Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Electoral politics remains significant.

BOE is likely to cut rates, while BoC may tilt more dovishly.

US Q2 earnings season formally begins.

Investors are under siege. A growing proportion of bonds in Europe and Japan offer negative yields. The German and Japanese curves are negative out 15-years, while one cannot find a positive yield among any tenor of Swiss government bonds. Despite a string of robust data, US Treasury coupon yields are at record lows.

Investors are under siege. A growing proportion of bonds in Europe and Japan offer negative yields. The German and Japanese curves are negative out 15-years, while one cannot find a positive yield among any tenor of Swiss government bonds. Despite a string of robust data, US Treasury coupon yields are at record lows.

The UK referendum hit an already vulnerable banking system in the eurozone. Italian banks are on the front burner, but the temperature is rising in Portugal, and this is not to mention the slow boil at some of the largest European banks, specifically singled out by the IMF as posing the greatest systemic risks.

Politics add an additional wrinkle. Both of the two main parties in the UK are divided. The leader of the UK’s Independent Party resigned. If Labour was not doing a fine job of destroying itself, Cameron, in among his last acts as Prime Minister, will give it a helping hand. He will have parliament vote on the renewal of the UK nuclear deterrent (Trident), and it will further split Labour. Corbyn has been long opposed, while the Labour MPs typically favor. There is an attempt by the Labour MPs to block Corbyn’s name from even appearing on the leadership ballot.

The US political parties hold their conventions over the next few weeks, though it is possible that Trump announces his vice-presidential running mate in the week ahead. Indiana Governor Pence appears to be edging out former Speaker of the House Gingrich. Perhaps to prevent the Republican Party to dominate the news cycles, it would not be surprising if Sanders were to endorse Clinton either in the week ahead of the following week.

Eurozone

The Economic Minister in France may declare his candidacy to challenge Hollande in the coming days. Meanwhile, Hollande is going to make a rare television address to the French people next week. Italy is on its third unelected Prime Minister, and even before the next parliament election, the country’s political outlook is deteriorating. If the Italian constitution referendum, scheduled for October, would be held today, it would likely lose, which would incite a political crisis if Renzi resigned as promised. Polls suggest that the anti-EMU (but less hostile to the EU) Five Star Movement is has replaced Renzi’s.

Meanwhile after its second election in six months, Spain still does not have a new government.There are several configurations that could work, but the personalities and programmatic demands are deterring the formation of a government. The political stalemate is paralyzing reform efforts. Austria will have to run its presidential election over due to voting irregularities.

There are two decisions next week, though they will not be made by politicians, they will have serious implications. The first decision will be made by the eurozone finance ministers. They will decide if Spain and/or Portugal should be sanctioned for the excessive deficits the EU judged.

The sanctions could include fines and the suspension of some regional funds. If the rules are not enforced, they lose credibility. If they are enforced, it appears discretionary and selective. Consider that despite repeated violations and expressions of concern; the German external imbalance has not been addressed. In European political theatre is might be best to sanction Spain and Portugal, and then suspend the judgement when the countries appeal under “exceptional circumstances” and make a “reasonable request.”

Japan

Abe’s Liberal Democrat Party and its coalition partner have expanded their majority in the upper house of the Diet. However, it did not appear to secure a super-majority (2/3) that ostensibly would have made it easier to change the Constitution, as Abe desires. Yet the situation is more complicated as the junior coalition partner is opposed to Abe’s stronger military thrust. The election is unlikely to have much market impact, and expect Abe’s immediate focus to be on solidifying plans for a large economic stimulus package.

China

The second important decision will come from a five-person panel at the Permanent Court of Arbitration at The Hague. At issue is a territorial dispute between the Philippines and China. It is the first case of its type. China has refused to participate. The Philippines want rulings on three aspects. First, what is the dispute over; islands, reefs, low tide elevations, etc.? An island (not man-made) comes with certain rights. Second, the Philippines wants the Court to specify what is rightfully the Philippines under the UN Convention on the Law of the Seas. Third, it wants the Court to determine if China has violated its rights. The ruling is expected July 12 near midday at the Hague.

Bank of Canada

In addition to the two political decisions, there are two major central banks that meet in the week ahead: the Bank of Canada and the Bank of England. The Bank of Canada faces an economy is struggling to sustain positive momentum. In 2015, Canada’s monthly GDP fell in six of the 12 months. The pattern is intact this year with two contracting months in the first four. May’s GDP will out toward the end of the month. Labor market improvement has stalled. Net exports appear to be a drag as record large trade deficits were recorded in the April-May period, and non-energy exports contracted in May.

Bank of England

Over the past two months, the implied yield on the December BA futures contract has fallen almost 25 bp (to 82.5 bp). The market has begun to price in the chances of a rate cut. However, investors would be surprised if the Bank of Canada were to deliver a rate cut now. The Canadian dollar, at least initially, would fall, especially as it would come as the market upgrades (on the margins) the risk of another December Fed hike. Rather than a rate move, expect a more pronounced dovish slant in the central bank’s forecasts and rhetoric.

