Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

How to Build and Destroy a Pension Fund System in 22 Easy Steps

How to Build and Destroy a Pension Fund System in 22 Easy Steps26 Oct 2022

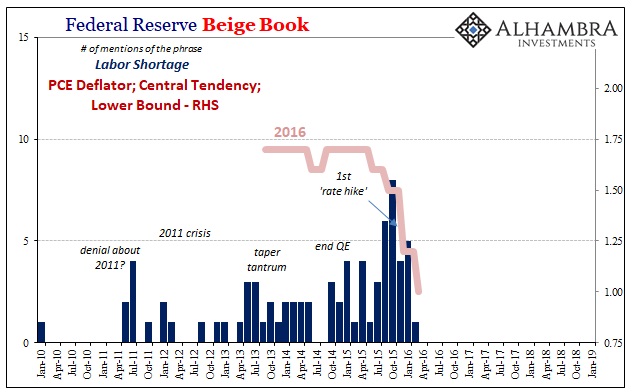

Nasty Number Five, Not Hawk Hiking CBs

Nasty Number Five, Not Hawk Hiking CBs27 Jun 2022

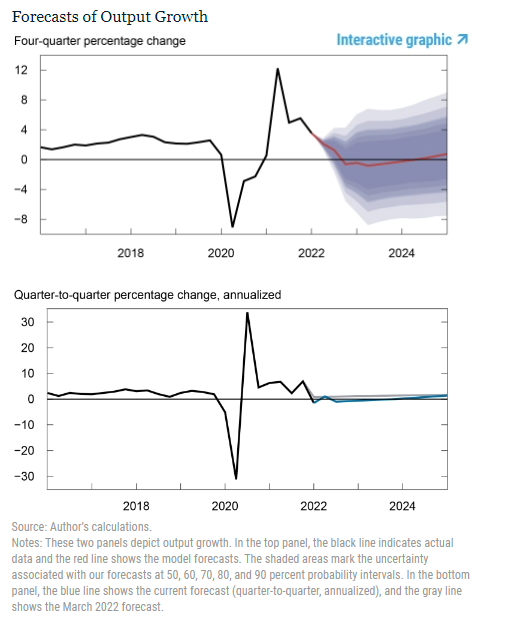

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk

Sorry Chairman Powell, Even FRBNY Now Has To Forecast Serious and Seriously Rising Recession Risk20 Jun 2022

Prices As Curative Punishment

Prices As Curative Punishment14 Jun 2022

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown2 Jun 2022

Peak Policy Error

Peak Policy Error1 Jun 2022

‘Unconscionably Excessive’ Denial

‘Unconscionably Excessive’ Denial30 May 2022

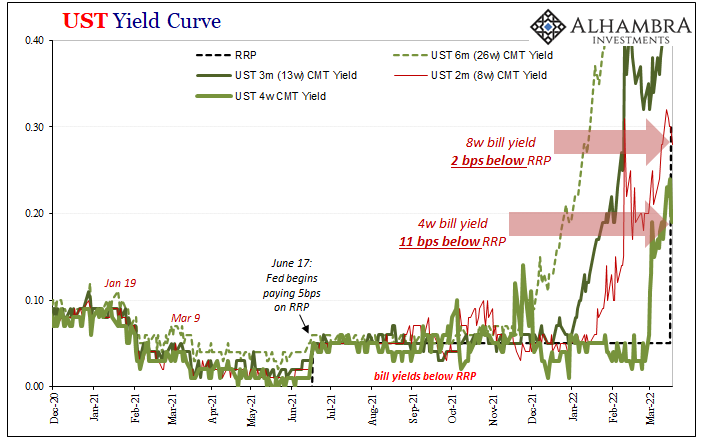

RRP (use) Hits $2T, SOFR Like T-bills Below RRP (rate), What Is (really) Going On?

RRP (use) Hits $2T, SOFR Like T-bills Below RRP (rate), What Is (really) Going On?27 May 2022

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Peak Inflation (not what you think)

Peak Inflation (not what you think)15 May 2022

Who’s Playing Puppetmaster, And Who Is Master of Puppets

Who’s Playing Puppetmaster, And Who Is Master of Puppets9 May 2022

China Then Europe Then…

China Then Europe Then…8 May 2022

Collateral Shortage…From *A* Fed Perspective

Collateral Shortage…From *A* Fed Perspective7 May 2022

Some ‘Core’ ‘Inflation’ Difference(s)

Some ‘Core’ ‘Inflation’ Difference(s)6 May 2022

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’21 Apr 2022

You Know What They Say About The Light At The End Of The Tunnel

You Know What They Say About The Light At The End Of The Tunnel14 Apr 2022

Concocting Inventory

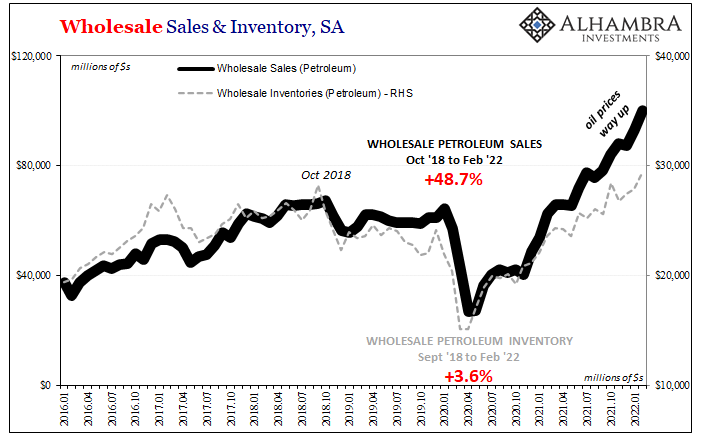

Concocting Inventory11 Apr 2022

Goldilocks And The Three Central Banks

Goldilocks And The Three Central Banks7 Apr 2022

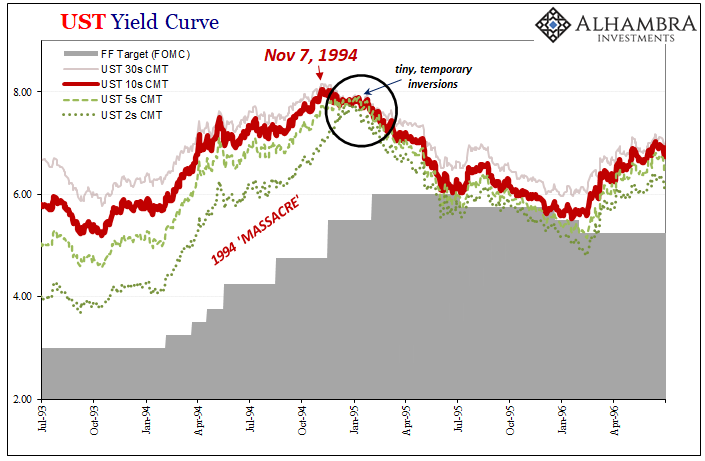

We Can Only Hope For Another (bond) Massacre

We Can Only Hope For Another (bond) Massacre30 Mar 2022