Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

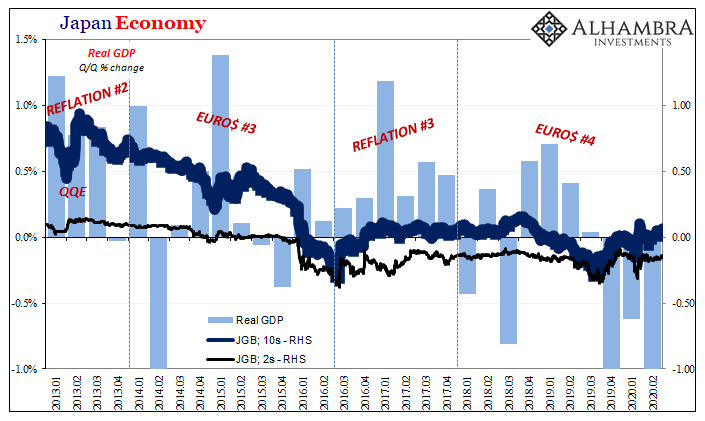

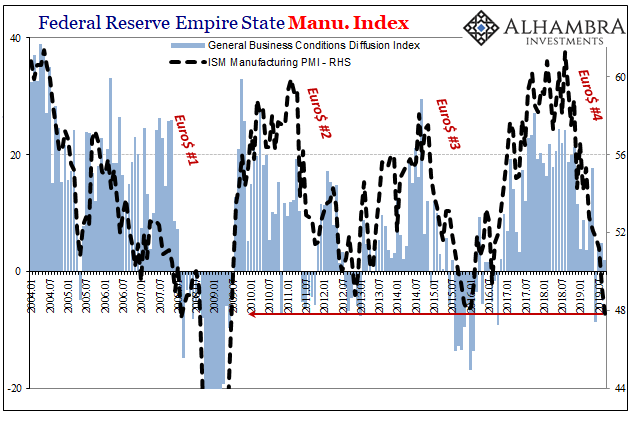

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

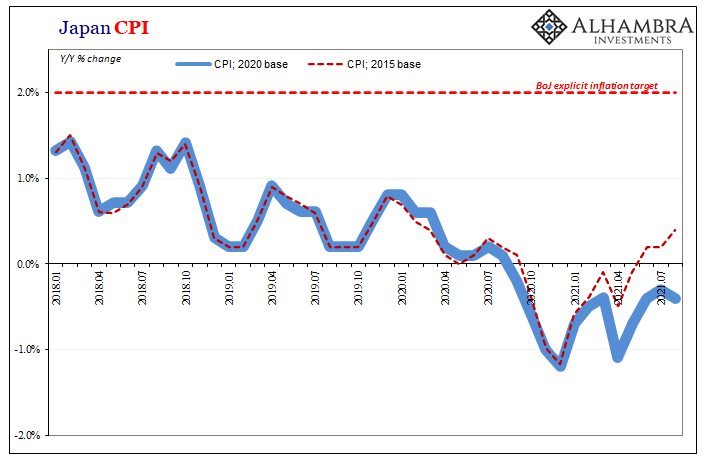

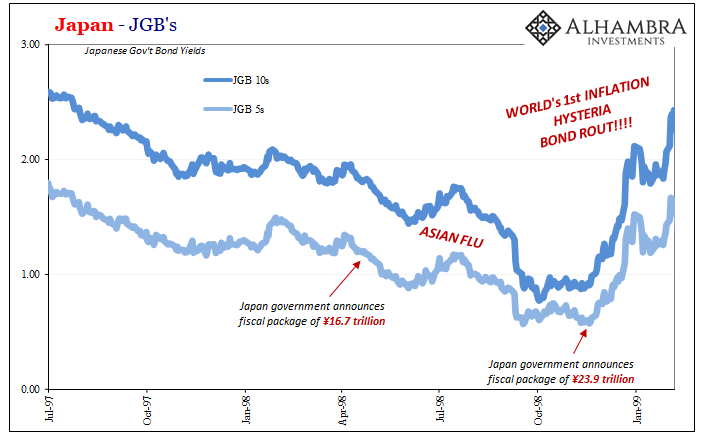

August Avoids Zero In JGB’s28 Sep 2021

Inching Closer To Another Warning, This One From Japan20 Jul 2021

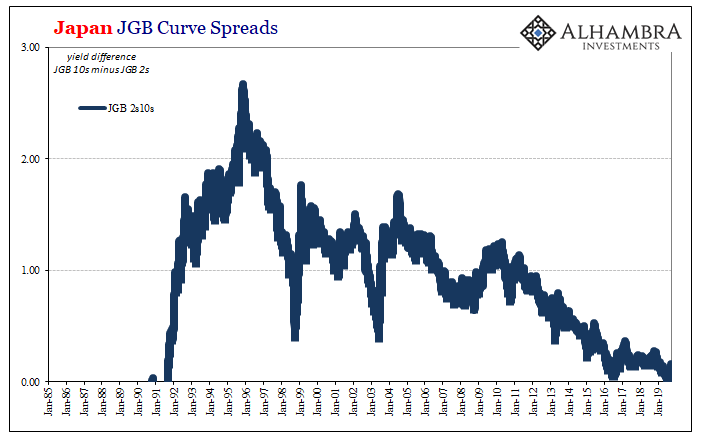

Bond Reversal In Japan, But Pay Attention To It In Germany9 Jul 2021

They’ve Gone Too Far (or have they?)10 Jan 2021

Re-recession Not Required12 Sep 2020

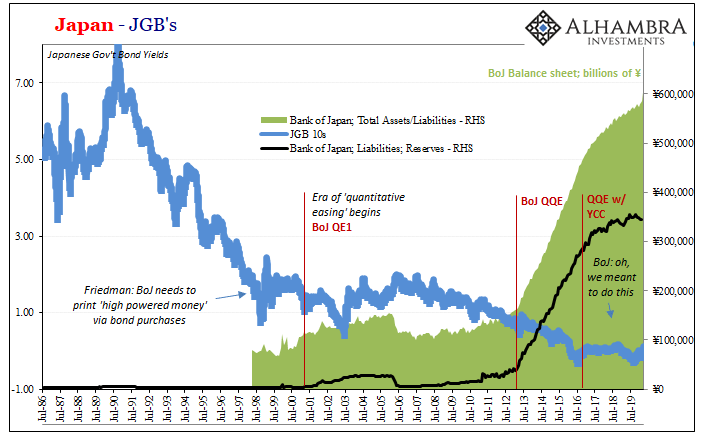

From QE to Eternity: The Backdoor Yield Caps4 Jun 2020

There Was Never A Need To Translate ‘Weimar’ Into Japanese

