Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

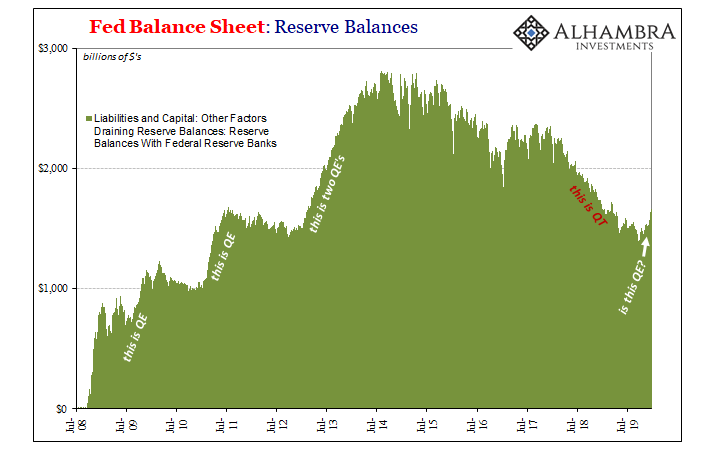

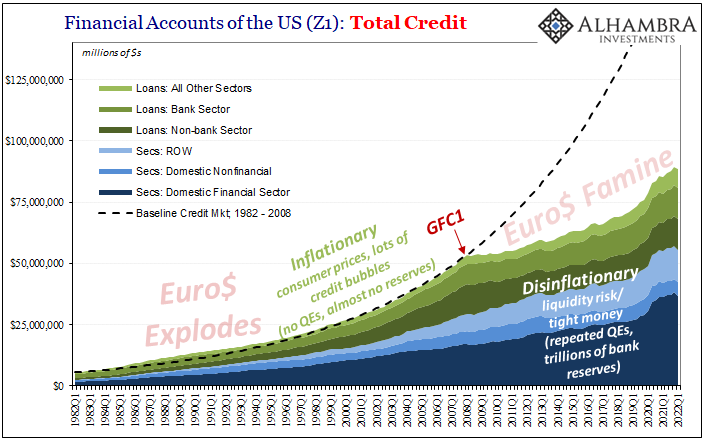

The Everything Data’s (Z1) Verdict: Not Inflation, Only More Of The Same

The Everything Data’s (Z1) Verdict: Not Inflation, Only More Of The Same26 Jun 2022

