Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancThe EUR/CHF ended the evening at 1.0810. The question is if the SNB was intervening or not. We are convinced that the “new floor” is the area between 1.08 and 1.0850. Hence there should be stronger interventions going on. |

EUR/CHF - Euro Swiss Franc, October 21 2016(see more posts on EUR/CHF, ) . - Click to enlarge |

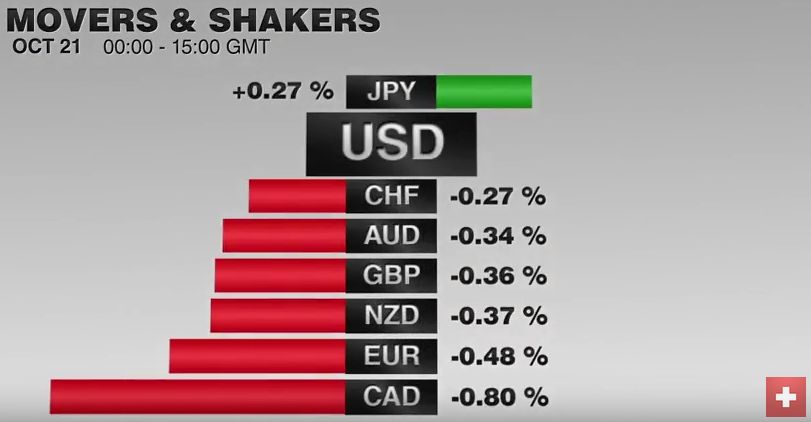

FX RatesThe US dollar is firm especially against the European complex and emerging market currencies. The yen continues to be resilient, and exporters are thought be capping the dollar above JPY104. The dollar is lower against the yen for the fourth consecutive session and set to snap a three-week advancing streak. The euro is extending its push to seven-month lows, after staging a big outside day yesterday, as short-term operators were whipsawed during the ECB’s press conference. As North American dealers return to their posts to close out the week, the euro is trading below the Brexit low. Assuming the euro does recover much ahead of the weekend, this will be the fourth consecutive session that the euro declined. In fact, the euro has fallen in 11 of the last 15 sessions. |

FX Performance, October 21 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Another streak that is continuing is the rally in oil prices. Although oil prices are marginally extended yesterday’s losses, it looks like the fifth consecutive week of gains. The momentum is slowing. In the last week of September, prices rallied nearly 8.5%. In the first three weeks of October, the pace has been 3.25%, then 1.1% and this week 0.5%. Comments from various oil officials, from Saudi Arabia to Russia, Nigeria, and Iran, seem to have contributed to an increasingly cautious stance toward any output freezes or cuts. To lend credence to our sense that oil prices may be rolling over, the December light sweet contract needs to break below the $49.70 area, which is about a dollar lower from prevailing levels. |

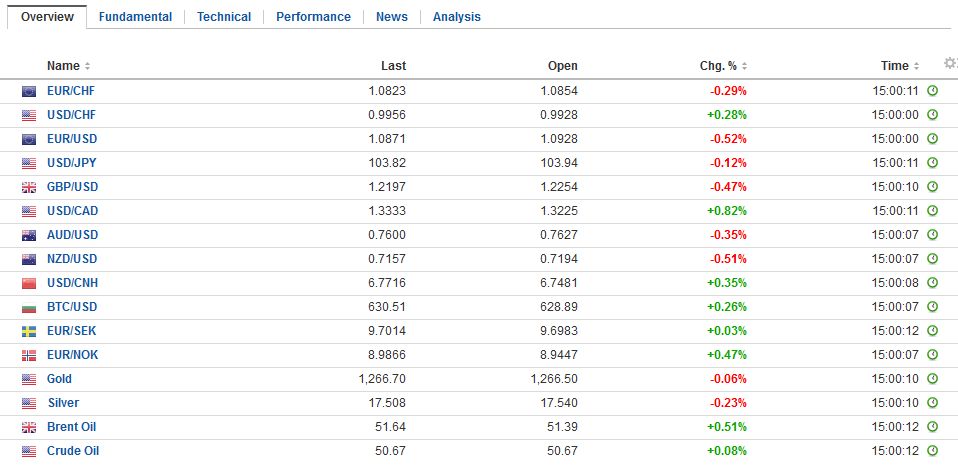

FX Daily Rates, October 21 (GMT 15:00) . - Click to enlarge |

| Equities are closing an ok week on a mixed note. Asian shares were lower. A typhoon closed Hong Kong markets, while an earthquake weighed on sentiment in Japan. The Nikkei still gained about 2% on the week, while the MSCI Asia-Pacific Index rose 1.1%. European shares are mixed, but the Dow Jones Stoxx 600 is trying to extend its advancing streak into a fourth consecutive session. On the week, it is up about 1.3%. The S&P 500 is called lower, and its small gain on the week (~0.2%) is in jeopardy. MSCI Emerging Market equities are around 0.25% off today, paring this week’s gains to about 1.5%. The saw tooth pattern of alternating weekly gains and losses has persisted since the start of September. |

