Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Consolidation Featured Ahead of Tomorrow’s US Retail Sales and Friday’s Japanese Wage News

Consolidation Featured Ahead of Tomorrow’s US Retail Sales and Friday’s Japanese Wage News13 Mar 2024

China’s CSI 300 Rises for Seventh Consecutive Session and Offshore Yuan Strengthens for the Sixth Session

China’s CSI 300 Rises for Seventh Consecutive Session and Offshore Yuan Strengthens for the Sixth Session21 Feb 2024

Dollar Jumps, while Surge in Covid Cases Raise Questions about China’s Pivot

Dollar Jumps, while Surge in Covid Cases Raise Questions about China’s Pivot21 Nov 2022

May Payrolls (and more) Confirm Slowdown (and more)

May Payrolls (and more) Confirm Slowdown (and more)7 Jun 2022

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed13 May 2022

For The Fed, None Of These Details Will Matter

For The Fed, None Of These Details Will Matter6 Mar 2022

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?5 Jan 2022

Very Rough Shape, And That’s With The Payroll Data We Have Now

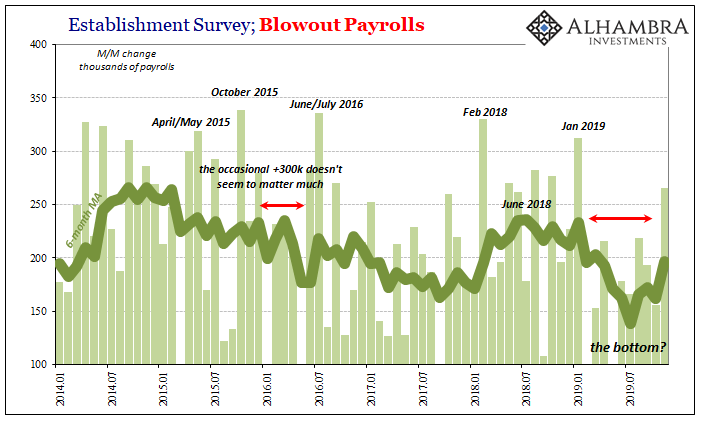

Very Rough Shape, And That’s With The Payroll Data We Have Now15 Jan 2020

Disposable (Employment) Figures

Disposable (Employment) Figures11 Dec 2019

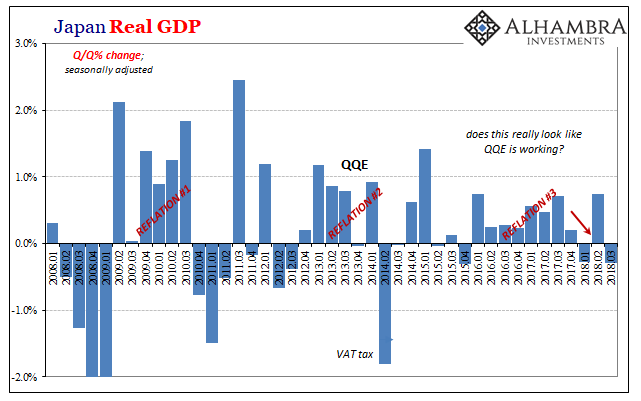

Japan: Fall Like Germany, Or Give Hope To The Rest of the World?