There Was Never A Need To Translate ‘Weimar’ Into Japanese17 May 2020

Why The Japanese Are Suddenly Messing With YCC6 Oct 2019

ISM Spoils The Bond Rout!!!3 Oct 2019

Japan: Fall Like Germany, Or Give Hope To The Rest of the World?29 Aug 2019

Lost In Translation8 Feb 2019

The Global Burden12 Apr 2017

Systemic Depression Is A Clear Choice5 Apr 2017

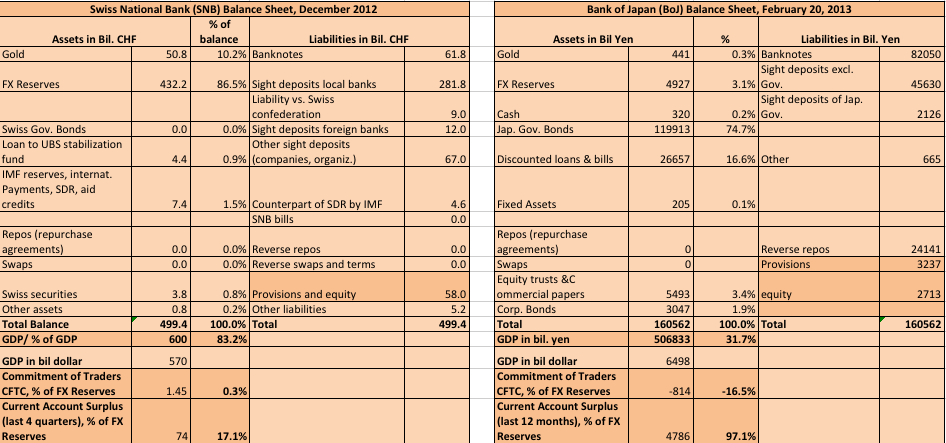

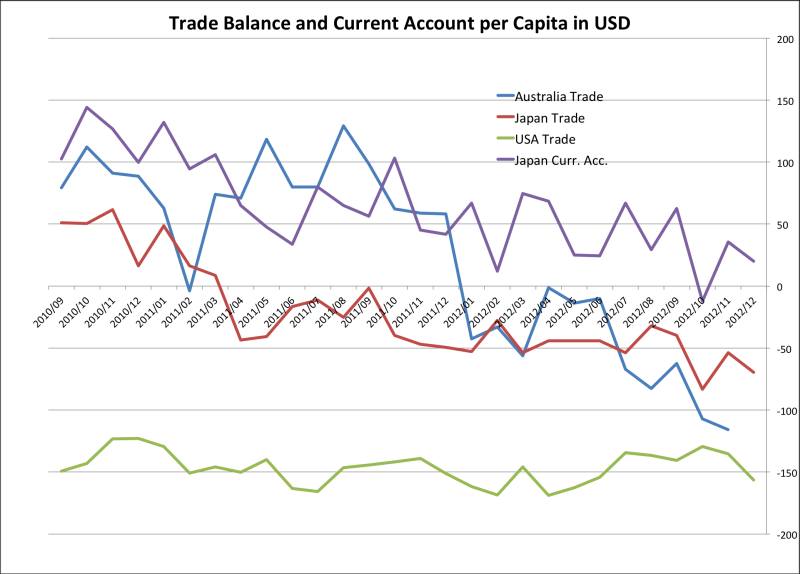

Japanese Currency Debasement, Part 1: Current Account and Japanese Bond Bears30 Jan 2013

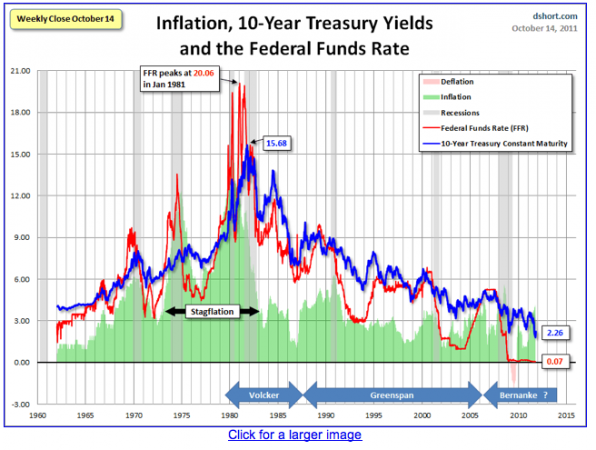

The Biggest Bubble of the Century is Ending: Government Bond Yields26 Dec 2012

May Japan face a weak yen and high bond yields?7 Dec 2012