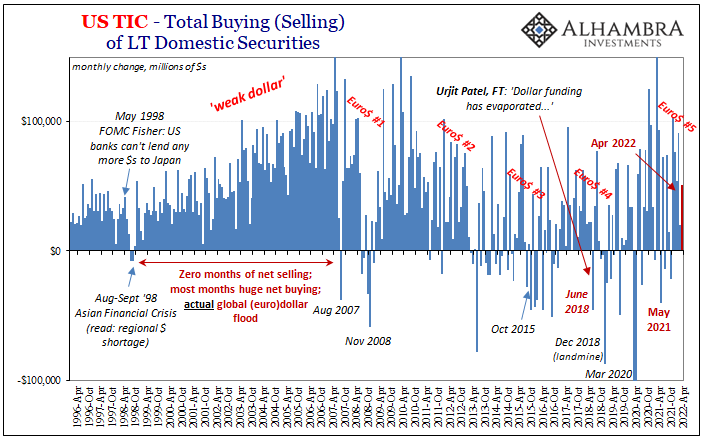

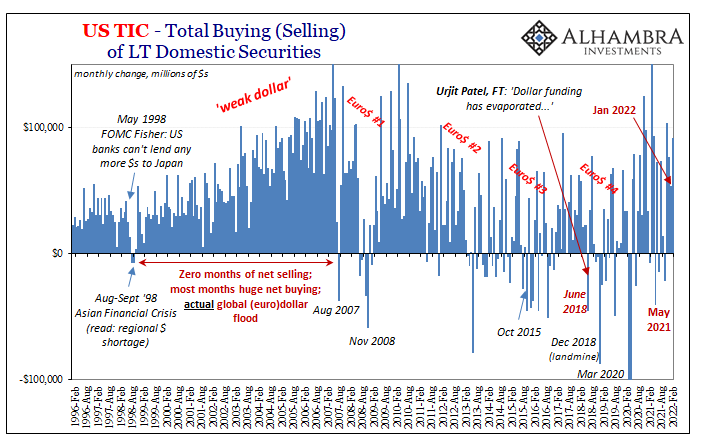

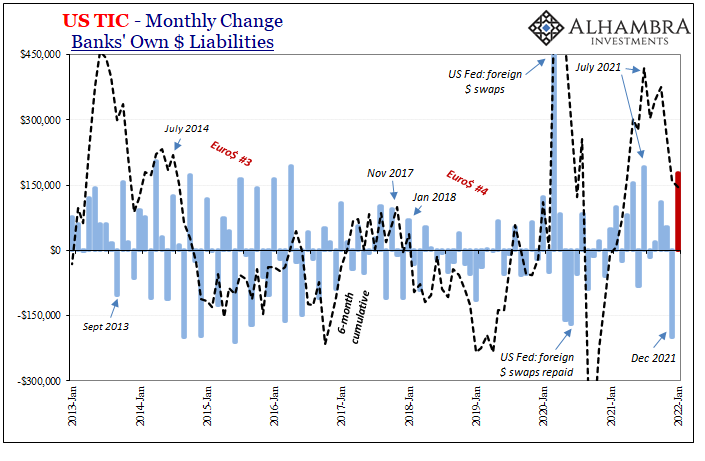

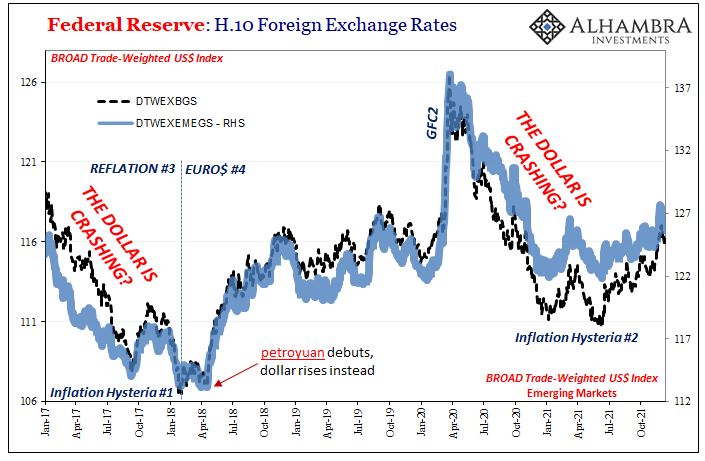

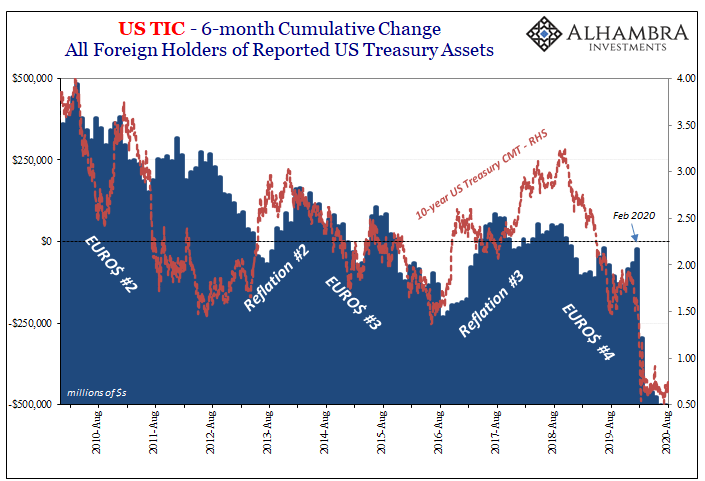

Angry April TIC Zeroed In On China’s CNY and Japan’s JPY

Angry April TIC Zeroed In On China’s CNY and Japan’s JPY21 Jun 2022

Hong Kong Stocks Pivot Euro$ #5

Hong Kong Stocks Pivot Euro$ #528 May 2022

Looking Back At Chaotic March Through TIC

Looking Back At Chaotic March Through TIC20 May 2022

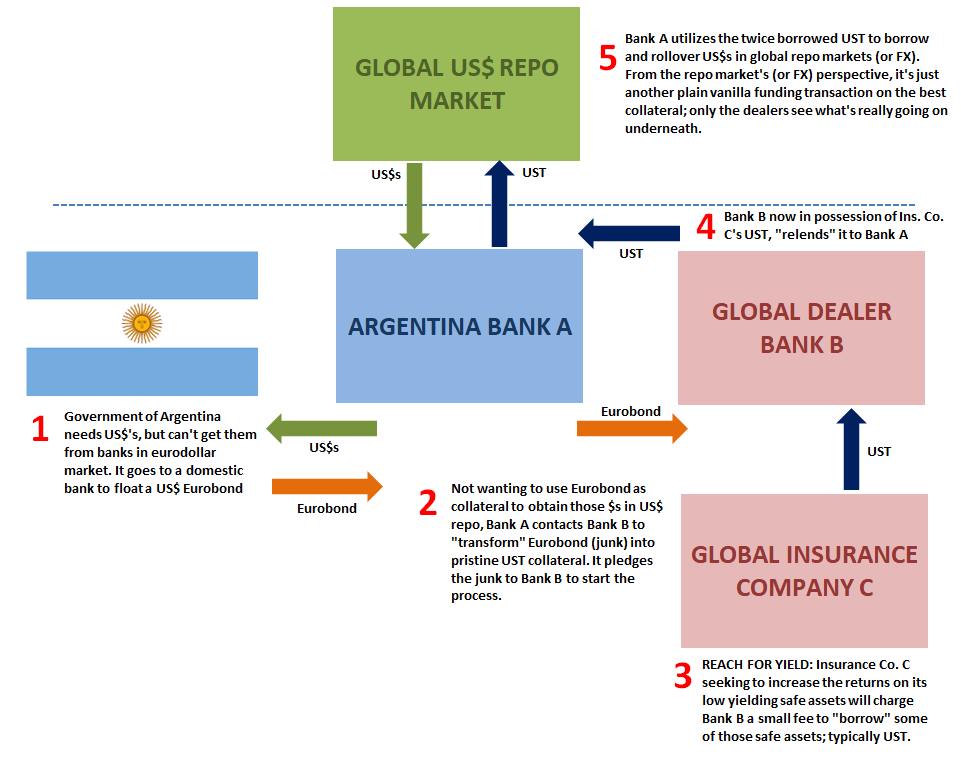

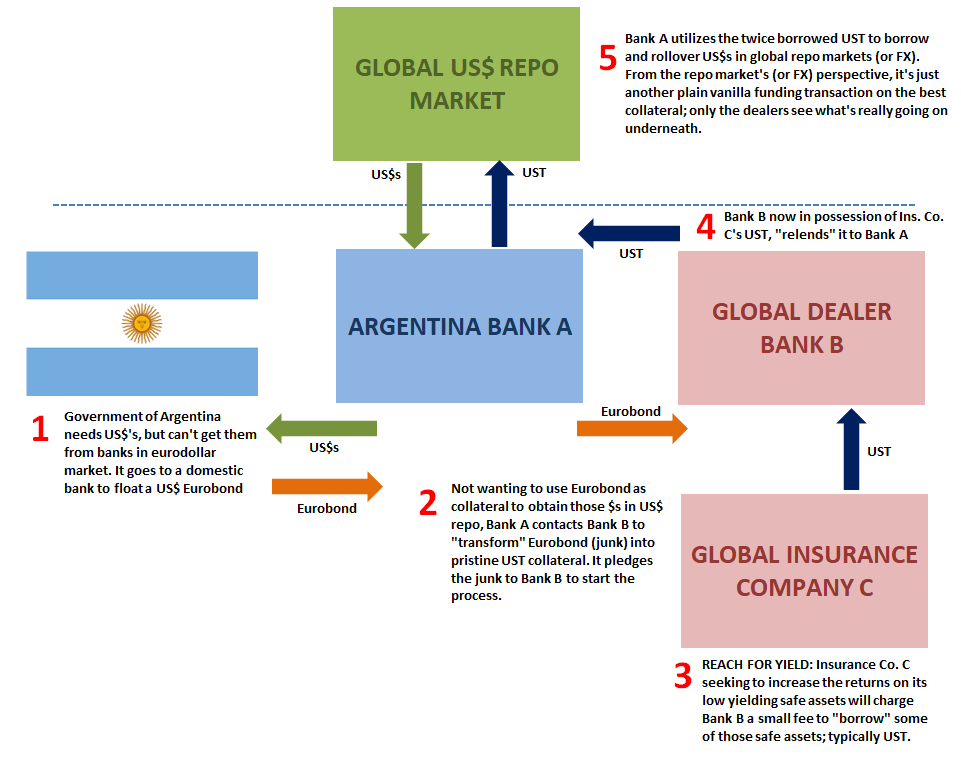

Eurobonds Behind Euro$ #5’s Collateral Case

Eurobonds Behind Euro$ #5’s Collateral Case12 May 2022

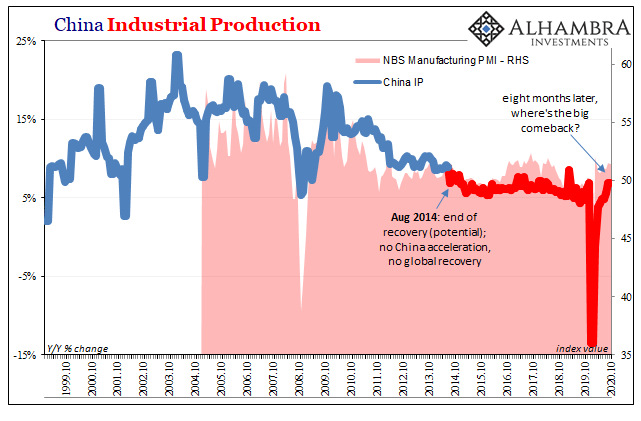

