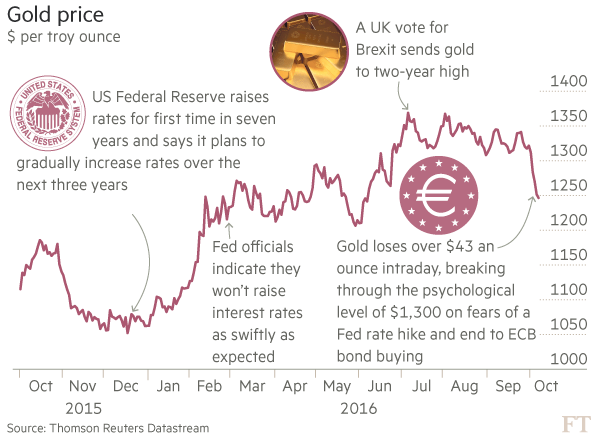

A Strong First Half of the Year, Followed by Another RetreatIn early 2016 gold had a big bull run. The precious metal rose close to 25% this year, pushed higher in a summer rally that peaked on July 10th. Gold experienced a bumpy ride over the remainder of the summer though, as investors became increasingly concerned about a potential rate hike by the Federal Reserve. Uncertainty returned to gold market and has intensified further since then. |

Gold Price(see more posts on gold price, ) Initially, gold rallied sharply in 2016, but then retreated again in the second half as concerns over Fed rate hikes and the impact of Mr. Trump’s election victory have pushed bond yields and the US dollar up in the short term. - Click to enlarge |

Trusting the Establishment a Bit Too Much?Investors cannot be blamed for their skittishness, considering the misleading information released by officials. Fed chair Janet Yellen stated at the Jackson Hole meeting of central bankers that the case for rate hikes had “strengthened”, yet she gave markets little guidance on timing, saying that rate hikes would be “gradual” and happen “over time”. This probably discouraged investors from buying gold, because they still trust the establishment and consider the Fed to have credibility. A rate hike offers investors an alternative to owning gold, as gold doesn’t pay interest. Higher interest rates also tend to dampen price inflation – which is held to be negative for the gold price as well. But surprise, surprise! The Fed then decided the time was not yet right for a rate hike after all. The initial market reaction seemed to indicate that demand for bullion was about to revive: the gold started to rise again after the Fed’s decision to refrain from a rate hike, the dollar weakened and further monetary stimulus was implemented in Europe and Japan. However, these are all market considerations involving short term trading tactics. This is indeed a valid and effective approach, but gold is far more than just a short term trading vehicle. We encourage investors to consider the bigger picture and to ponder gold’s long-term appeal, instead of merely focusing on short-term gyrations in reaction to the Fed’s interest rate decisions. |

There is still a lot of faith in the omnipotence of our vaunted central planners – it won’t last. Cartoon by Bob Rich - Click to enlarge |

A System in Danger of FailingWe and many others have repeatedly warned our readers of the potential failure of the system due to the damage inflicted by the extreme expansionary monetary policies central banks have adopted. The additional money that is constantly pumped into the economy and markets ultimately poses a grave danger to systemic stability. Central banks are now essentially in a lose-lose situation: prolonging the current low/negative interest rate environment will only expand credit and asset bubbles further and ultimately have a disastrous impact on the economy. On the other hand, raising rates will undoubtedly precipitate a severe recession as well. They will surely try their best to avoid this, but it is an inevitable outcome. As the Austrian School of Economics warns, the longer one waits with abandoning a credit expansion, the worse the eventual fallout will be. The economy already seems to be dying a slow death. The Fed’s recent decision to once again postpone its long planned rate hike certainly shows that the central planners have similar concerns. Recent and upcoming events pose considerable political and economic risks, with the outcome of the US presidential election being the most important. After Donald Trump’s surprise victory, it remains to be seen what his economic policy priorities will actually consist of, but among other things, he seems set on increasing government spending. What does his victory mean for gold? Ahead of the election Citigroup’s analysts opined that “a Trump win will bring about higher volatility in gold and forex”. They painted a bullish scenario, in which gold was predicted to rise to USD 1,425 in Q4 2016. This short term call has turned out to be wrong so far, but if the markets are correct in their assessment that Trump’s victory will boost price inflation, the medium to long term prospects for gold certainly remain bullish. Apart from the U.S. election, there are still other potential risks lurking this year, even though they may not be making headlines in the mainstream media. For one thing, Russia apparently wants to transition its currency away from the dollar. Russia’s government wishes to disengage from the US dollar based monetary system by adopting a “national sovereign currency”, with the aim of supporting the ailing Russian economy by severing the link between the ruble money supply and Russia’s foreign exchange reserves (the so-called Stolypin group plan). Meanwhile, China has joined the International Monetary Fund’s special drawing rights (SDR) basket on October 1st. As a part of this basket of reserve currencies, the Yuan is on a par with the U.S. Dollar, the Euro, the Yen and British pound. This represents a milestone for China: not only has it been recognized as a global economic power, but central banks will now start to add yuan-denominated assets to their reserves. Given that additional alternatives are now available, the popularity of treasury bonds could decline. Dollars could circulate back into the US economy, generating additional price inflation pressure in the U.S. Such a development should eventually also put pressure on the US dollar, and the Fed will then no longer have the luxury to just print money at will. A weaker dollar traditionally translates into rising demand for precious metals, which would boost the gold market’s bull run. Recent events and data suggest that the dollar will remain strong in the near term and accordingly put pressure on gold prices. One should look beyond that though and consider the longer term implications of the developments discussed above. |

