Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

The Fed is more confident this year of stable growth and rising inflation.

The new US Administration’s economic agenda is beginning to take shape, though it is not clear that consumer interests will be pursued.

There are several considerations, including politics in Europe, that are driving European rates higher.

The RBA and RBNZ meet next week. Neither is expected to change policy.

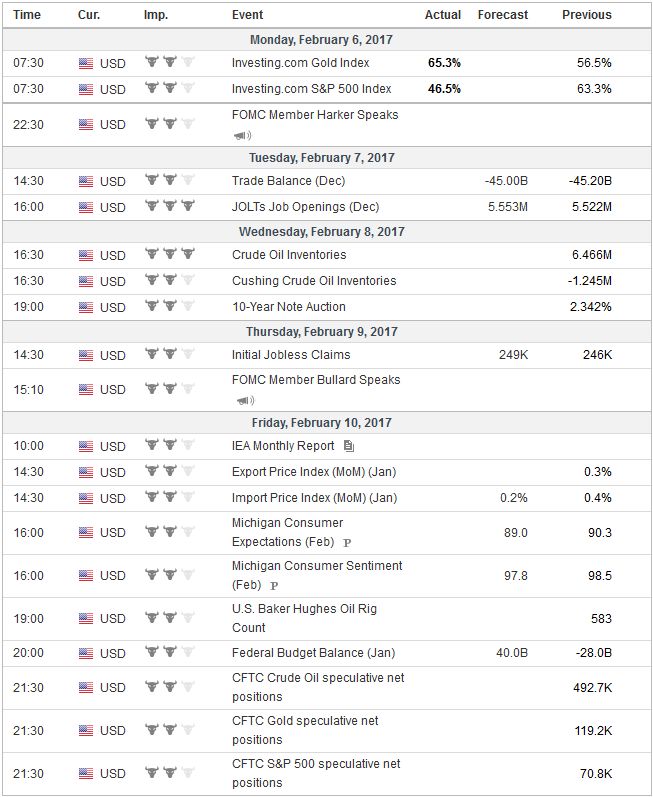

United StatesThe US dollar has been correcting lower since mid-December. Interest rates have begun moving in the dollar’s favor, and the equity market is again knocking on record highs. The US economic data, coupled with Fed comments, keep the Fed on track to hike rates. Even with the weaker than expected wage growth in January, investors saw a greater chance of a June hike. Yellen has warned of a “nasty surprise” if the Fed waits too long, and even the dovish Chicago Fed President Evans seems endorsed two, and possibly three hikes this year. This year is different than 2015 and 2016 when the Fed hiked rates in December both years. The Fed is more confident of the underlying resilience of the economy and more sure that price pressures will continue. In December, the FOMC statement said that “…inflation is expected to rise…” Last week the FOMC statement said that “…inflation will rise…” The five-year breakeven (conventional yield minus the yield on the five-year inflation protected security) closed above 2% for the second consecutive week. A year ago it was a little more than 1%. The 10-year breakeven has closed above 2% for four consecutive weeks. It is approaching 2.10%, the highest since September 2014. The US economic calendar turns lighter next week. However, after a disappointing first estimate for Q4 16 GDP, the typically more conservative NY Fed GDP tracker is pointing to 2.9% growth in the current quarter. The Atlanta Fed sees the economy tracking 2.3%. The unpredictable nature of the new US Administration, and its seeming willingness to antagonize allies and rivals alike, and making arbitrary judgments, appears to have increased the uncertainty. Although Administration officials articulate pro-growth sentiment, there is a concern that other policies will undermine the investment climate. Still, as the Trump Administration begin turning its attention to its economic agenda, investors’ confidence may be bolstered. Already a group of large exporters, including GE, Boeing and Oracle are forming a lobby to support the border tax. The executive order to review Dodd-Frank signed before the weekend, send the S&P 500 financial index up 2%, with several of the large bank shares rallying the most in three months. However, the focus seems to be on parts of the legislation, like the Volcker Rule that curbs proprietary trading by banks, which were seen a conflict of interests and encouraging risk taking that is ultimately backstopped by taxpayers’ money. Also, the fiduciary rule, which forces financial advisers to put client interest first in managing retirement savings, has also incurred the wrath of the President. These are not the kind of things will help Trump’s supporters or broaden his base. The vice-chair of the House Financial Services Committee sent a pointed letter to Federal Reserve demanding that it ceases and desist from continuing to participate in multilateral financial regulation negotiations, including the Financial Stability Board. The letter is not from the chair of the committee or President Trump. Nevertheless, it is important, and the Federal Reserve will respond, perhaps in the days ahead. Yellen will deliver her semi-annual testimony to Congress in the middle of the month, and this will likely be a key topic. Like other positions Trump is staking out, the claim that US participation in global regulatory efforts is undermining US growth has been made for several years by top US bankers, including JP Morgan’s Jamie Dimon. |

