Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

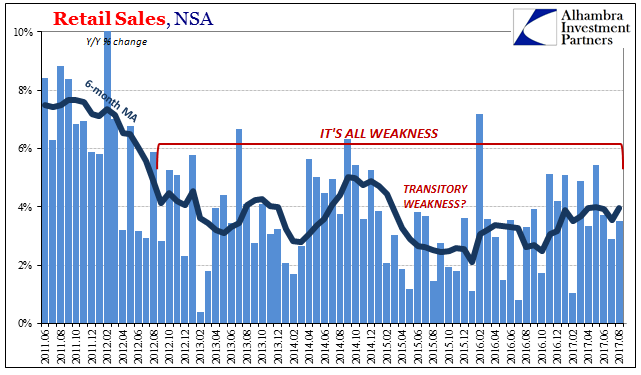

Retail Sales, Consumer Sentiment, And The Aftermath Of Hurricanes

Retail Sales, Consumer Sentiment, And The Aftermath Of Hurricanes17 Jan 2018

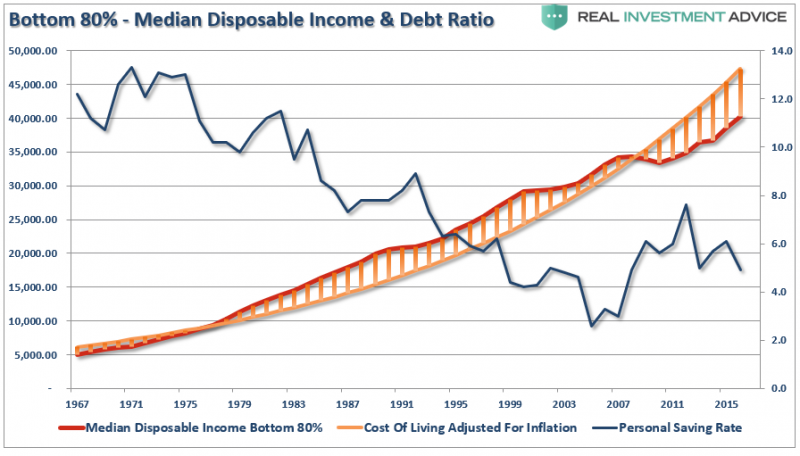

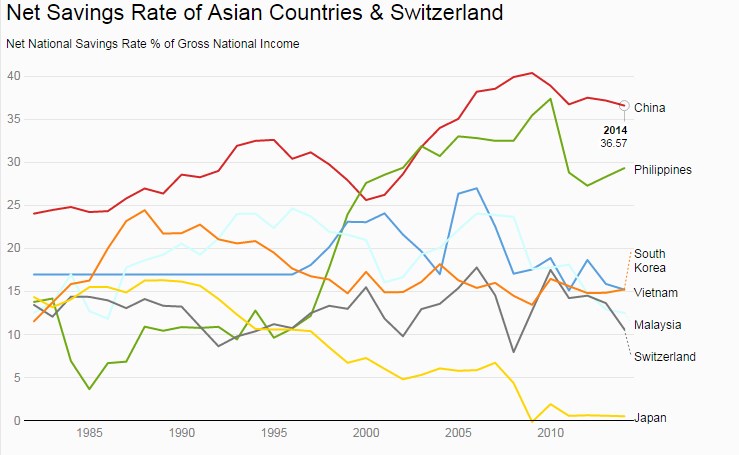

The Savings Rate Conundrum

The Savings Rate Conundrum8 Nov 2017

The (Economic) Difference Between Stocks and Bonds4 Nov 2017

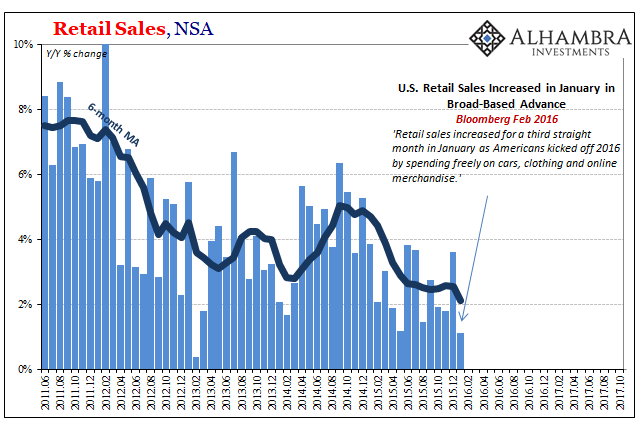

US Retail Sales: Retail Storms17 Oct 2017

The Damage Started Months Before Harvey And Irma11 Oct 2017

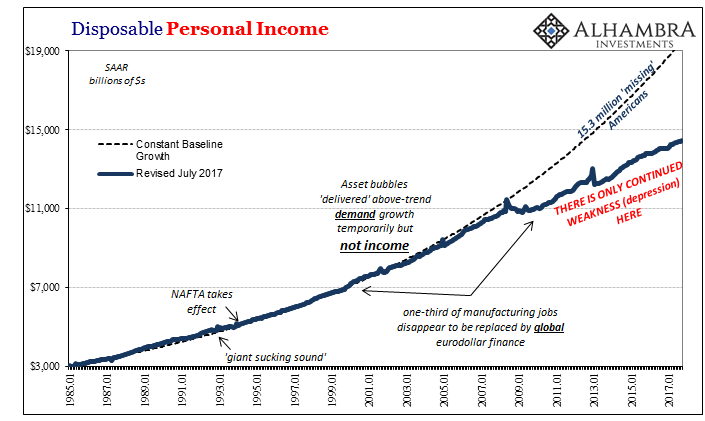

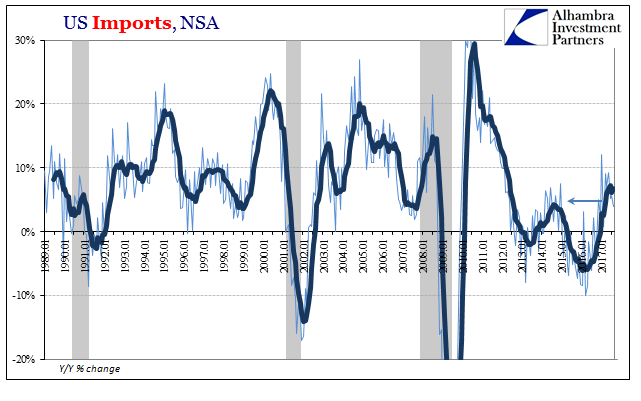