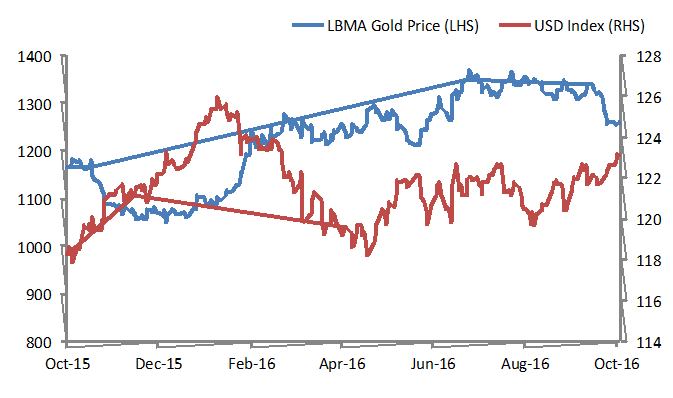

Gold Price vs USD Index The gold price is weakening in the short term as the U.S. dollar appreciates. The dollar’s recent strength is likely to be a temporary phenomenon though. - Click to enlarge |

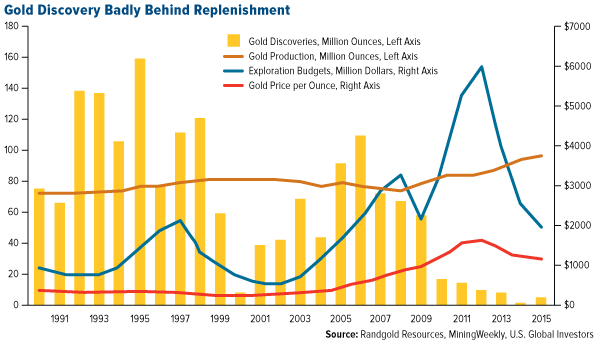

Newly Mined Gold Supply Set to Reach Peak by 2019Apart from the demand for for gold, we also need to look at the other side of the equation: the supply. The industry is facing a developing supply crunch, which could lead to a peak in gold production quite soon. According to Randgold Resources CEO, Mark Bristow, “peak annual gold production may be reached within the next three years as miners fail to replace their reserves”. As the chart below illustrates, this supply crunch is caused by a lack of new discoveries due to tighter exploration budgets. As Bristow moreover points out, mining companies are high-grading to improve their cash flows in the short term, which will inevitably shorten the lifespan of their mines. Production at Barrick Gold, the world’s largest producer, declined by 7.5% in Q2 2016 compared to the same quarter in the previous year. Similarly, production at Anglo Gold Ashanti Ltd., the third-largest gold mining group, declined by 12% in the first half of 2016. Due to gold’s very high stock-to-flows ratio, the impact of declining mine production on prices will generally tend to be small. If gold demand is boosted by macro-economic developments though, it could add momentum to a price rally, not least because it will affect market perceptions. |

Gold Discoveries Gold discoveries are severely lagging behind reserve replacement needs. The impact of mine production on gold prices should be quite limited, but it may well affect market perceptions once the bull market resumes. - Click to enlarge |

The Bigger Picture: Gold as a Backup PlanWe believe the picture couldn’t be clearer: as the extreme monetary policy experiments of central banks continue to fail in achieving their objectives, a vicious cycle has developed. Why are the authorities not putting an end to this downward spiral? Their strategies seem to be mainly focused on avoiding short term pain while maintaining the illusion that they have everything under control. |

The central bankers: purveyors of Kool-Aid. Cartoon by Bob Rich - Click to enlarge |

| Central banks continue to find justifications for the “need” to keep loose monetary policy in place. The Fed attributed its recent decision to once again postpone a rate hike to low consumer price inflation.

