Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancThe EUR/CHF remains under the 1.08, the former line in sand for the SNB. CHF is a hedge against an unexpected outcome of the election. |

EUR/CHF - Euro Swiss Franc, November 08(see more posts on EUR/CHF, ) . - Click to enlarge |

FX RatesThe equity markets snapped their losing streak yesterday and are consolidating today. The US dollar is narrowly mixed. The euro and sterling are slightly firmer, but well within yesterday’s ranges. The dollar-bloc is a bit lower, and once again the Australian dollar is struggling to sustain moves above $0.7700. The focus is over course on the US election. In addition to the national contest, a third of the Senate and the entire House of Representatives is up for election. While the media and some politicians warn against voter fraud, the real “rigging” is the legal kind. There are always a few irregularities, but why we can talk of swing states and the high re-election rate of incumbents is not because of illegal fraud, but the legal gerrymandering, which is the drawing of districts for partisan purposes. |

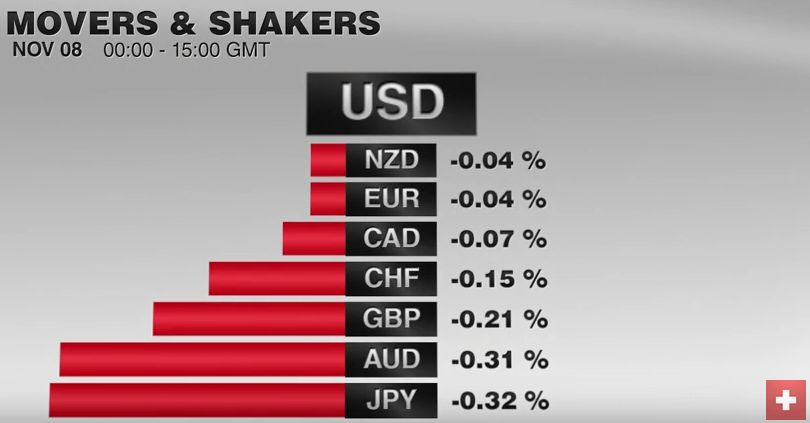

FX Performance, November 08 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| In addition, there is a long history of efforts to dissuade minority voters. The mere fact that the election is held in the middle of the week speaks to an ambivalence toward widespread participation. Many, if not most other countries hold elections on weekends.

Nor should the power of incumbency be under-appreciated. The US House of Representatives reelection rate is higher than the Central Committee of the Chinese Communist Party. The CCP also have term limits, something US legislators do not. Patronage and clientele networks predated communism by thousands of years. |

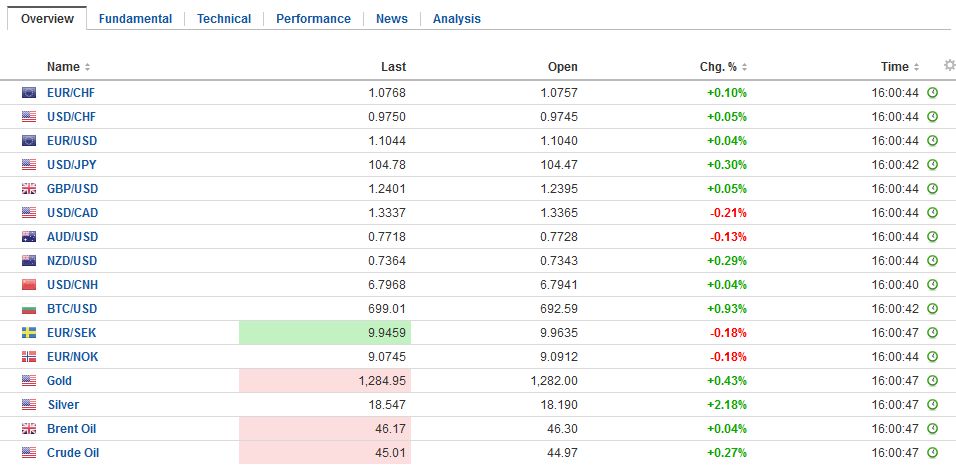

FX Daily Rates, November 08 (GMT 16:00) . - Click to enlarge |

| The die is cast. Despite some media continuing to report a knife-edge decision, the market seems to be fairly confident of a Clinton victory. An as expected outcome would also likely includes a Democrat control of the Senate, even if through the Vice-President as tie-breaker. Such a result would, of course, have considerably less impact than a Trump victory, with the GOP maintaining control of the entire legislative branch.

