Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

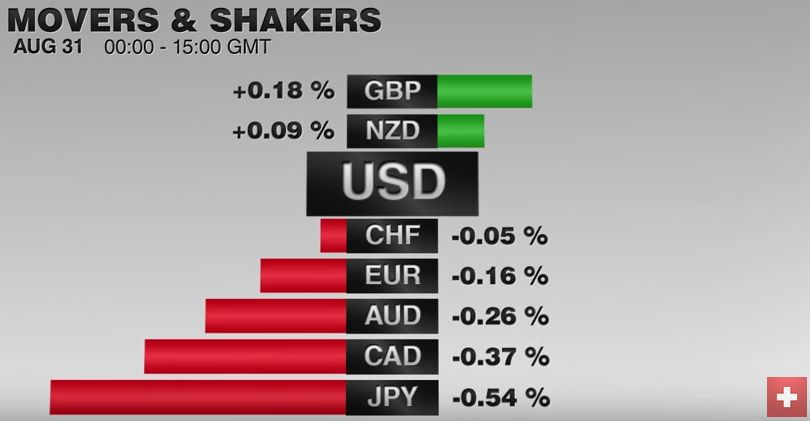

The US dollar is firm against the dollar-bloc currencies, and sterling, but is heavier against the euro and yen.

The 13th consecutive year-over-year decline in China's imports helped keep the pressure on the commodity producers. Despite New Zealand reporting strong Q3 manufacturing sales (3.5% vs. -0.2% in Q2), the pendulum of market expectations have continued to swing for a rate cut later this week.

The drop in oil prices, and secondarily the widening of the interest rate gap with the US, sent the Canadian dollar to new multi-year lows yesterday. Although the price of oil has stabilized today, the technical damage has been done, and the Canadian dollar has extended yesterday's losses. It is difficult to see any significant technical hurdle until close to CAD1.40. However, near-term the CAD1.3600-CAD1.3630 appears to be the next target. Support for the US dollar is seen just below CAD1.3500.

The euro is within yesterday's ranges. Given Thursday's dramatic moves, we argue that 1) the leg lower than began in mid-October is complete and 2) with the rally to almost $1.10, many of the short-term positions have been cleared. This sets up for a better two-way market. As we saw yesterday, there are those who are inclined to buy euro dips, on the ideas that downside is limited and that, at the very least, the correction is not over. At the same time, there are those focusing on the divergence theme and interest rate differentials, are sellers of euro bounces.

EMU confirmed Q3 GDP at 0.3% for a 1.6% year-over-year pace. What was important about today's release though was the details available. Contrary to conventional wisdom, the weak euro is not spurring an export-led expansion. It is still primarily an internal affair. Household consumption rose 0.4%. A little less than expected, but a touch better than the revised 0.3% increase in Q2. Government expenditures, rose 0.6%, twice the pace the market expected and what was seen in Q2. Gross fixed investment was disappointingly flat (consensus 0.2%), but the Q2 figure was revised to 0.1% from -0.5%.

Sterling has been offered since the unexpected decline in Halifax house price index. The 0.2% slippage in prices compares with expectations of an increase of the same magnitude. While this report tends not to be a market mover, a combination of the surprise and the general bearish tone encouraged selling. With today's losses to almost $1.4990, sterling has retraced 61.8% of the bounce since in the second half of last week. A move above $1.5020 would help stabilize the tone though the $1.5040-$1.5060 area may be a more important hurdle.

The industrial production report was mixed. It eked out the 0.1% gain the market expected in October, and the September decline (-0.2%) was revised away. However, the disappointment was with manufacturing output. It fell 0.4% or twice the expected decline. It was only partly mitigated by the upward revision to the September series (0.9% from 0.8%). Given the volatility, using moving averages help identify the underlying trend. The three-month average of UK manufacturing output is 0.3%. This is the highest since August 2014.

As anticipated, Japan's Q3 GDP was revised higher to 0.3% from the initial 0.2% contraction reported. We do not accept that there is a technical or official definition of recession. Yes, the two consecutive quarters of contraction is a rule of thumb, but even the US does not use that definition. Recession denotes the end of a business cycle.

We do not think that Japan's business cycle has ended and recent data points to accelerated growth here in Q4. And more importantly, than any one economist view is the understanding of Japanese officials due to the reaction function. Japanese officials seem to share generally our understanding of the state of their economy.

Separately Japan reported a seasonally adjusted October current account surplus twice the size of the September surplus, though not as large as the market expected. Some calls for a stronger yen next year are predicated on a larger external surplus. However, the yen's strength today seems to be more a function of the slide in equities and that Us 10-year yields are ten bp below last week's high.

China reported a November trade surplus of $54.1 bln, nearly $10 bln smaller than the consensus expected. It is the smallest surplus in four months. To the extent that the expected trade surplus fed into an analysis of the decline in reserves reported yesterday, it would suggest somewhat less capital outflows. Exports fell more than expected at 6.8%, a little better than the 6.9% decline in October. Imports improved more than expected. The 8.7% decline year-over-year compares with a consensus forecast for nearly a 12% contraction and an 18.8% contraction in October. The CPI figures tomorrow are seen as more important for influencing the PBOC’s monetary stance.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.K. House Price Index