China, Japan, And The Relative Pre-March Euro$ Calm In February

China, Japan, And The Relative Pre-March Euro$ Calm In February22 Apr 2022

It Wouldn’t Be TIC Without So Much Other

It Wouldn’t Be TIC Without So Much Other23 Mar 2022

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)14 Jan 2022

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation13 Oct 2021

Taper *Without* Tantrum

Taper *Without* Tantrum17 Aug 2021

A Clear Balance of Global Inflation Factors

A Clear Balance of Global Inflation Factors30 Jun 2021

There’s Two Sides To Synchronize

There’s Two Sides To Synchronize3 Mar 2021

The Endangered Inflationary Species: Gazelles

The Endangered Inflationary Species: Gazelles11 Feb 2021

Consumers, Too; (Un)Confident To Re-engage

Consumers, Too; (Un)Confident To Re-engage19 Dec 2020

Treasury Auctions Are Anything But Sorry Because They’ve Never Been Sorry About Solly

Treasury Auctions Are Anything But Sorry Because They’ve Never Been Sorry About Solly28 Nov 2020

Six Point Nine Times Two Equals What It Had In Twenty Fourteen

Six Point Nine Times Two Equals What It Had In Twenty Fourteen17 Nov 2020

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay2 Oct 2020

What’s Zambia Got To With It (everything)

What’s Zambia Got To With It (everything)1 Oct 2020

Reopening Inertia, Asian Dollar Style (Still Waiting On The Crash)

Reopening Inertia, Asian Dollar Style (Still Waiting On The Crash)20 Sep 2020

Bottleneck In Japanese

Bottleneck In Japanese9 Sep 2020