That said, like modern political parties, the Democrats and GOP are coalitions. The Warren-Sanders wing of the Democrat Party will push for sympathetic nominees and policy. The GOP seems more divided with a burnt-earth wing, a only Tea-Party wing, the old guard (traditional leaders), and the Trump wing. Many commentators are seeing the GOP turn on Paul Ryan as they have the past two GOP speakers. |

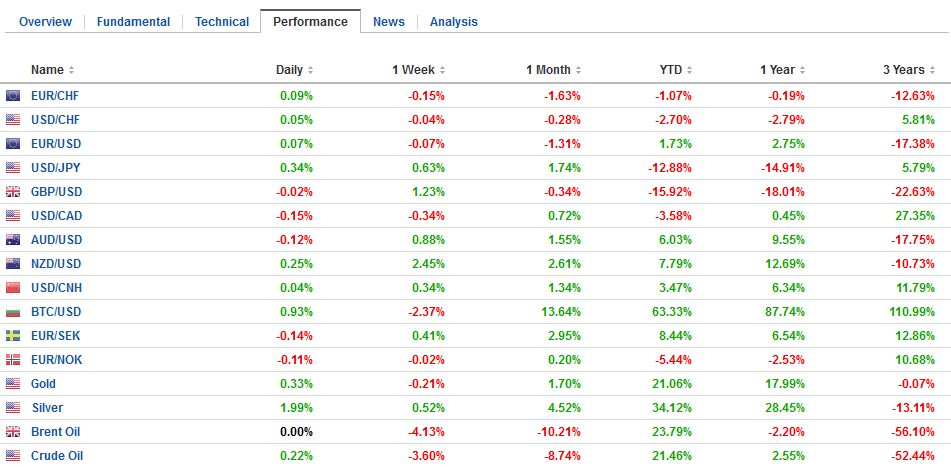

FX Performance, November 08 . - Click to enlarge |

United KingdomSeptember industrial output in the UK fell 0.4%. It is the second consecutive decline of the same magnitude. Outside of a 0.1% gain in July, UK industrial output has not increased since April. |

U.K. Industrial Production YoY, October 2016(see more posts on U.K. Industrial Production, ) . Source: Investing.com - Click to enlarge |

U.K. Manufacturing Production YoY

|

U.K. Manufacturing Production YoY, October 2016(see more posts on U.K. Manufacturing Production, ) . Source: Investing.com - Click to enlarge |

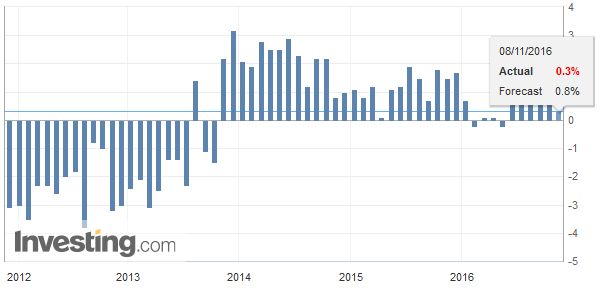

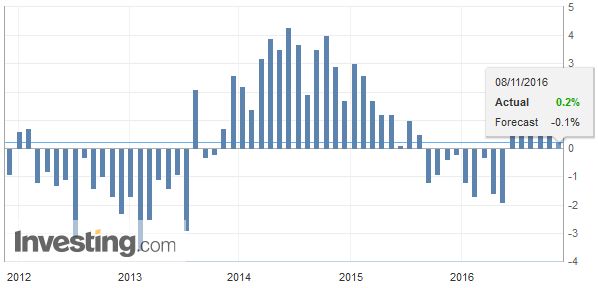

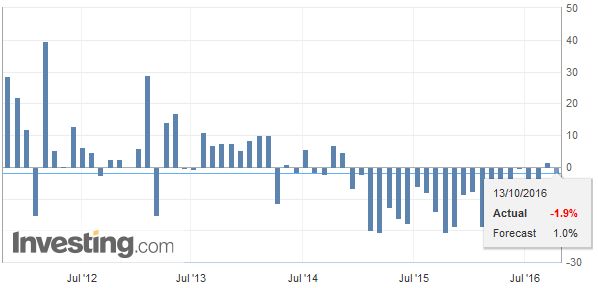

GermanyIn terms of data, the market has a different focus today. Still for the record, note that Germany and the UK reported industrial production. Both were weaker than expected in September. German industrial output fell 1.8%. The Bloomberg median was for a 0.5% decline. The August series was revised to 3.0% from 2.5%. The year-over-year pace was halved to 1.2%. The Bundesbank has already acknowledged that the economy softened in Q3, but there are already preliminary signs of a stronger Q4. The first look at Q3 GDP will be in a week. Most are looking for around a 0.3% gain after a 0.4% pace in Q2.

