Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancThere are bets going around that the Swiss Franc will depreciate further. We do not agree. Today’s PMI data, namely the quite strong German Manufacturing PMI and the contracting U.S. ISM PMI shows that these bets are premature. |

Click to enlarge. |

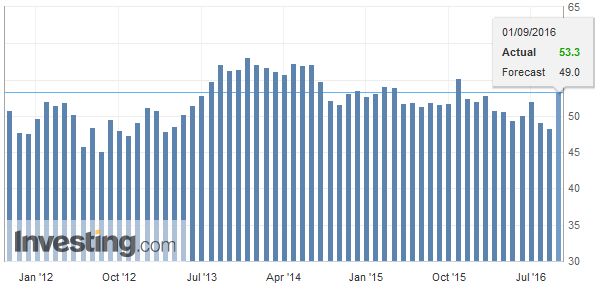

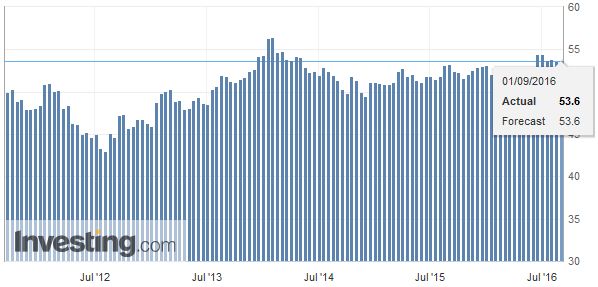

United KingdomThe new month has begun with a couple of surprises. The biggest surprise has been the record jump in the UK manufacturing PMI to 53.3 from 48.3. A much smaller rebound was expected in August after the Brexit shock drop in July. |

U.K. Manufacturing PMI(see more posts on U.K. Manufacturing PMI, ) Click to enlarge. Source Investing.com |

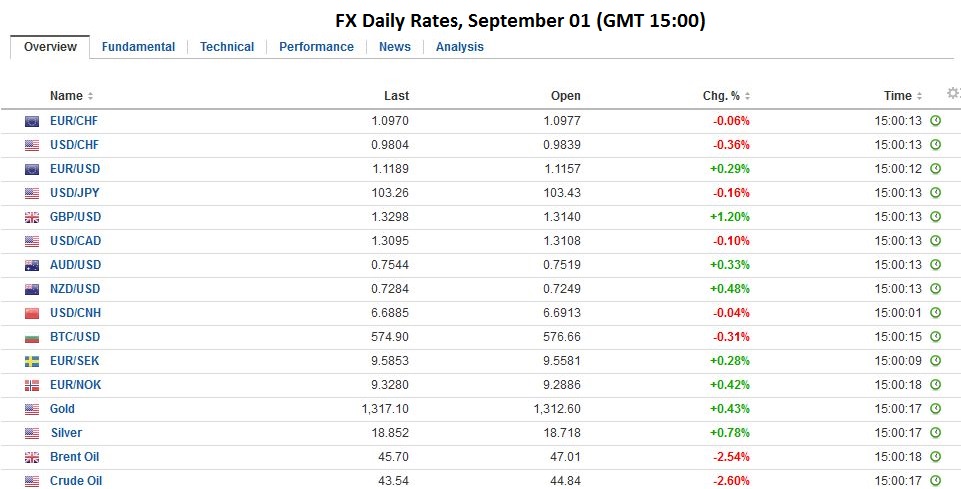

FX RatesThere is a linear type of thinking that appears to be driving the market’s response which was to take sterling a cent higher against the dollar. The idea is that pundits, economists. Many policymakers (including the Bank of England) and investors have bought the hype about Brexit being bad for UK economy. However, this misses the point and misunderstands an important aspect of how markets work. The reason the PMI jumped was driven by the decline in sterling. It is about exports. While the market logic of taking sterling higher on the better than expected news is understandable, from an economic point of view, it blunts a key driver. |

