yellen’s speech on Monday (with live and Twitter-sourced questions) will be closely monitored. Since the FOMC minutes, the focus has shifted toward the Fed’s balance sheet. There remain three issues of concern. The first is when will the Fed stop reinvesting maturing issues. Many had expected this to be a 2018 story, but the minutes and Dudley’s comments suggest Q4 is possible. The second issue is how will this be executed. Will the Fed focus on its MBS portfolio or its Treasury assets? The initial inclination is to do both. Should it be done all at once or should it be phased in over time? The mere fact that it doing it at once is even considered is striking. That course would be very aggressive given the maturing issues over the next two years (2018-2019 ~$770 bln of the $2.4 trillion Treasuries held by the Fed will mature). The Fed seeks to do it in a way that is predictable and transparent for investors and not disruptive. The third issue is the relationship between the balance sheet and the Fed’s interest rate policy. It is clear that the Fed will rely on its Fed funds target is its primary tool. Dudley has suggested that when the balance sheet begins shrinking, the Fed could pause in the interest rate cycle. The initial scenario that this suggests may be a hike in June and September, providing the opportunity is still there, and pausing to slow the reinvestment process, before, (ideally) resuming the rate hikes in 2018. An important caveat that investors need to bear in mind is that the configuration of the Federal Reserve Board of Governors will significantly change over the next 12-15 months. We had been surprised that the Fed’s dots last month did not seem to line up with the rhetoric, but the balance sheet discussion that was aired in the minutes may explain why. |

Economic Events: Canada, Week April 10 - Click to enlarge |

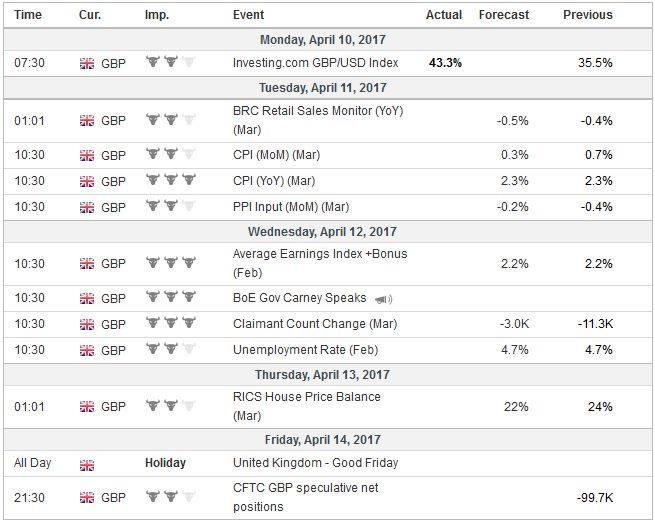

United KingdomThe UK reports on inflation and employment in the holiday-shortened week. Core inflation in the UK is expected to tick down to 1.9% from 2.0%. Headline inflation may slow, but if it does, it will likely prove temporary. The past decline in sterling and the rally in energy prices has not completely worked their way through the system. Inflation has yet to peak in the UK. On the other hand, the labor market remains firm, and the ILO measure of unemployment is expected to be steady at 4.7% in February. The market often pays more attention to the average weekly earnings than to the unemployment rate. Average weekly earnings are expected to be steady at 2.2%, but they appear to be holding up due to bonus payments. Excluding bonuses, average weekly earnings growth is expected to slow to 2.1% from 2.3%. That would be the slowest rise since last July, which itself was the lowest since the end of 2015. Softening wage growth will likely allow the BOE to look past the near-term overshoot of inflation. |