FX Performance, October 21 . - Click to enlarge |

EurozoneThe financial media and some pundits make it sound as if Draghi left investors in a lurch by not acknowledging that the ECB is discussing extending its asset purchases. Yet the market does not seem confused. The ECB is widely expected to extend its purchases beyond March of next year. There seems to be good reason that there is no need for such a discussion now. It is premature, and the sequence is important. The ECB instructed Euro system committees to conduct a technical review of monetary policy. That report is not complete. The staff forecasts need to be updated to make an informed decision about what may be needed going forward. Draghi also provided a strong hint into the criteria. First, he said that the ECB will continue its asset purchase plan until Mach 2017, or until inflation is showing significant progress toward the target. Second, he said that inflation is not yet on an upward trajectory. Third, Draghi said the growth risks were on the downside. Even without being explicit, the only conclusion one can draw from this is that the asset purchases will continue. Many, if not most, expect a six-month extension. Of course, the extension may not enjoy unanimous support. For those who opposed the asset purchases in the first place, it is difficult for them to support an extension. They were a minority then and still look to be in a distinct minority. |

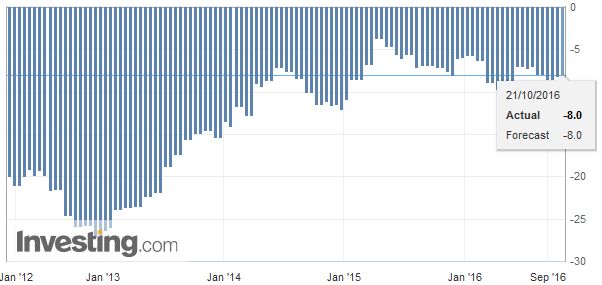

Eurozone Consumer Confidence, September 2016(see more posts on Eurozone Consumer Confidence, ) . Source: Investing.com - Click to enlarge |

United States

Despite higher oil prices and firm, if not higher, inflation readings from the US, UK, China, and Australia, bond yields are lower this week. The US 10-year yield is off a little more than two bp this week, half of which is being recorded in Europe today. European bonds yields are off mostly 4-6 bp. Ahead of the DBRS review later today, Portuguese bonds are firm, with the yield off five bp this week.

The short-end of the coupon curve has been softer, leaving yields mostly firmer. The US premium over Germany on two-year money widened by a single basis point this week, and two basis points over Japan. The premium is unchanged against the UK. The big move was against Canada. There the US premium rose seven bp, widening the spreading by 50%, as the Bank of Canada Governor indicated that easing policy was discussed. That helped offset the impact of the balanced risk profile (changed from downside bias).

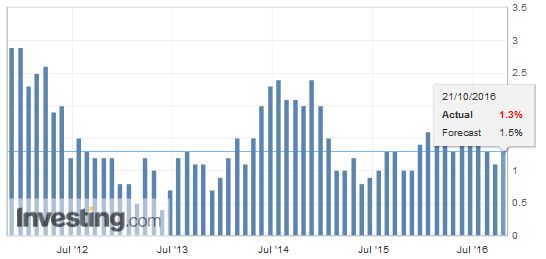

CanadaThere is no US economic data on tap, though two Fed officials speak (Tarullo and Williams). Canada’s August retail sales and September CPI will draw attention. Consumer prices are expected to firm with the year-over-year rate rising to 1.4% from 1.1%, while the core may be flat at 1.8%. |

Canada Consumer Price Index YoY, September 2016(see more posts on Canada Consumer Price Index, ) Source: Investing.com - Click to enlarge |

| Retail sales are expected to rise 0.3%, as they bounce back from a 0.1% decline in July. We suspect the risk is to the downside. |

Canada Retail Sales MoM, September 2016 Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,Canada Consumer Price Index,EUR/CHF,Eurozone,Eurozone Consumer Confidence,FX Daily,newslettersent