Click to enlarge. |

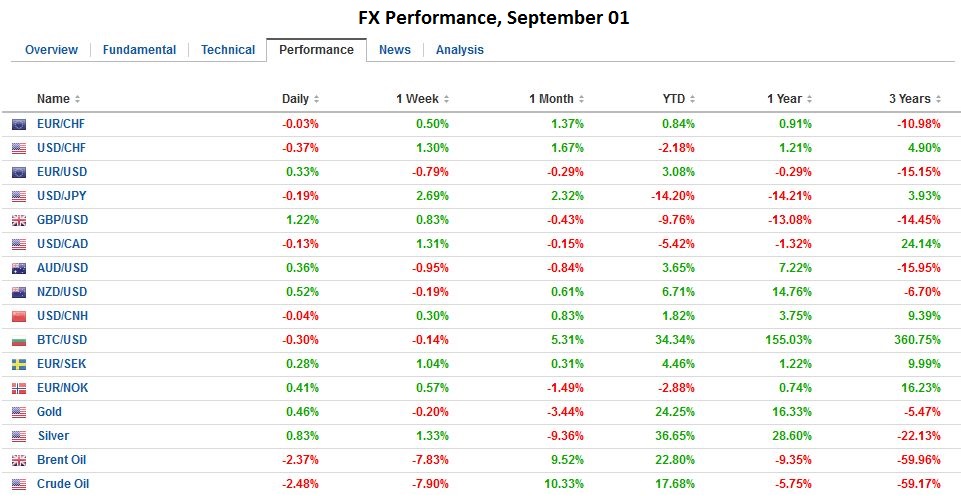

| Two points need to be made. First, when thinking through the impact of a shock event, investors need to consider not just the event, but the market response. This is the kernel of truth in the self-correcting aspect of the market, which may be exaggerated by market fundamentalists. The decline in sterling and UK interest rates will help cushion a potential economic blow, and the short-term cost of which is greater price pressures, which were also evident in the PMI report.

Second, while some observers played up the impact of the referendum on more than market psychology, many, including ourselves, were more concerned about the implications after the divorce for the UK and the future of a medium-sized country with a large current account deficit, reliant on financial services in an era of deleveraging. We also recognized, like many, that business decisions will take the time to filter through. We have compared the issue to cooking frogs rather than frying bacon. Don’t be lulled to sleep by warm water. The risks are that it will still boil. |

Click to enlarge. |

| The immediate hurdle for sterling is near $1.3280 and then $1.3370. Given the spike up on the news, many short-term participants will watch how the pullback unfolds to help determine whether and or where to fade this bounce. The euro fell to test GBP0.8400. The August low was seen near GBP0.8340, which would be the next downside target.

There were three surprises from Asia-Pacific to note. First, the Australia’s manufacturing PMI dropped to 46.9 from 56.4. It is the first sub-50 print and the lowest reading since June 2015. Australia also reported flat July retail sales figures, for which the median forecast was for a 0.3% bounce after 0.1% gains in May and June. However, the Australian dollar was not sold. It is recovering from yesterday’s dip below $0.7500 for the first time since the start of August. The euro has been mostly confined to yesterday’s ranges. We again highlight support in the $1.1110-$1.1125 area, which houses a retracement objective and the 200-day moving average. Resistance is seen near $1.1170. Meanwhile, the dollar is extending its gains against the yen for the seventh consecutive session. If a foothold above JPY103.50 is secure, the market appears to have its sights set on JPY104. Support is pegged just below JPY103. |

Click to enlarge. |

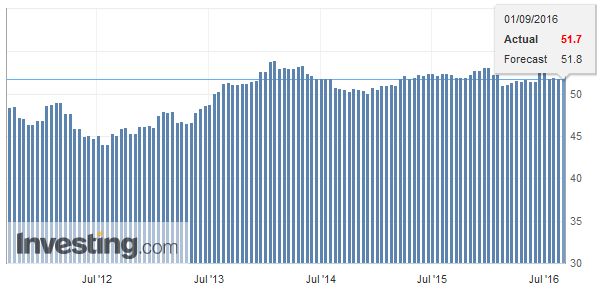

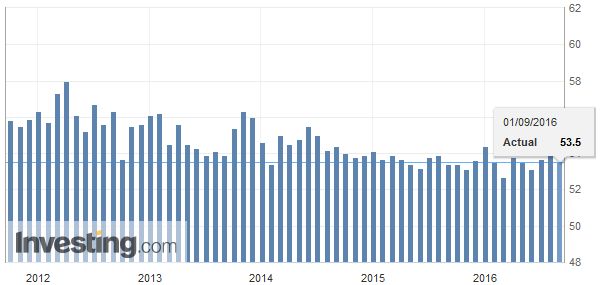

EurozoneThe eurozone surprised today too. Its final manufacturing PMI slipped to 51.7 from 51.8 of the flash reading and 52.0 in July. It is the second consecutive decline. Next week’s service PMI is more important, not just because it is a larger part of the economy, but also because services reflect more domestic rather than international forces. Yesterday’s slightly softer than expected CPI also seemed to reflect weakness in service prices. This is a yellow flag about the economic momentum, which will likely be noted by the ECB next week. |

Eurozone Manufacturing PMI(see more posts on Eurozone Manufacturing PMI, ) Click to enlarge. Source Investing.com |

Germany Manufacturing PMIThe headline disappointment is minor compared with a couple of the country reports. Germany matched the flash reading, so we cannot look to Berlin. France’s manufacturing PMI was revised down to 48.3 from 48.5 flash estimate and 48.6 in July. It has not been above the 50 boom/bust level since February. Italy was even a bigger disappointment. Its reading fell to 49.8 from 51.2. It is the first sub-50 reading since January 2015. |

Germany Manufacturing PMI(see more posts on Germany Manufacturing PMI, ) Click to enlarge. Source Investing.com |

