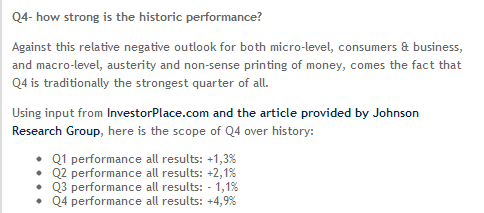

Read More »

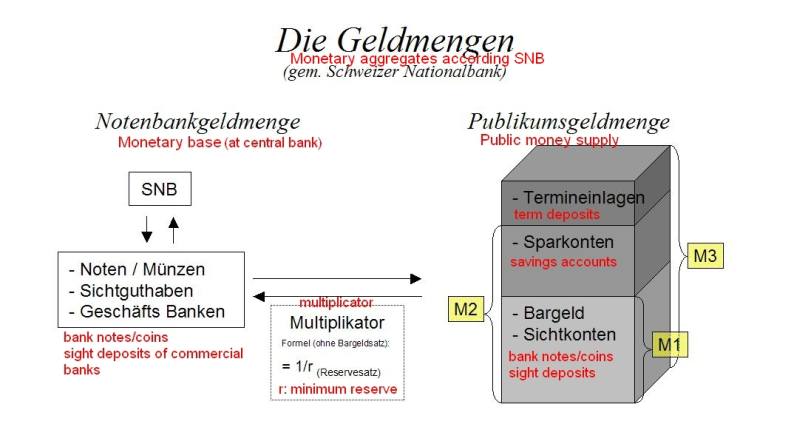

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

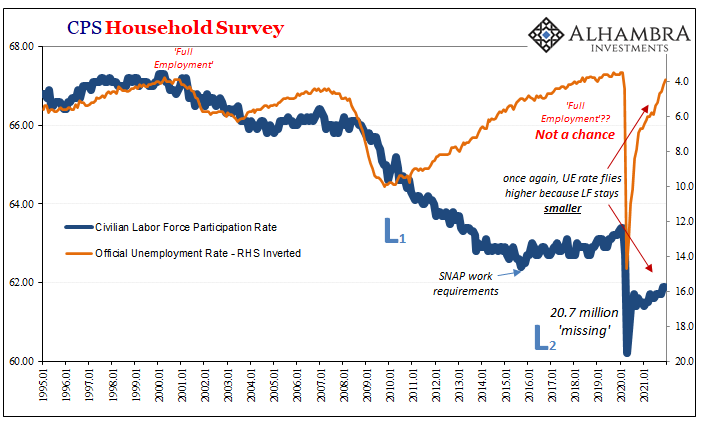

Taper Discretion Means Not Loving Payrolls Anymore

Taper Discretion Means Not Loving Payrolls Anymore10 Jan 2022

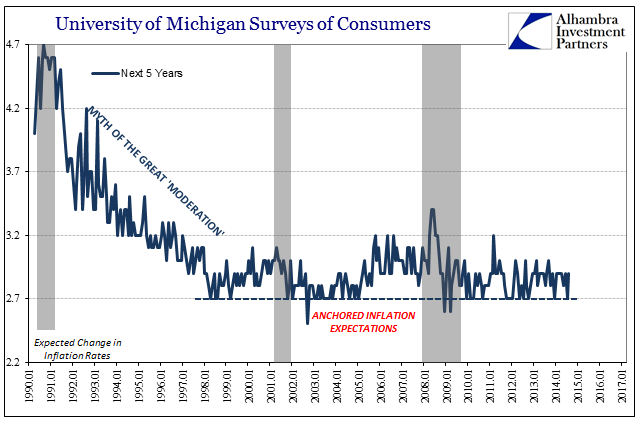

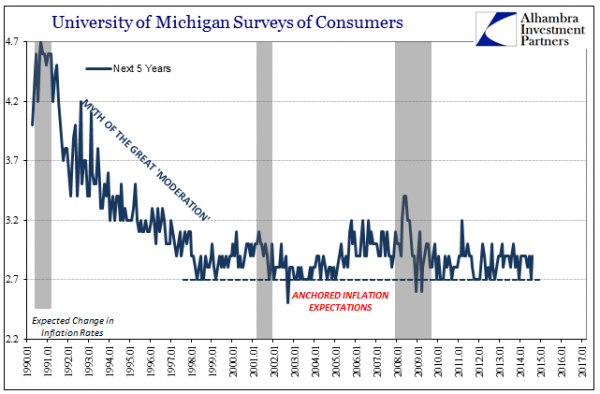

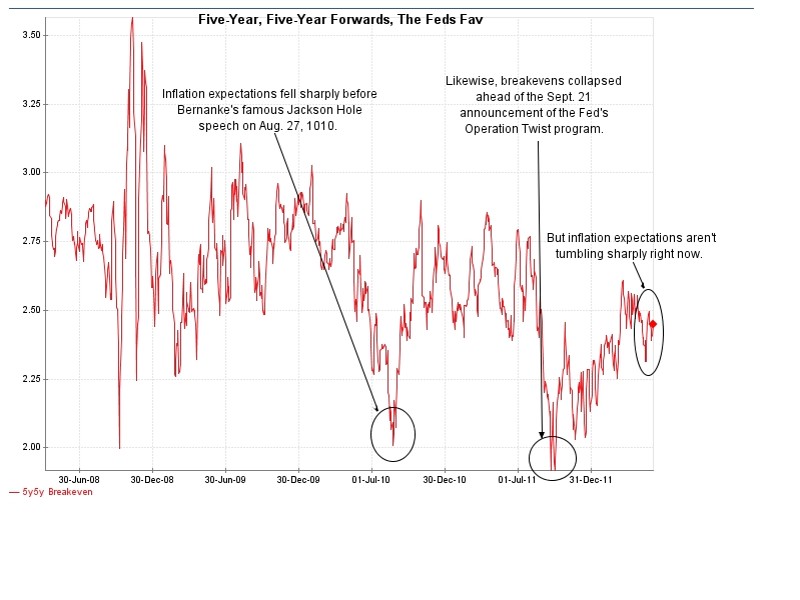

Further Unanchoring Is Not Strictly About Inflation

Further Unanchoring Is Not Strictly About Inflation18 Mar 2017

Global Risk Off: China Reenters Bear Market, Oil Tumbles Under $30; Global Stocks, US Futures Gutted15 Jan 2016

SNB Sight Deposits Fall by 1.2 Billion CHF, Weeks ending February 1 and 811 Feb 2013

