Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The US presidential selection process is well underway, and yet there has been no coherent discussion of fiscal policy. In part, this is because it does not appear particularly urgent.

The US presidential selection process is well underway, and yet there has been no coherent discussion of fiscal policy. In part, this is because it does not appear particularly urgent.The US deficit peaked in 2009 at 10.1% of GDP. Last year it stood at what for most OECD countries an enviable 2.6%. This year and next it is forecast by private sector economists to reach 2.9%.

There are many who arguethat monetary policy has been as accommodative as possible. With the expansion entering its seventh year, unemployment at 5%, and the Fed’s preferred inflation measure (the core PCE deflator) at 1.7%, interest rates remain low in both nominal and real terms.

The Fed funds target is 25-50 bp. While most economists expected to it be lifted in June, investors seem less sanguine. The Fed funds futures strip is consistent with one rate hike late this year. Treasury yields through the seven-year note are below the core PCE deflator. The real 10-year yield is only a few basis points in positive territory.

Growth in Q4 15 was poor at a revised annual rate of 1.4%. Although we, like many, had anticipated a rebound in Q1 16, this does not seem to be the case. The Atlanta Fed GDPNow tracker projects growth at 0.3% in the first three months of the year, while the newer New York Fed GDP tracker anticipates, with a different methodology a 0.8% annualized pace.

Some economists like Summers and Krugman have been advocated greater public investment. Both Bernanke and Yellen appear sympathetic to such proposals. While recognizing the high level of government debt, they also have argued in favor of new government investment, particularly with such low prevailing interest rates.

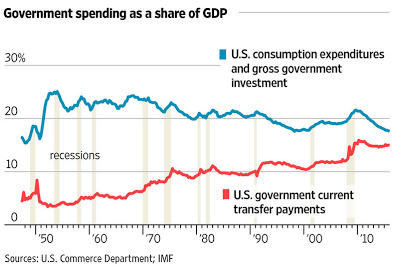

Indeed, government (local, state and federal combined) spending on goods and services and investment fell to the lowest in a generation (1949) in Q4 last year of 17.6% of GDP. Government expenditures have not fallen, so what is happening?

As this chart from the Wall Street Journal

|

|

In fact, making a few conservative assumptions, and barring new initiatives, the two lines in the chart are likely to cross during the President’s term. This points to a changing relationship between the government and citizens.

Some argue that these transfer payments are crowding out government spending and investment. This is only true if one accepts certain ideological claims. To crowd out suggests that government expenditures are fixed. They can be spent either on transfer payments or consumption and investment. There is no iron law that says that government expenditures are fixed. The governments of many, if not most high income countries, have greater expenditures as a percentage of GDP than the US.

Although it has tried higher tax schedules and lower tax schedules, the Federal government seems unable to increase revenue to more than 20% of GDP. That means expenditures in excess of 20% of GDP are financed by debt issuance. US government debt in public hands is about 75% of GDP. If one includes the government debt owned by different parts of the government, the debt ratio increases to 105% of GDP.

What ultimately is important is not the level of debt but the ability to service it. Last year the cost of servicing the Federal debt was 6% of GDP or $223 bln. However, there is a critical offsetting factor. The Federal Reserve is the single largest holder of US Treasury bonds. As is its practice, it turns over money back to the Treasury every year, even before QE, more than what it needs for its operations. Last year, it was nearly $100 bln. This reduced the “real” debt servicing costs to almost 3% of GDP.

Roughly $220 bln of the Fed’s Treasury holdings will mature this year. The Federal Reserve has indicated that it will only allow its balance sheet to shrink through the maturation of its holdings after its normalization process is well underway. Previously we had thought that this could mean that later this year, it could allow some passive reduction of its balance sheet by not replacing maturing instruments.

However, as a consequence of the more gradual normalization process, i.e., rate hikes, this does not seem likely this year. One implication of this is that the Federal Reserve is likely to transfer another $100 bln or so back to the US Treasury this year.

The main obstacle to a new New Deal in the US is not stem from economics. There is nothing in the literature that says a 4.0% deficit horrific, but a 3% deficit is sustainable. Just like low interest rates offer a low the hurdle rate for private investment, it does the same for public investment. The proposal to increase public investment is not to have one group of people dig ditches and another group to fill it. Surely the US infrastructure is in desperate need to modernizing. One of the big economic challenges is the low productivity. Economic studies have shown that improved infrastructure boosts productivity.

Private investment in the US is weak. Some attribute it to tax, regulatory, and political uncertainty, but it need not be purely in the realm of psychology. Consider that in March, the capacity utilization rate was at 74.8%, a six-year low. Low utilization rates by themselves, leaving aside the fuzziness of uncertainty, deters investment in plant and equipment. The weak private investment also means that a public investment program would not be crowding in out.

If the chief obstacle is to a public works program is not economic, what is it? It is ideological beliefs that hold government efforts in low regard. It is a loss of social trust, and arguably civic responsibility. It the ideological belief that government is the problem, not the solution. It is arguments that the government’s debt is already too high.

Will we or our children look back at this time with low real and nominal interest rates, and see a missed opportunity to strengthen the US infrastructure, modernize cities, roads, bridges, electric grids, and set the stage for tomorrow, with investment in renewable energy? Will not doing something now be more costly than doing a new public investment program?

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: Fiscal,newslettersent