Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Policy outlook is clear: ECB and BOJ review next month, FOMC still looking for opportunity.

Inventory cycle making quarterly US GDP forecasting difficult, but it looks like re-acceleration still the more likely scenario than recessions.

Why didn’t European bank stress tests results have more impact?

The drip-feed of high frequency economic data from the major economies slows in the week ahead. The data that is reported is unlikely to have much impact on the expectations of policy going forward.

The state of play is fairly straightforward. The Federal Reserve is finding it difficult to take the next step in the normalization of monetary policy. According to Bloomberg calculations, the Fed funds futures strip does not show greater than a 42% chance of a rate hike at any meeting through the end of next year.

Japan

The BOJ and the ECB have signaled a review of their respective monetary stances next month. Neither the BOJ’s increased equity purchases and new dollar lending facility (which could be more important due to changes in the US money markets that impact dollar funding), nor the “fresh water” in Abe’s fiscal plans have impressed investors. There is some speculation that BOJ Governor Kuroda may abandon the 2% inflation target.

We have argued that the target is on the wrong inflation measure (CPI excluding fresh food), and the time frame was too ambitious. It should be a medium-term target or goal. Making it short-term, and the repeated moving it further out, undermines the very credibility and transparency that an inflation target theoretically enhances.

Eurozone

The ECB staff will offer updated forecasts next month. There are two areas that many investors expect action.

First, following the staff forecasts, it will be clear that officials cannot be confident that its inflation target will be approached. Eurozone fiscal policy became a little easier this year as ostensibly to cope with the refugee challenge. It is anticipated to be somewhat less accommodative next year. The 80 bln euro a month of asset purchases may be extended from March until September 2017. This would be the second extension.

Second, the extension of the asset purchases may aggravate the shortage of some securities in the eurozone. Some speculate that the capital key (a function of size of the economy) as the determining mechanism of how the 80 bln euro in asset purchases is distributed among the member may be abandoned. We demur. There are a number of other adjustments that can be made, and we see the capital key as an important principle that is unlikely to be easily eschewed.

United States

When the Fed was engaged in asset purchases, before the ECB or BOJ initiated their program, a popular chart showed the size of the respective balance sheets. It seemed to show that the expansion of the Fed’s balance sheet was weighing the dollar. We were skeptical. Over the past year, the ECB and BOJ’s balance sheets have expanded by nearly 50%, while the Fed’s balance sheet has contracted by 5%. During the period, the yen has appreciated by over 22%, while the euro has risen 1.6% against the dollar. On a real broad trade-weighted basis, which is the most relevant economic measure, is about 3% higher over the past year.

The Fed’s hesitancy in lifting rates is not due to the dollar any more. At first, policymakers were thrown off balance by the shockingly poor May employment report. We argued at the time that a statistical quirk was not uncommon; taking place once a year or so. Of course, confidence in this assessment was only possible because the June and July employment data. The two-month average stands at 274k, which is the highest this year, and above all but two months last year.

More recently, the weakness of Q2 GDP shook confidence. However, investors may be more rattled than policymakers. Our understanding is that the Fed’s leadership tries to focus on the signal and look past the noise. In terms of GDP, the signal comes from final domestic demand, which excludes inventories and net exports, leaving the components of GDP that monetary policy can directly impact.

The main reason that the initial estimate of Q2 GDP fell well short of market and official expectations was due to the continued liquidation of inventories. The strong consumption (4.2%), which was nearly three-times larger than the Q1 increase (1.5%) was met by inventories rather than new output. It was the third consecutive quarterly liquidation, and it appears to have largely run its course.