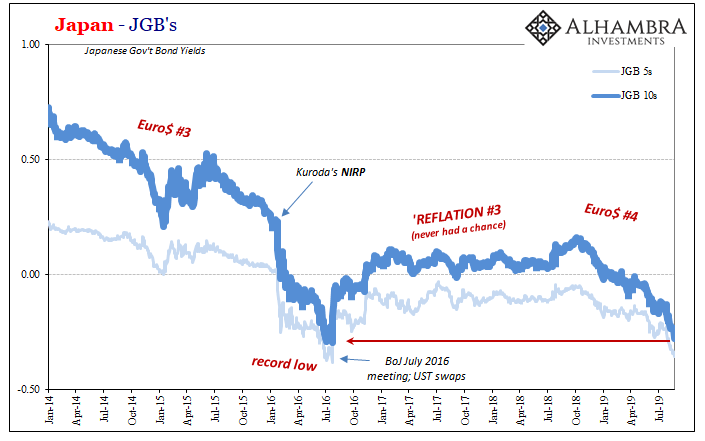

Japan: Fall Like Germany, Or Give Hope To The Rest of the World?29 Aug 2019

No Surprise, Hysteria Wasn’t a Sound Basis For Interpretation

No Surprise, Hysteria Wasn’t a Sound Basis For Interpretation28 Feb 2019

Inflation Falls Again, Dot-com-like

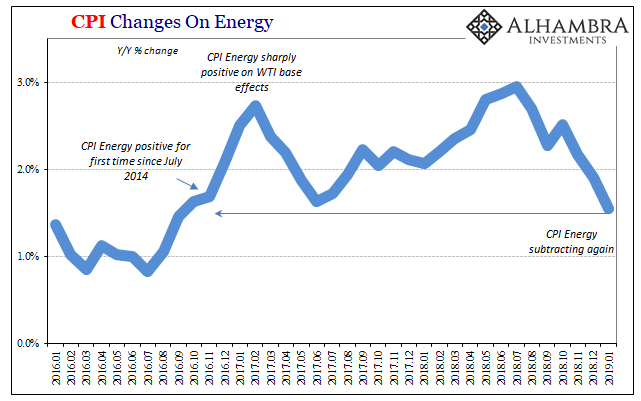

Inflation Falls Again, Dot-com-like16 Feb 2019

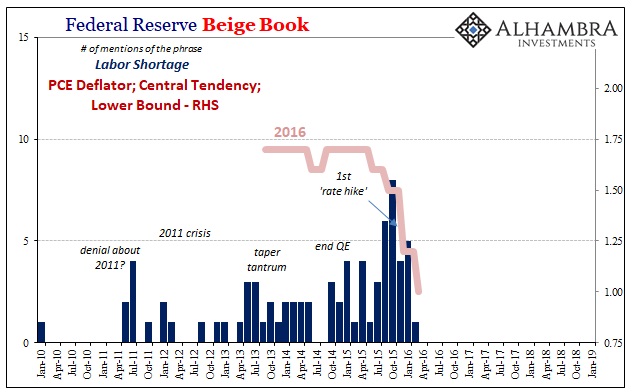

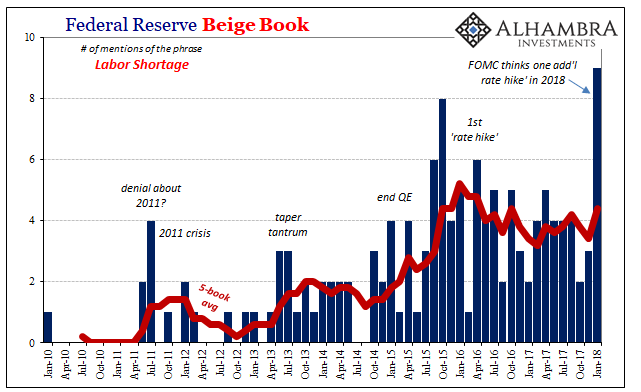

Hall of Mirrors, Where’d The Labor Shortage Go?

Hall of Mirrors, Where’d The Labor Shortage Go?20 Jan 2019

Economics Is Easy When You Don’t Have To Try

Economics Is Easy When You Don’t Have To Try11 Dec 2018

Another ‘Highest In Ten Years’

Another ‘Highest In Ten Years’1 Nov 2018

No Such Thing As An 80 percent Boom

No Such Thing As An 80 percent Boom26 Oct 2018

Buybacks Get All The Macro Hate, But What About Dividends?

Buybacks Get All The Macro Hate, But What About Dividends?13 Jul 2018

The Retail Sales Shortage

The Retail Sales Shortage22 Apr 2018

U.S. Unemployment: The Dissonance Book

U.S. Unemployment: The Dissonance Book20 Jan 2018

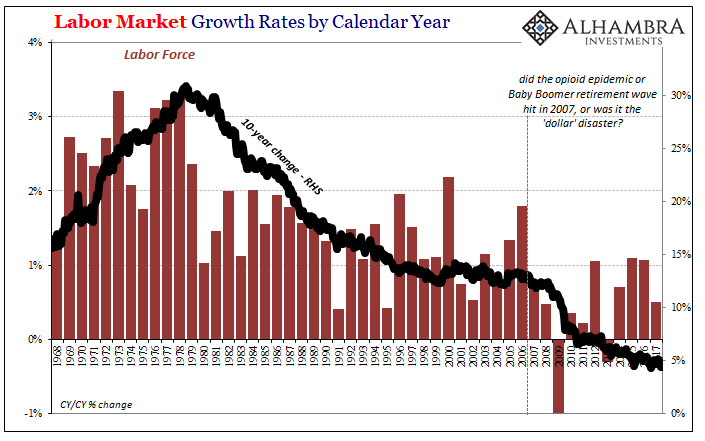

The Reluctant Labor Force Is Reluctant For A Reason (and it’s not booming growth)

The Reluctant Labor Force Is Reluctant For A Reason (and it’s not booming growth)10 Jan 2018