Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

There are two broad themes among the major currencies today. The first is the pullback in the euro and yen after yesterday's run-up. Position adjustments with the help of stop losses seemed to be the key consideration. Both the euro and yen extended the recovery seen in the second half of last week. Year-end considerations, both in terms of positioning and less liquidity, likely played a role as well.

The second broad theme is the relative strength of the Australian and New Zealand dollars. The RBNZ got the ball rolling with a hawkish rate cut. By that, we mean that although the RBNZ cut rates, its guidance reinforced the view that the 25 bp cut in the cash rate to 2.50% may be the last cut in the cycle. The central bank indicated that at current rates, the inflation target can be reached. To be sure the RBNZ called for further depreciation of the New Zealand dollar. We suspect that, although the RBNZ is on hold for next few months, strength in the currency or continued weakness in commodities will likely put it back into play later in Q1 or early Q2.

The New Zealand dollar staged a sharp rally on the news, and then extended the rally in Asia a little past $0.6780. The failures to rise through the $0.6800 area spurred some liquidation that pushed the Kiwi back to $0.6720. Support is seen in the $0.6680-$0.6700 area.

The Australian dollar was initially dragged higher by the Kiwi' surge but then got its own impetus in the form of a jobs report that seems too good to be true. The consensus had expected a 10k loss in jobs after a 58.6k increase in October. Instead, 71.4k jobs were reported though the October increase was pared to 56.1. The unemployment rate ticked down to 5.8%, even though the participation rate rose to 65.3% from 65.0%. Also, the breakdown showed a gain of 41.6k full-time positions after a revised 38.4k ( initially 40k) increase in October. Year-to-date, Australia has reported 301.7k new jobs, the best since 2006.

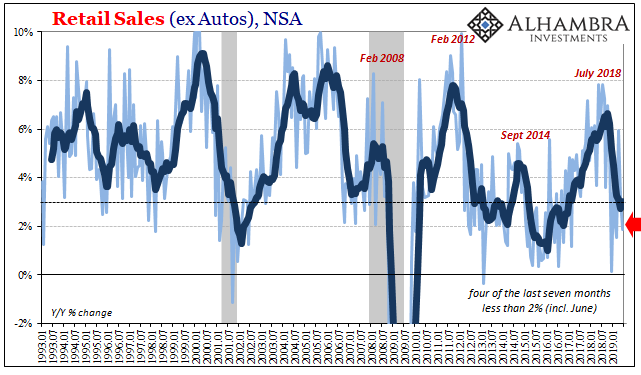

While there does seem to be some improvement, many suspect that methodological issues relating to the rotating sample may be distorting the data. Although time series that economists look to for confirmation, like income tax receipts, are not matching the improvement. However, retail and auto sales figures are robust, and home construction is at record highs.

The Aussie ran out of steam near $0.7335. Initial support is seen in the $0.7250-$0.7280 area. Many suspect the RBA's monetary easing cycle is over though appreciation of the Aussie and weak commodity prices could see speculation of lower rates materialize in a couple of months.

The Swiss National Bank met, and as widely anticipated, left its 3-month LIBOR target unchanged at -75 bp. It too expressed concern about the overvaluation of its currency and indicated that negative rates and continued intervention will help. It did not change the inflation forecast for next year, which stands at -0.6%. This year's estimate was tweaked to -1.1% from -1.2%. The Swiss franc is moving largely in line with the euro today as yesterday's gains are unwound. The franc has strengthened slightly on the cross.

The Bank of England meets and will publish the minutes immediately. McCafferty has been the lone dissenter calling for a hike. There is some thought that he could abandon this position not be the first time that McCafferty ran ahead of the pack only to rejoin the fold. His hawkish dissent did not prevent the market from recognizing the more dovish signals from the BOE. So if the dissent is abandoned, we would not expect it to have much impact.

Last week, the June 16 short-sterling futures contract tested the contract high set on October 2 at 99.34 (implying a 66 bp interest rate on a three-month deposit in six months time), which is evidence of the recognition that McCafferty was off-message. However, rates have firmed a bit, and the implied yield had risen to 72 bp currently. Sterling itself has staged a rebound from the dip to about $1.4960 on Tuesday to almost $1.5200 today. Intra-day technicals warn of risk of a break of $1.5150.

Sterling's strength is more evident against the euro than the dollar. The euro rallied from about GBP0.7000 at the start of the month to almost GBP0.7280 on Tuesday this week. It is now testing the GBP0.7200 area. A break could spur a move toward GBP0.7160 initially.

The euro peaked near $1.1040 in the North American session yesterday, extended last week’s advance. A loss of momentum in Asia brought in selling in Europe. Potential exists to $1.0890-$1.0920 today. We had anticipated the $1.08-$1.10 to confined prices ahead of US retail sales due tomorrow. At the start of the week, the $1.08 level was briefly frayed but appeared to bring in some bottom-pickers. Similarly, the move above $1.10 also seemed premature. It appears headed back to the middle of the range though a light news stream in North America may deny it sufficient momentum to reach $1.09.

Lastly, we note the conflicting signals from Sweden and Norway. Sweden’s November CPI disappoint by falling 0.2% on the month for a 0.1% year-over-year pace. Underlying inflation, which uses fixed mortgage interest rates slipped to 1.0% from 1.1%. Although the Riksbank is not expected to ease rates further or expand is asset purchases next week, deflationary forces indicate that the central bank’s work may not be done.

Norway, on the other hand. reported stronger than expected inflation pressures. Headline CPI rose 0.4% in November, lifting the year-over-year rate to 2.8%, which is the highest level in more than two years. The underlying rate is adjusted for tax changes and excludes energy, rose 3.1% year-over-year. Norges Bank meets next week and is expected to stand pat. Sweden’s central bank is concerned about (the lack of) price pressures, while Norway is more concerned about weak growth.

The stronger inflation report sparked more than a one percent drop in the euro against the krone. However, the move needs to be placed in the context of the sharp euro gains over the past week. The NOK9.41 area corresponds to a 38.2% retracement of those gains, and NOK9.35 is about the 50% objective. The euro remains firm against the Swedish krona at the upper end of this week’s range.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Participation Rate,U.S. Retail Sales