Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

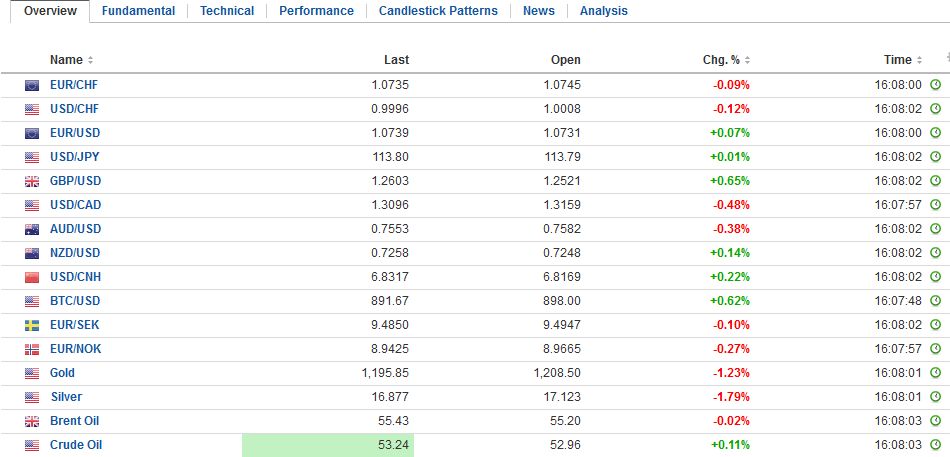

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 25(see more posts on EUR/CHF, ) Source: Investing.com - Click to enlarge |

GBP/CHFThe pound is higher against the Swiss Franc as we finally get some clarity over just what Brexit means. The pound was initially expected to fall but contrary to popular expectation it found favour as Theresa May finally delivered some clarity over just what Brexit means. Most analysts are expecting sterling will come under pressure again, in some respects this is just the beginning of what is going to be a long journey. I think if you are buying Francs in the short term current rates above 1.25 are well worth considering although longer purchasers might be more interested to target a higher price. Most analysts have been expecting the pound to struggle and with a basic level of uncertainty removed the pound has found favour. Problems ahead for the UK to overcome include the prospect of a Scottish Referendum, challenges in parliament and the House of Lords. There are also some other outstanding legal cases over Brexit but none with quite the weight of the Supreme Court case so far. Brexit is expected to now go ahead and the bill to trigger Article 50 could be well under motion very soon with Article 50 potentially being triggered as expected by the end of March. All in all if you have a transfer to buy Francs the pound is likely to remain susceptible to shocks so nothing should be taken too much for granted.But the mood on the pound has changed and this has presented some good fresh opportunities to buy Francs which might well extend to later in the year ans the initial shock factor of Brexit wears off. |

GBP CHF - British Pound Swiss Franc, January 25(see more posts on GBP/CHF, ) Source: Investing.com - Click to enlarge |

FX RatesThe US dollar is softer against nearly all the major currencies. Participants appear to be growing increasingly frustrated with emerging priorities of the new US Administration. They want to hear more details and discussion of the tax reform, deregulation, and infrastructure plans. However, the priority today is on authorizing the construction of a wall between the US and Mexico and possible action on immigration from “terror-prone” countries, according to press reports. |

FX Performance, January 25 2017 Movers and Shakers Source: Dukascopy - Click to enlarge |

| Sterling is the strongest of the major currencies. Having reached almost $1.26 today, it is at its best level since December 14, when the Fed hiked rates for the second time in the cycle. After an initial wobble, sterling recovered smartly after the Supreme Court’s decision yesterday requiring a both chambers to vote on a bill to trigger Article 50. The general sentiment appears to be that while different amendments will be submitted, the small Tory majority may be sufficient to frustrate the most dramatic proposals, such as having a second referendum on the entire deal.

|

FX Daily Rates, January 25 - Click to enlarge |

| We anticipated that the court ruling would prove anti-climactic and that sterling was poised for additional near-term gains. Yesterday’s knee-jerk reaction saw sterling fall to test the trendline drawn off the early September and December highs, and the neckline of a possible head and shoulder bottom pattern (~$1.2425 and $1.2415 respectively) and recover to close on its highs. And today, follow through buying has lifted it further. The intraday technical readings are stretched. A support band between $1.2500 and $1.2550 may be sufficient to deter sharper losses. |

FX Performance, January 25 - Click to enlarge |

AustraliaOn the other hand, the Australian dollar is the weakest of the majors, being the only one lower against the dollar. It is off about 0.6% after a disappointing CPI report. To frame the issue, recall that the Australian dollar fell in each of the last three months of 2016, and four of the last five months. However, this month has been a different story. It is the strongest of the majors, gaining around 5% coming into today’s session. The Q4 CPI miss was not major, but it has spurred talk that the central bank could cut rates again, with some thinking as early as next month. Consumer prices in Q4 rose 0.5% instead of 0.7% as it did in Q3 and as the median forecast in the Bloomberg survey had expected. The year-over-year pace was 1.5% up from 1.3%, but just off the 1.6% anticipated. The trimmed mean and weighted median were also 0.1% less than expected. While the RBA cannot be pleased with the sharpness of the Australian dollar’s appreciation, we have not convinced the miss on Q4 CPI is sufficient to push the central bank into another rate cut. |