Economic Events: United Kingdom, Week April 10 - Click to enlarge |

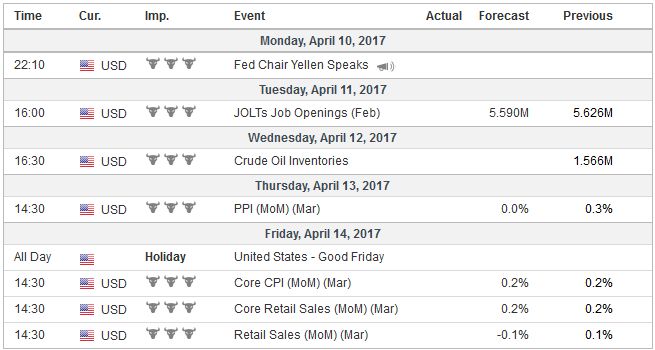

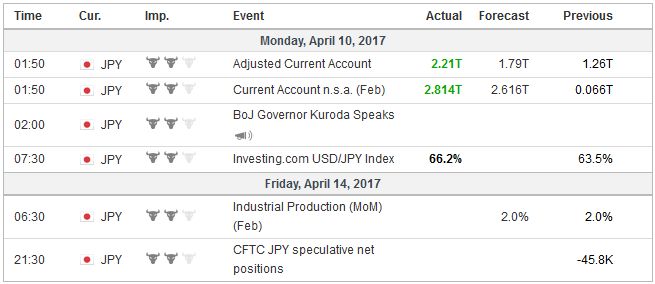

United StatesEconomic data for the US and Europe may not be important drivers. We note that the two most important US data points, March CPI and retail sales, will be reported on Good Friday, which is a holiday for many. The Fed’s March hike means that US Q1 data is of little consequence. Policy is forward-looking, as are investors. A tick down in the pace of CPI and soft headline retail sales, which are expected will simply confirm what investors already know. Price pressures are elevated but not accelerating, and after a shopping spree in Q4 16, American consumers pulled back in Q1 17. The Atlanta Fed’s Q1 GDPNow was halved lasted a week. It now suggests the US economy nearly stagnated in Q1 (0.6% at an annualized pace). However, the NY Fed’s tracker put growth near 2.8% in Q1. Even splitting the difference (1.7%) seems unrealistically high. US 10-year yields (as a proxy for the rate differential) still seems to be the single largest influence on the dollar-yen exchange rate. However, there are a couple of economic reports that are important for investors. First, Japan reports is February current account. February always improves over January. Japan’s surplus is expected to be near JPY2.5 trillion after JPY65 bln surplus in January. In February 2016 it was almost JPY2.4 trillion, and in February 2015 it was nearly JPY1.5 trillion. Still under-appreciated by many, Japan’s current account surplus is driven more by its investment income balance than its trade balance. Moreover, in February, the US Treasury makes a coupon payment, and as of the end of January, US data suggests Japanese investors held $1.1 trillion of US Treasuries. |

Economic Events: United States, Week April 10 - Click to enlarge |

JapanThe strengthening international activity for Japanese companies is boosting capital expenditures and industrial output in Q1. This will likely be seen in the upcoming machine tool orders and industrial output figures. Also, Japanese fund managers had been sellers of foreign bonds and stocks in recent weeks but turned buyers at the end of March. A renewed portfolio outflows can remove one source of the upward pressure on the yen. On the other hand, the anticipation of a weaker yen may encourage foreign investors to return Japanese equities, which underperformed in Q1 (both the Nikkei and Topix have fallen thus far this year while the other G7 markets have risen). |

Economic Events: Japan, Week April 10 - Click to enlarge |

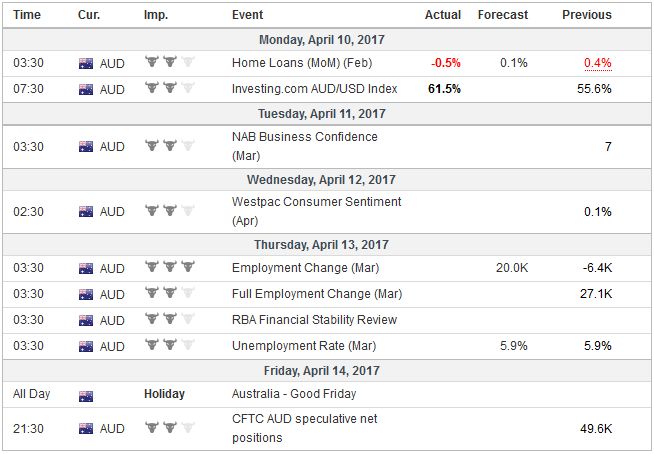

AustraliaLastly, we note that Australia may receive more attention too. The Australian dollar was the weakest of the major currencies last week, falling 1.7% to its lowest level since mid-January. It reports mortgage lending, which probably was flat in February, and credit card usage before the employment report on April 12. The median expectation in the Bloomberg survey calls for a 20k increase in net new jobs Down Under. It would be the most in four months. The unemployment and participation rates are expected to be unchanged at 5.9% and 64.6% respectively. Although speculators in the futures market are still net long Australian dollars, the more recent price action warns of a sentiment shift. The RBA is thought to be one of the few major central banks that could still cut interest rates later this year. |

Economic Events: Australia, Week April 10 - Click to enlarge |

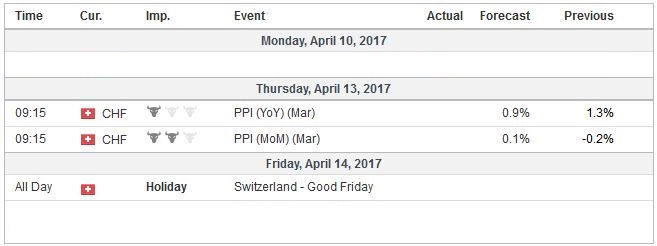

Switzerland |

Economic Events: Switzerland, Week April 10 - Click to enlarge |

Full story here Are you the author?

Tags: #USD,Australia,Canada,Federal Reserve,Greece,IMF,Japan,newslettersent,Russia,U.K.