On the other hand, the Bank of England is the more likely of the two to cut rates. BOE Governor Carney has already acknowledged that this may be necessary. The central bank has already canceled the anticipated increase in banks’ capital buffers. The market appears to have discounted a 25 bp base rate cut. The implied yield of the September short-sterling futures contract has fallen from nearly 60 bp before the referendum to 33 bp at the end of last week, having briefly touched a low point of 28 bp.

Some economists anticipate the Bank of England will bring the base rate down from 50 bp to 10-15 bp over time. While this is possible, we suspect that at 25 bp, officials would have gotten as much stimulus from lowering the base rate as possible. Should further stimulus be judged necessary, and we suspect it will, new asset purchases would seem to be a more promising measure than another cut in the price of money.

To be clear, if a 25 bp rate cut is not delivered at this week’s meeting, sterling would likely act positively, at least initially. It would be seen as a sign of caution. It would likely signal more emphasis on the new forecasts that are provided with the Quarterly Inflation Report next month. However, the Bank of England, apparently more than many others, took seriously the risk of Brexit, and what was once a risk forecast, now becomes the base case, more or less.

It still needs to calibrate its response, but perhaps the most surprising thing that has happened since the referendum is the resilience of the FTSE 250 (appreciating that the FTSE 100 stronger performance is a function of its heavy dependence on foreign earnings which are all the more valuable in a weak sterling environment). The FTSE 250 finished last week at roughly the midpoint of the referendum induced drop. Parts of the UK economy looked to be softening before the referendum, but economic readings outsides of consumer surveys, are not in real time. The freezing up of the several property funds is instructive. Although the problem looks contained, there are still risks of unforeseen contagions. Also, the interlocking ownership of some of the funds, pose concentration risks that regulators may want to investigate.

One of takeaways from the Great Financial Crisis experience is the most effective policy response comes early and forcefully. The Bank of England has every reasons to suspect that the Brexit decision will hit an economy that may have already been slowing. The political firestorm does not help matters. The BOE can act, or it can react. We suspect it will act. This does not preclude the BOE from doing more later. It can cut rates now and launch QE next month, with the Quarterly Inflation Report. We envision a modest purchase program (~GBP50 bln) that would be completed in a few months.

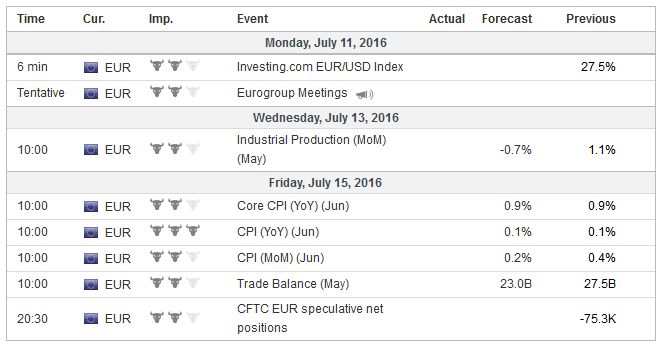

Eurozone DataThe eurozone economic data calendar looks interesting but it is not. Many countries have reported the national industrial output figures, so a significant month-over-month (~-0.8%) decline would not be surprising. It would be the third contraction in four months. The final CPI reading is likely to confirm the preliminary 0.1% year-over-year increase. The first above zero print since January, but is still nothing. The May trade balance also aggregates already released reports, and in any event, typically does not move the market. Two other issues dominate the discussions about the eurozone. The first is the Italian banking situation, where its third largest bank is the subject of much official and investor pressure. The debate is not whether the state can inject funds into its banks. It can. At stake is who must take losses first. Partly due to the idiosyncratic nature of Italy’s way (though ironically shared by Portugal) is that the bank bonds were widely treated by borrower and lender alike as a form of deposit in the bank. That is to say as much as half of the bank bonds in some institutions are owned not be institutional investors or foreign investors, but by retail savers, who are also known a taxpayers and voters. A resolution does not seem imminent, but the pendulum of market sentiment may have begun anticipating new capital as the FTSE Italian bank shares index jumped nearly 10% before the weekend. |

|

The second issue that has emerged and will continue to be debated ahead of the ECB meeting on 221 July is about the pending shorting of assets that qualify for purchase under its QE program. Presently the purchasing is being done according to the “capital key”, which is a function GDP and population.

This means that it buys more German bunds than bonds from any other country. At the same time, German is running a balanced budget and paying down debt. Also, given fears that Brexit could trigger a sequence of events lead to the fracturing of the monetary union, Germany bunds have an embedded call option (for the new German mark).

The ECB adopted two rules that increase the apparent shortage of Germany bunds. No security can be included in the purchase program whose yield is lower than the discount rate (-0.40%). There is also a cap on any issuer of 33%. Almost two-thirds of German bunds have yields below the deposit rate.