Economic Events: United States, Week February 06 - Click to enlarge |

EurozoneGiven the recent ECB and BOE meetings and preliminary estimates for Q4 16 GDP, data from December are unlikely to move markets. Investors seem to focused on three things: Brexit, European elections, and the sharp rise in European interest rates and expanding premiums over Germany. UK Prime Minister May is widely anticipated to formally trigger Article 50 next month and begin the two-year negotiation process. Meanwhile, the next month’s Dutch elections are not drawing the same attention as the French election even though the populist-nationalist forces seem stronger. It is still the early days, but there does appear to be a reasonably good chance that a coalition government in the Netherlands excludes the Freedom Party, even if it gets a plurality of the vote. Le Pen is likely to lose in the second round of the French elections. In Germany, the CDU and SPD are most likely to for another coalition government, with Merkel as Chancellor. The AfD are barely drawing one in nine voters. |

Economic Events: Eurozone, Week February 06 - Click to enlarge |

United KingdomIn France, Fillon, who had been the leading candidate to meet Le Pen in the second round has been undermined by a scandal in which he hired family members as advisers with lucrative salaries. Macron, the former Socialist who broke away to form his own centrist party, is on the ascendancy. As it stands now, it appears that the populist-nationalist shift in the UK and the US is seeing support for the EU rising in Europe. It is forcing liberal (in the European sense) global elites to offer a better defense of their vision and forging a bulwark against the spread of populism-nationalism. |

Economic Events: United Kingdom, Week February 06 - Click to enlarge |

GermanyRising peripheral yields stem from at least a couple factors, including stronger world growth, higher inflation in Europe, and political concerns. Peripheral yields are often like high-beta Bunds. In a falling interest rate environment, the spreads tend to narrow, and in a rising rate environment, they typically widen. There does appear to be some preliminary evidence of a readjustment of portfolio flows within Europe which favor Germany. What has been lost in some of the recent criticism of Germany and the euro by the new US Administration is that while the euro may be too weak for Germany, it may be too stronger for large parts of South Europe and France. Also, the competitive strength of Germany is not appreciated. German exporters can be competitive with a stronger euro, but many other countries would not. And in a weak euro environment, German companies can take market share or boost margins. German retail sales fell a little more than 1% December from the year earlier. The best way to address the large German surplus is not through a zero-sum foreign exchange adjustment but through stronger domestic demand in Germany through investment and stronger wage growth. Although the German government is correct in noting that these are private sector decisions, it is somewhat disingenuous in that government policy can create the proper incentives structure to increase the likelihood of the desired outcome. |

Economic Events: Germany, Week February 06 - Click to enlarge |

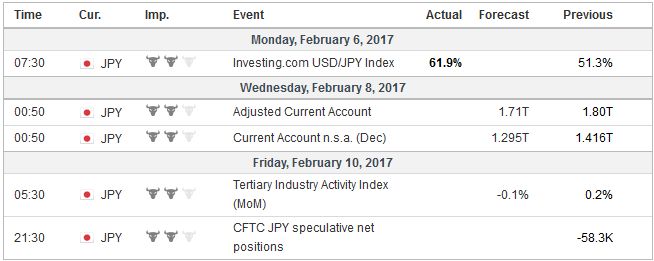

JapanThe highlight from Japan will be its December current account balance. There is a large seasonal component. The December balance is typically worse than the November balance. In fact, this has been the case for eight of the past 10 years. The pattern is expected to hold. The December surplus is expected to fall from JPY1.415 trillion to JPY1.183 trillion. However, the details may be more interesting. The trade surplus typically grows in December and is expected to do so again. The Bloomberg median expects a JPY751 bln BOP trade surplus after a JPY313 bln in November. What will likely hold back the large balance is investment income, which often tapers in December. Elsewhere, we note that both the Reserve Bank of Australia and the Reserve Bank of New Zealand hold policy meetings in the week. Neither central bank is expected to change rates. The recent strength of their respective currencies may draw some attention. The improvement in terms of trade can be eaten away by continued currency appreciation. However, with buoyant housing markets, the central banks will be reluctant to ease policy, especially when global growth prospects have improved. |

Economic Events: Japan, Week February 06 - Click to enlarge |

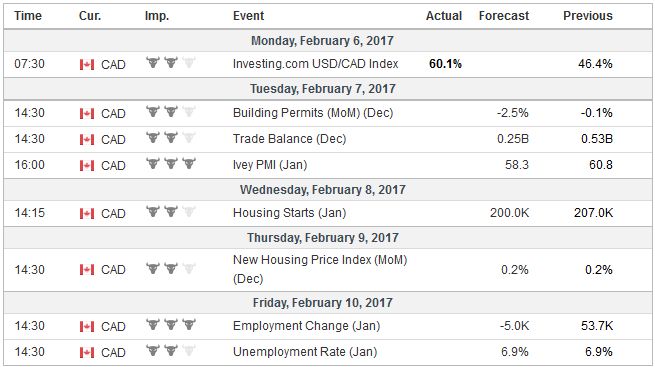

CanadaCanada reports December trade figures and January employment data. In November, Canada reported its first monthly trade surplus in a little more than two years. Higher energy prices may have helped offset a pullback in other exports after a 4.3% increase in November. The risk is for some payback in the employment report as well. Recent job growth has been strong. In the last five months, Canada created roughly 200k jobs. This would be as if the US created two mln, which is a little more than twice the reported pace. There is some risk that Canada’s jobs growth is overstated and maycorrectlower. |

Economic Events: Canada, Week February 06 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week February 06 - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Interest rates,newslettersent,NZD