SNB Sight Deposits Rise by 100 Million CHF, Week January2828 Jan 2013

SNB Sight Deposits Rise by 2 Bln. Francs, M3 by 10 Bln., Week January 2121 Jan 2013

SNB Monetary Data Week October 2629 Oct 2012

SNB Monetary Data Week October 1922 Oct 2012

SNB Monetary Data Week October 1215 Oct 2012

IMF Data: SNB Forex Reserves and Gold in September 201212 Oct 2012

SNB Monetary Data Week October 58 Oct 2012

The win of the pro-bailout parties in the Greek elections was no win for the SNB25 Jun 2012

Quantitative Easing Indicators, June 2012

Quantitative Easing Indicators, June 201210 Jun 2012

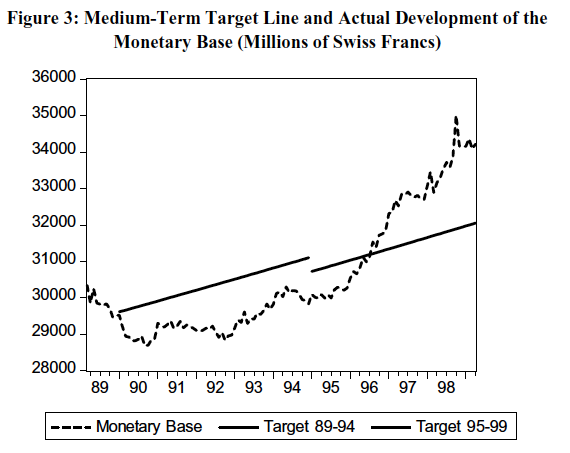

Swiss Inflation, GDP, Monetary Base between 1974 and 2000

Swiss Inflation, GDP, Monetary Base between 1974 and 200011 Aug 2003