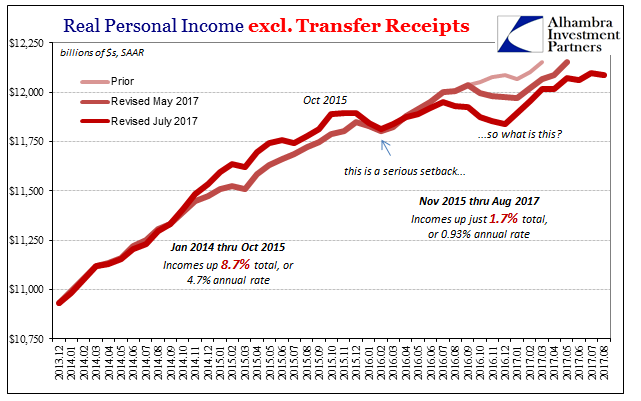

Incomes Are What Matters, So Bad Month, Bad Year, Bad Decade8 Oct 2017

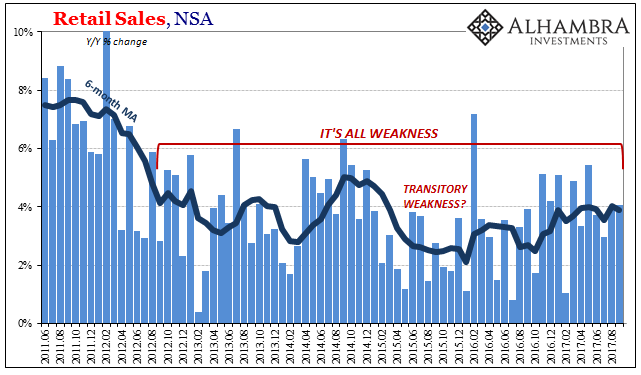

Retail Sales and the End of ‘Reflation’22 Sep 2017

FX Daily, August 02: Greenback Slides Despite RBA Rate Cut and 7-year Low in UK Construction PMI

FX Daily, August 02: Greenback Slides Despite RBA Rate Cut and 7-year Low in UK Construction PMI3 Aug 2016

Stockman Rages: Ben Bernanke Is “The Most Dangerous Man Walking This Planet”

Stockman Rages: Ben Bernanke Is “The Most Dangerous Man Walking This Planet”12 Jul 2016

Will the Dollar Appreciate on higher U.S. Savings and a Smaller Trade Deficit?12 Jul 2014