|

Germany Industrial Production, October 2016(see more posts on Germany Industrial Production, ) . Source: Destatis - Click to enlarge |

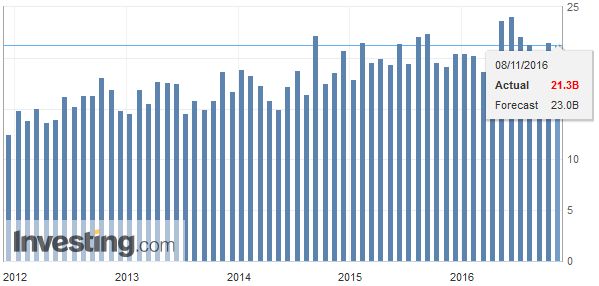

| Two of the world’s large surplus countries, Germany and China reported trade figures. German’s trade surplus rose to 24.4 bln euro from 19.9 bln in August. It is the largest surplus since June well above the 12 and 24-month averages (21.2 bln and 20.7 bln euros respectively). Exports and imports fell after strong gains in August. |

Germany Trade Balance, October 2016(see more posts on Germany Trade Balance, ) . Source: Investing.com - Click to enlarge |

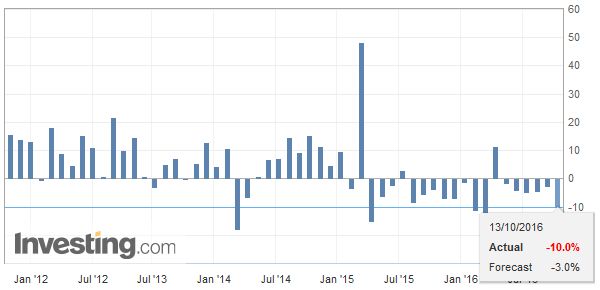

ChinaChina’s trade surplus rose to $49.1 bln from $42 bln in September. Exports fell 7.3%. It is the seventh consecutive months that exports have fallen. Imports fell 1.4% after a 1.9% decline in September. With the exception of the August when imports rose 1.5%. |

China Exports YoY, October 2016(see more posts on China Exports, ) . Source: Investing.com - Click to enlarge |

China ImportsImports have been falling since last 2014. As we saw with the depreciation of the yen, a weaker yuan (~9% over the past 15 months) has not boost exports, as ECON101 would suggest. For the record, exports to the US fell 5.6% in October. Exports to the EU fell 8.7%. Crude oil imports slipped from September’s record. Cooper imports fell to their lowest level since February 2015. The drop in copper imports seems to reflect “import substitution” as domestic output is rising. |

China Imports YoY, October 2016(see more posts on China Imports, ) . Source: Investing.com - Click to enlarge |

| Separately, we note China’s auto sales surged by a fifth last month. It was the eighth month of gains. A key consideration appears to be beating the end of a tax cut on small engine autos. Although the tax cut is slated to expire at year-end, the government is reportedly looking at extending it. Foreign-owned producers are participating. GM deliveries reportedly rose 5.7% and Ford’s deliveries rose 14%. Nissan’s deliveries increased 16% and Honda’s surged 40%. |

China Trade Balance, Otober 2016(see more posts on China Trade Balance, ) . Source: Investing.com - Click to enlarge |

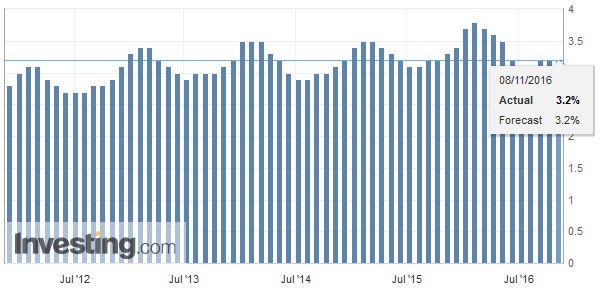

Switzerland |

Switzerland Unemployment Rate, October 2016(see more posts on Switzerland Unemployment Rate, ) . Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$AUD,$JPY,China Exports,China Imports,China Trade Balance,EUR/CHF,FX Daily,Germany Industrial Production,Germany Trade Balance,newslettersent,Switzerland Unemployment Rate,U.K. Industrial Production,U.K. Manufacturing Production