Australia Consumer Price Index (CPI) YoY, Q4 2016(see more posts on Australia Consumer Price Index, ) Source: Investing.com - Click to enlarge |

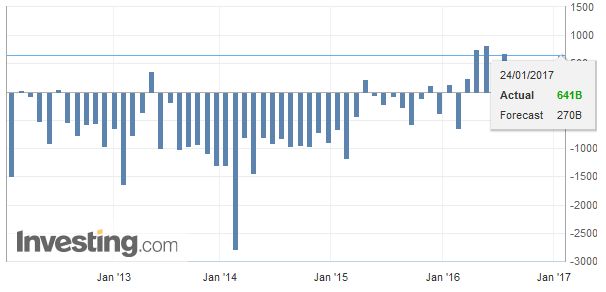

JapanDespite firm US yields after yesterday’s seven basis point increase in the US 10-year yield yesterday, and rising equities, the dollar is practically flat against the yen. Earlier, Japan reported a larger than expected December trade surplus (~JPY641.4 bln, more than twice the Bloomberg median). The December trade balance is nearly always better than November’s but what stands out is that jump in exports. |

Japan Trade Balance, December 2016(see more posts on Japan Trade Balance, ) Source: Investing.com - Click to enlarge |

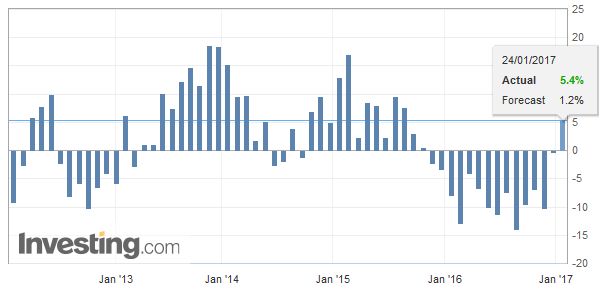

| The 5.4% rise year-over-year is nearly five times larger than expected and snaps a 14-month contraction. Of note, exports to the US rose 1.3% from a year ago, while exports to the EU were off 4%. The big story is the 12.5% jump in exports to China, its largest trading partner. On a value basis, exports of auto parts and electrical circuits each rose 38%. |

Japan Exports YoY, December 2016(see more posts on Japan Exports, ) Source: Investing.com - Click to enlarge |

| The contraction of imports continued. The 2.6% decline year-over-year was larger than expected, though it is the smallest contraction since first going negative at the start of 2015. The combination of stronger exports and weaker imports allowed Japan to report is fourth consecutive trade surplus. It may spur economists to revise up Q4 GDP forecasts, and turn more optimistic on Q1 17. Both the Topix and Nikkei rose for the first time this week. The 1.0% and 1.4% respective gains were the best since January 4 the first trading session of the year for Japan.

The Japanese equity gains were part of the regional rally after the US S&P 500 rose to new record highs yesterday. The MSCI Asia Pacific Index rose nearly 0.5% to record its highest close since late September. Led by financials and industrials, European shares are rallying as well. The 1% gain of the Dow Jones Stoxx 600, if maintained would be the largest since the day before the Fed hiked last month. The gap higher today suggests the nearly monthly long correction after a 5.7% rise in December. |

Japan Imports YoY, December 2016(see more posts on Japan Imports, ) Source: Investing.com - Click to enlarge |

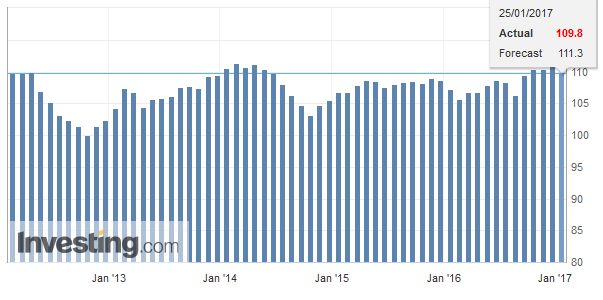

GermanyThe German IFO disappointed, but the market reaction was minimal. |

Germany Ifo Business Climate Index, January 2017(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

| Essentially the assessment of the current situation improved slightly, but the expectations components softened. |

Germany Current Assessment, January 2017(see more posts on Germany Current Assessment, ) Source: Investing.com - Click to enlarge |

| This combination weighed on the business climate measure (109.8 vs. 111.0), which is still at elevated levels.

While we continue to think that the euro’s upside correction may be in its final stages, it does look poised to push higher first. A retest of yesterday’s high near $1.0775 seems likely. The next technical objectives are in the $1.0820-$1.0850 area. Support is seen near $1.07. |

Germany Business Expectations, January 2017(see more posts on Germany Business Expectations, ) Source: Investing.com - Click to enlarge |

United States

The US and Canada’s economic calendars are light, offering a little distraction from political events. Although it may not be a market-mover, global investors will be watching for the Italian court ruling on Italy’s political reform (lower chamber only), and are sensitive to the implications for the timing of the election. The 5-Star Movement is running neck-to-neck with the PD, even though problems in the local government in Rome, which it leads, raise questions of whether it has succeeded becoming a governing power rather than simply an opposition force.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$EUR,$JPY,Australia Consumer Price Index,EUR/CHF,gbp-chf,Germany Business Expectations,Germany Current Assessment,Germany IFO Business Climate Index,Japan Exports,Japan Imports,Japan Trade Balance,newslettersent