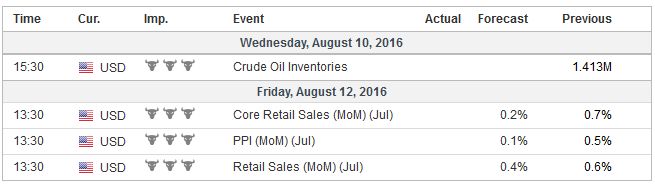

Economic CalendarAt the same time, US consumption appears to have begun Q3 on a firm note. US auto sales rose from an annualized pace of 16.61 mln in June to 17.77 mln in July. Domestic brands accounted for the lion’s share of the increase. It is the strongest sales since last November. The industry figures do not always translate into retail sales, but if they do, there may be upside risks to the median forecast of 0.4% for July, which the US data highlight of the week ahead. The components of retail sales, which are used for GDP calculations, had their strongest quarterly advance in Q2 since Q1 12. After rising 0.5% in May and June, the pace may have slowed to 0.3%. That would match the 12-month average. Still, as we approach the middle of the quarter, the Atlanta Fed’s GDPNow tracker puts Q3 growth at 3.8%, helped by an 8.8% increase in private sector investment. An alternative methodology at the NY Fed puts Q3 growth at 2.6%. Of course, the Atlanta Fed estimate, if true, is preferable, but even under the NY Fed’s less optimistic results, after three-quarters of disappointment, the economy bounces back above trend. Even if we have struggled to anticipate the quarterly pattern of growth, the important point is that the US economy is re-accelerating as the headwinds from oil (on investment, manufacturing, etc.) and the inventory cycle dissipate, and not entering a recession as so many naysayers warned. |

|

Incidentally, a GDP tracker has been launched by the Bank of Italy for the eurozone. The coincident indicator (hence it is dubbed COIN) was updated at the end of July.It estimates Q3 GDP at 0.31%, up from 0.29% in June. The initial estimate of 0.3% in Q2 will likely be confirmed this week.

The US election has moved within the three-month time frame that is important for numerous market participants. The dramatic departure from American tradition and the status quo that Trump’s candidacy represents brings a new level of attention to the contest. Like many, we are surprised that Trump secured the Republican nomination in the first place. While his unorthodoxy may have yielded some advantages in the primaries facing many rivals, his vulnerabilities have been highlighted over the past few weeks.

In the electoral cycle, the situation tends be fluid until around Labor Day, or early September in the US. However, there has been a deterioration of Trump’s support that the national polls only partly reflect. The key is the Electoral College, and a handful of swing states.

When political analysts look at the Electoral College map, Pennsylvania is emerging as a critical state for Trump and, demographically, it is his sweet spot. The state is 20% whiter than the country as a whole, exposed to manufacturing, with a large working class base. Romney lost the state by five percentage points. It is a truism, that for Trump to win he must do better than Romney. Trump is trailing by more than 10 percentage points in a recent poll of likely voters.

Trump’s positions have alienated many Hispanics. This threatens his performance in other swing states, such as Florida and Nevada. Michigan is also an important Electoral College state that Trump needs to win but is slipping further behind Clinton. The gap is now near 10 percentage points. In New Hampshire that was the home to Trump’s significant victory in the primaries, he is trailing Clinton by 15 percentage points.

Nationally, Trump continues to do a few percentage points better than Romney did among non-college educated, especially white men. However, he is trailing Romney by more than twice as much among college-educated whites. Ethnic voters account for a larger share of the electorate than they did in 2012, and Clinton is polling better than Obama. Trump lags Clinton by almost 70 percentage points among these voters. Earlier, the polls that included third party candidates tightened the contest, meaning they took votes from Clinton. This seems to be less the case in more recent polls.

The takeaway is that with the election in three months, it is becoming more difficult to see how Trump will be able to secure the 270 Electoral College votes he needs to become the next president. Although humbled by difficulty in anticipating political (let alone economic) developments, it might make sense for investors not to completely discount the possibility of a Trump victory, but spend more energy on contemplating the policy implications if the Democratic Party can secure the legislative branch, as well. The Senate is possible, if not likely, while the House of Representatives is regarded as more difficult for the Democratic Party, but not impossible.