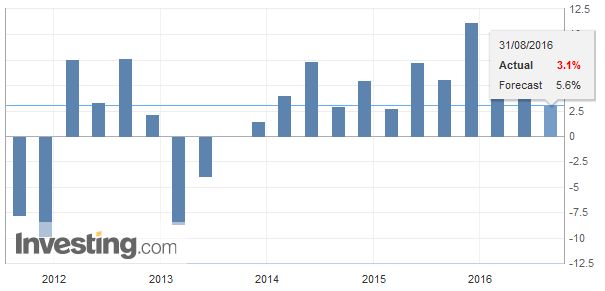

JapanSecond, Japan’s surprise was the weaker than expected Q2 capex figures, which warn of the risk that Q2 GDP is revised lower. Capex was expected to have risen by 5.5% after 4.2% gain in Q1. Instead, it increased by 3.1%. Separately, Japan reported that corporate profits fell 10% in Q2, which is the largest decline since 2011. It was a function of two factors, a 3.5% drop in sales (weaker domestic demand) and the rise of the yen (translation of foreign earnings). |

Japan Capital Spending YoY Click to enlarge. Source Investing.com |

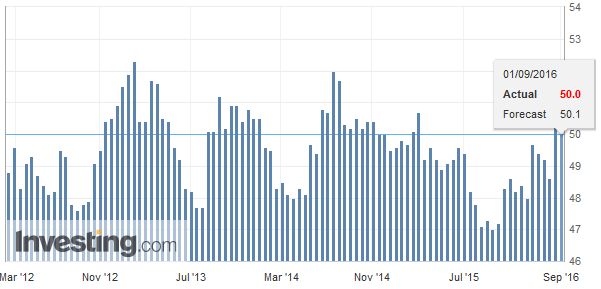

ChinaThird, China surprised. The official manufacturing PMI rose to 50.4 from 49.9. It is the highest reading since October 2014. |

China Manufacturing PMI(see more posts on China Manufacturing PMI, ) Click to enlarge. Source Investing.com |

China Caixin Manufacturing PMIThe Caixin measure, which has a greater weight for smaller companies than the official measure, slipped to 50.0 from 50.6.

|

China Caixin Manufacturing PMI(see more posts on China Caixin Manufacturing PMI, ) Click to enlarge. Source Investing.com |

China Non-Manufacturing PMIThe official services PMI eased to 53.5 from 53.9. It appears that China can host the G20 meeting this weekend and note the economy appears to be stabilizing. |

China Non-Manufacturing PMI(see more posts on China Non-Manufacturing PMI, ) Click to enlarge. Source Investing.com |

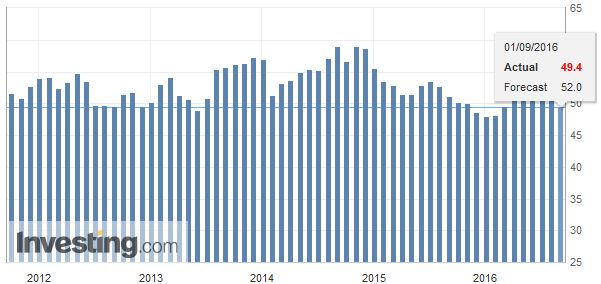

United StatesThe North American session features a full slate of data, but two reports stand out: the manufacturing ISM and the auto sales. Both are expected to soften a bit. The other reports, like Q2 productivity and labor costs, are not typically market movers, though important for understanding the economy and US competitiveness. |

U.S. ISM Manufacturing PMI(see more posts on U.S. ISM Manufacturing PMI, ) Click to enlarge. Source Investing.com |

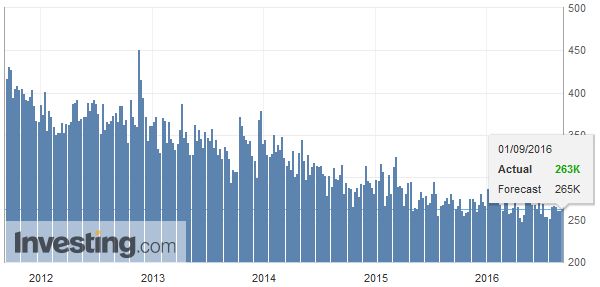

U.S. Initial Jobless ClaimsWeekly jobless claims do not attract much interest the day before the national report. Construction spending is also not a market mover, but an increase in July would snap a three-month drop, and boost confidence that GDP is recovering, and it broadens outside of consumption. |

U.S. Initial Jobless Claims(see more posts on U.S. Initial Jobless Claims, ) Click to enlarge. Source Investing.com |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$EUR,China Caixin Manufacturing PMI,China Manufacturing PMI,China Non-Manufacturing PMI,Eurozone Manufacturing PMI,FX Daily,Germany Manufacturing PMI,Japanese yen,newslettersent,U.K. Manufacturing PMI,U.S. Initial Jobless Claims,U.S. ISM Manufacturing PMI