Recall too that the purchases were initially were to end in September, but have been extended to next March. We suspect that later this year, the ECB may extend it another six months. To sustain the buying the ECB can move away from the capital key, remove the deposit floor, lift the issuer limit. Many reports have focused on shifting from the capital key to the size of the debt market. Under such rule, Italy with its large stock of debt would be the single biggest beneficiary, while the amount of bunds that would purchased would be almost halved.

However, the capital key may be an important principle in decision-making as compromise between large and small countries. It seems that it may have too much gravitas to overrule as the first attempt. We suspect the story itself may not be what it seems. Tactically, such leaks often are aimed to hurt precisely that view or interest it appears to represent. It may be more helpful to think about those kind of leaks being plants rather than dogged reporting or careless officials.

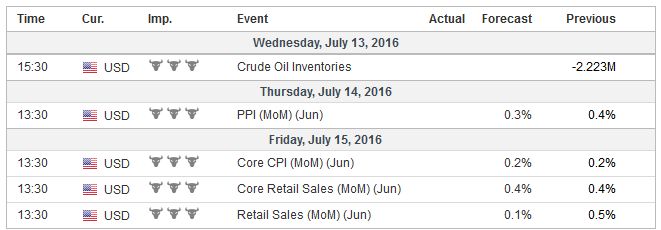

United StatesThe US data highlights typically include consumption and price readings after the employment report. However, the retail sales and CPI reports that will be reported at the end of next week may offer little than headline risk. The fact of the matter is that this month’s FOMC meeting will come and go with little fanfare. If the Fed is to move in September, which the market says is highly unlikely, it will not be because of June retail sales and consumer prices. Retail sales may be held back by the serial decline in auto sales (which are still at elevated levels), but the story of the Q2 is the recovery in consumption. Consumer prices likely remain firm. The core rate is expected to remain steady at 2.2%. It has been above 2% since last October. The headline rate is expected to tick up to the top of the narrow (0.9%-1.1%) range that has prevailed since February. We note that since the UK referendum, the Fed funds have traded firm around 40 bp. This is 3-4 bp rich compared with the rates that prevailed previously. The October Fed funds futures contract which is the best gauge in the futures market for the September meeting which is held late in the month (September 21) closed before the weekend at an implied 40 bp and the December Fed funds futures closed at 41 bp. The US Q2 corporate earnings season formally kicks-off in the coming week. It is expected to be the sixth consecutive quarterly decline in sales and the fifth straight decline in earnings. If there is good news to be found in the aggregate, it is that the pace of decline in slowing (e.g., S&P 500 earnings are projected to fall about 5.5% after a 6.6% decline in Q1; sales are expected to slip 0.9% after easing 1.5% in Q1). With the market at record highs, it appears liquidity rather than earnings has been the driver. |

|

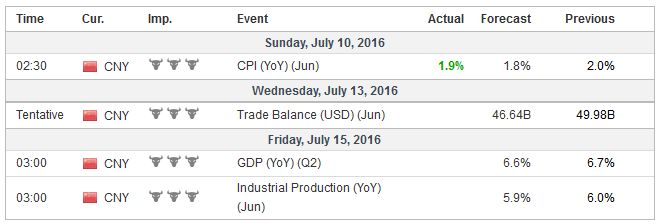

ChinaChina data cycle hits high gear in days ahead. The data is expected to show a continued gradual slowing of China’s economy, in which, nevertheless, the lending is accelerating with diminishing returns. The dollar has risen in ten of the last 12 sessions against the yuan. It has risen in eleven of the past 13 weeks. And it is falling faster against the basket the PBOC said it adopted at the end of last year. The operational policy remains of a “reasonably stable” exchange rate. Something must be lost in translation. However, we are not convinced Chinese officials are engineering the depreciation of the yuan.Market forces can explain the pressure on the yuan. Chinese officials appear to have simply reduced its resistance. In fact, it seems much more likely that if China were adopt a truly free-floating currency, which the yuan would fall further and faster than it has done. On a broad trade-weighted basis, the yuan appreciated nearly 30% from the middle of 2011 through the middle of last year. Over the past year, it recouped a little more than a third of its decline. Many have expressed concern about the deflationary spillover that the yuan’s depreciation will cause.We suggest the decline in bond yields is not being driven by Beijing but by Frankfurt, London, Brussels and Tokyo. The yuan’s depreciation against the yen is really more a function of the yen’s side of the equation. Also, remember the space China occupies in global supply chains. Valued-added costs incurred in yuan for exports still appears low by global standards. |

|

Our concern about a rapid or significant depreciation of the yuan is two-fold. First, its would aggravate the debt burden of companies that borrowed in dollars (or other foreign currencies). Second, it would make it more seductive for China to dump its surplus industrial capacity (steel, aluminum, glass, cement, etc., etc.) on foreign markets. Europe is expected to decide soon whether to recognize China as a market economy, which for WTO purposes, means it would be more difficult, but not impossible, to resist dump practices.

Full story here Are you the author?

Tags: Bank of Canada,Bank of England,China,Five Star Movement,Japanese yen,Matteo Renzi,newslettersent,Post-Brexit,Swiss government bonds