The legislative agenda of a Democrat in the White House and a Democrat-dominated Congress would be different than what Obama has experienced, for example. There would be budgets and appointment confirmations. The Federal Reserve’s Board of Governors would be fully staffed. Some form of Glass-Steagall could get resurrected, though it is ironic to note that it was in the Bill Clinton’s Administration that Glass-Steagall, which had already been largely gutted was put out of its misery. It would have implications for trade policy. The Federal minimum wage would likely rise.

The Reserve Bank of New Zealand meets in the week ahead. Indicative prices in the derivatives market suggests investors are as confident that a cut rates will be delivered as they were that the Bank of England was going to cut last week. As we saw last with the Australian rate cut, lower rates in high rate countries need not undermine a currency. The Australian dollar was one of two major currencies that appreciated against the US dollar last week (The yen was the other appreciating currency).

The health of European banks continues to be important issue for investors. The IMF identified three European banks it said posed the greatest threat to the global financial stability. The branches of two European banks failed the Federal Reserve’s stress test. The problems at Italian banks, especially Monte Paschi, were seen as more pressing. It was the only bank that failed the recent European stress test. In the past week, the banking index of the Stoxx 600 was flat last week, and the MSCI European bank index rose 0.5% last week. An index of Italian banks fell 6.2%, which includes a 5.5% rally in the last two sessions.

A few hypotheses have been suggested as possible explanations for the reason the stress tests did not seem to make a difference to investors. One is that what ails European banks is not capital cushion needed in an economic crisis. That is to say that the regulators have done their job. They have delivered a more resilient banking system.

Another hypothesis is that the stress tests are largely irrelevant. What concerns investors may not be if banks have sufficient capital to whether a prolonged economic downturn, but if they can survive the grind of the status quo. There is no end in sight of negative interest rates, loan growth is slow, the nonperforming loan problem has barely been addressed, and, arguably, there are too many banks and branches in Europe. But apparently, a deep and protracted economic downturn won’t wipe out their capital.

The stress tests may be irrelevant on another level. Officials stress tested around 50 banks. These are large institutions. These are the ones that have been under pressure to raise regulatory capital, adopt better risk controls, and address governance issues. Surprises do not often arise from where one looks, but from where one doesn’t.

Italy’s bad loan problem is not limited to the five banks that were stress tested. German Landes banks are not seen as systemically significant. Many institutions that failed, including Bear Stearns, may not have been systemically important. A year ago, it was relatively small Greek banks which were not systemically important, that appeared to threaten to bring down the entire EMU.

In the US, the FDIC has helped wind down hundreds of banks, without much fanfare. Accounts up to are insured (up to $250,000), unlike in Europe where the depositor is insured. Early in the Great Financial Crisis, the US did two things, before the forced recapitalization of healthy and weak banks. It raised the deposit insurance cap to $250,000 and allowed small business accounts to be treated like deposits. In effect, the US moved to strengthen the system before reducing risks.

Ultimately, Europe’s problems are symptoms of the failure to complete the banking union. It is caught in a Catch-22. Germany and the creditor nations do not want to move to greater union without first reducing risk in the system. It is proving difficult if not impossible to reduce risk without greater union.

While not discounting the insight of the second hypothesis, there is a third possibility. The simplest and most benign hypothesis is that observers are rushing to judgment. The bank shares did continue to fall in the first couple days of last week but finished with a 2-3 day advance. Let’s see what happens this week. The danger of attributing short-term price action to macro forces is that the price action often reverses before the purported cause are removed.

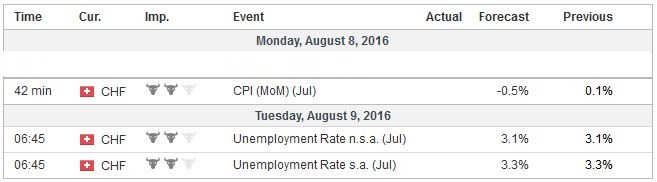

SwitzerlandSwitzerland publishes the CPI today and tomorrow the Unemployment rate. |

Click to enlarge. |

Tags: Banca Monte dei Paschi,Bank of Japan,Bear Stearns,ECB,newslettersent