The question is how valid these price inflation data actually are. The next chart shows a comparison of today’s annual CPI rate of change with the consumer price inflation rate calculated according to the methodology used in the 1980s (chart by Incrementum based on Shadow Stats data). The chart shows that while price inflation averaged 2.7% per year according to current CPI calculations, it amounted to an average rate of 7.6% according to the old methodology employed by Shadow Stats. Even though the latter is probably an exaggeration, the extremely wide gap shows that there has been a strong incentive to make price inflation appear to be as low as possible (there are many reasons for this, but a very important one are inflation-linked non-discretionary government expenses, which have been lowered significantly by the change in calculation methodologies). It wouldn’t be surprising if the Fed were to hike rates, only to cut them again shortly thereafter. It has opted to play it safe for the moment by keeping rates unchanged, but at the moment it seems highly likely that another rate hike will finally be implemented in December. This will provide the Fed with a little bit of additional room to cut rates later on. Presumably the Fed wants to avoid ending up in the same controversial situation the ECB finds itself in at the moment. The imposition of negative interest rate policies is meeting with a growing backlash – banks and other financial market participants as well as the public at large are increasingly opposed to this unsustainable policy. |

Price Inflation(see more posts on Price Inflation, ) Official CPI inflation rate vs. Shadow Stats inflation rate (y/y) – it seems likely that neither rate “correct” (note that it is actually not possible to measure the mythical “general level of prices”), but even if the truth is somewhere in the middle, we are left with a considerable gap between reality and officially sanctioned illusion - Click to enlarge |

| The monetary policies currently in place are designed to produce currency debasement and further debt accumulation, which will only prolong the economy’s agony. Meanwhile, economic productivity remains under great pressure and the economy’s structural integrity is increasingly in question.

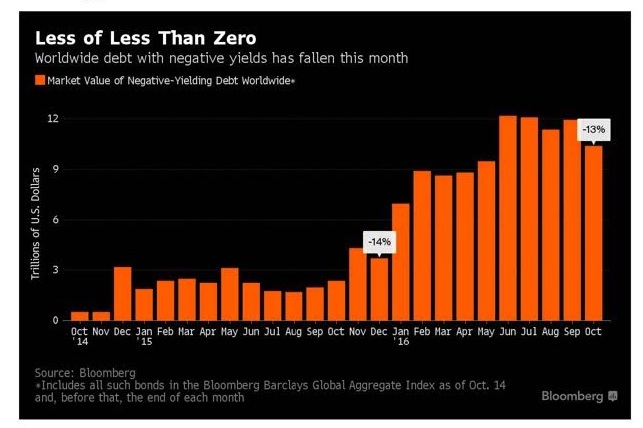

According to Merrill Lynch, until shortly before the recent bond market correction, around USD 13 trillion of sovereign bonds outstanding world-wide had negative yields to maturity, while about three quarters of sovereign bonds traded at yields of 1% or lower. |

Negative Yield Debt Sovereign debt with negative yields-to-maturity, in USD trillion - Click to enlarge |

| Amid this chaotic environment, we have also seen the emergence of major cracks in the banking sector: Deutsche Bank is facing severe difficulties after the imposition of a USD 14 billion fine by the U.S. Department of Justice to settle claims arising from the bank’s mortgage lending activities in the US during the housing bubble.

Could this mean that Germany’s largest lender will have to be bailed out? According to the EU’s new bank resolution legislation, the government is actually not allowed to do that. Alas, “banks in Europe are still choked with some €900 billion euros in bad debt left over from the last financial crisis”, according to Peter Dattels, the IMF’s markets and capital markets deputy director. Apart from the troubles faced by Deutsche Bank, banks in Italy are holding more than a third of these non-performing loans, while Italy’s government is under enormous pressure due to an upcoming constitutional referendum that it will likely lose. All of this has the potential to deeply impact the already weakened European economy and could well lead to another euro currency and debt crisis. |

Deutsche Bank(see more posts on Deutsche Bank, ) Deutsche Bank’s share price over the past 20 years. Evidently, the company isn’t exactly doing well at the moment - Click to enlarge |

Conclusion

While many market participants will keep looking for clues in FOMC statements, one’s investment decisions shouldn’t be based on questions such as “will the Fed hike rates next month” or “will there be a short term correction in the gold market” – that is simply superficial and ignores the major fundamental problems the system is facing.

With so many question marks hanging over the global economy, we believe holding gold is of paramount importance. Gold stored in physical form outside the banking system is the only viable form of insurance in this dangerous market environment.

Our case for gold is to consider the long haul. Whether or not there could be another gold market correction is not the issue. We believe gold’s secular bull market has by no means ended. There is probably still a long, long way to go.

Charts by: Thomson-Reuters, Randgold Resources, LBMA, Incrementum, Bloomberg, StockCharts

Chart and image captions by PT

Full story here Are you the author?Tags: central-banks,Deutsche Bank,gold price,Janet Yellen,newslettersent,On Economy,Precious Metals,Price Inflation