Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Media Attention All Over FOMC, Market Attention Totally Elsewhere19 Mar 2022

Houston, We Have An Oil (and inventory) Problem7 Mar 2022

This Is A Big One (no, it’s not clickbait)2 Dec 2021

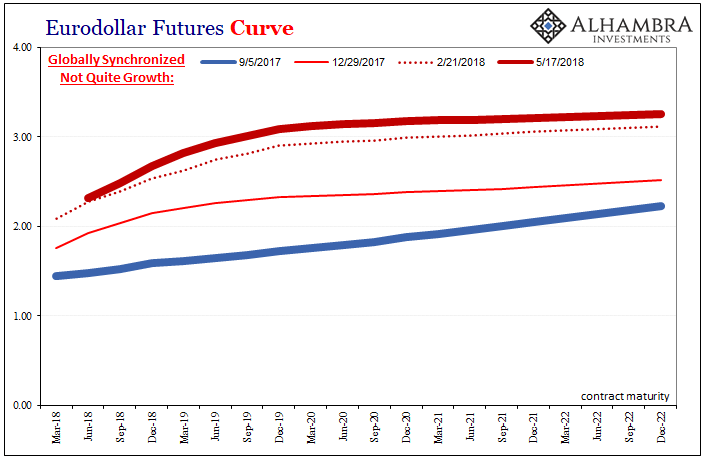

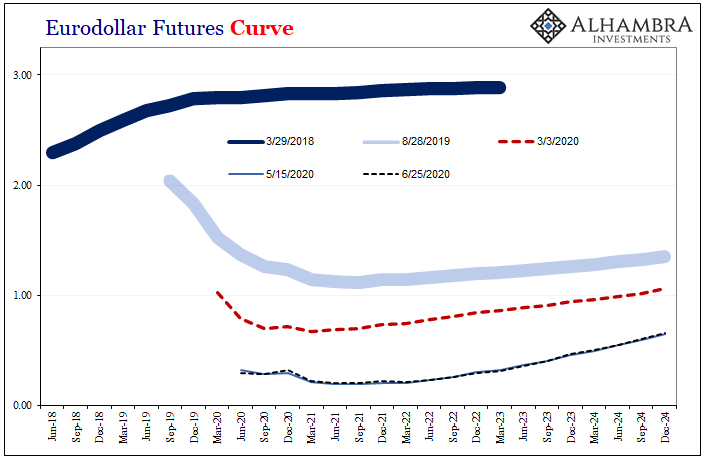

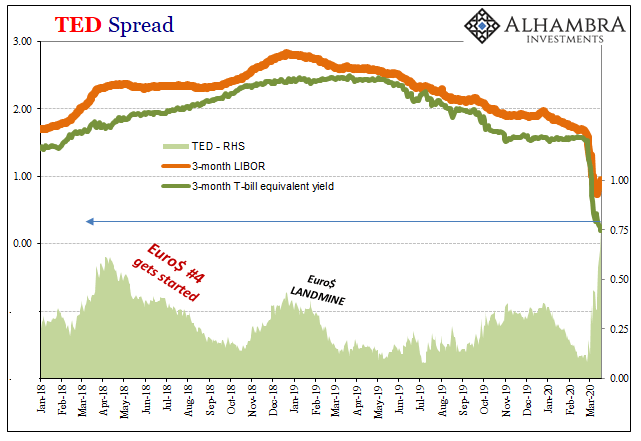

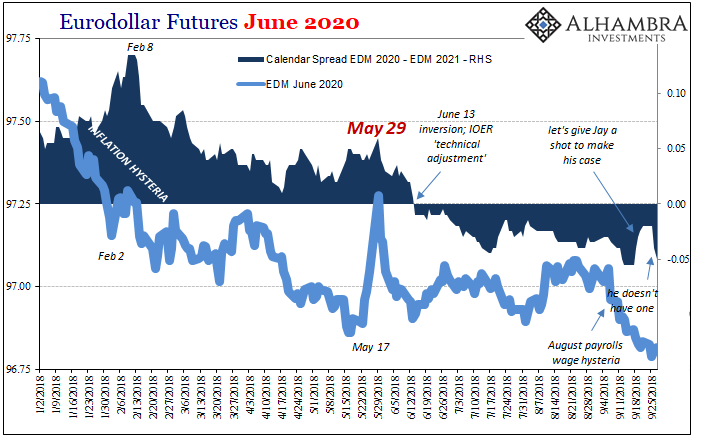

Wait A Minute, What’s This Inversion?28 Jun 2020

Is GFC2 Over?18 Mar 2020

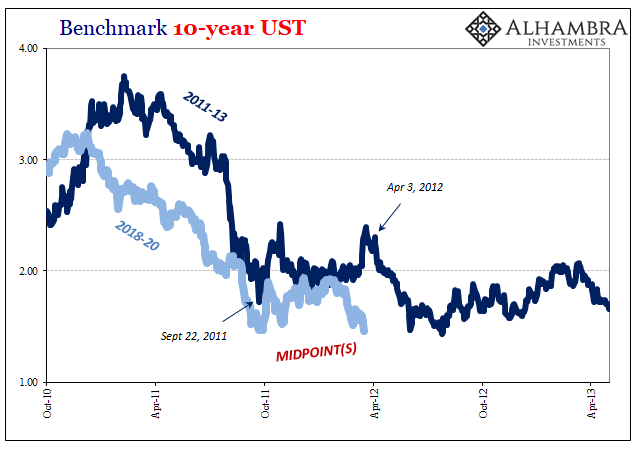

Was It A Midpoint And Did We Already Pass Through It?25 Feb 2020

What Kind Of Risks/Mess Are We Looking At?4 Jun 2019

Chart(s) of the Week: Reviewing Curve Warnings19 Mar 2019

Eurodollar Futures: Powell May Figure It Out Sooner, He Won’t Have Any Other Choice20 Nov 2018

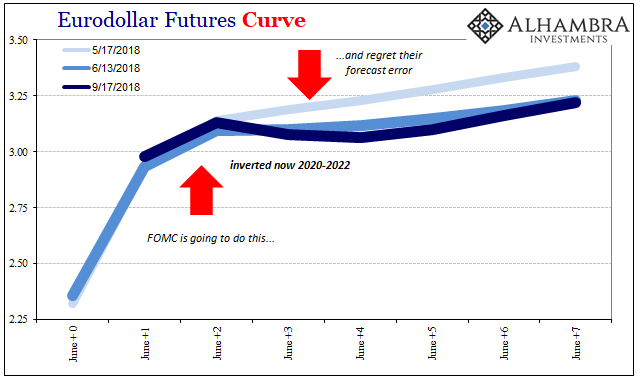

Make Your Case, Jay28 Sep 2018

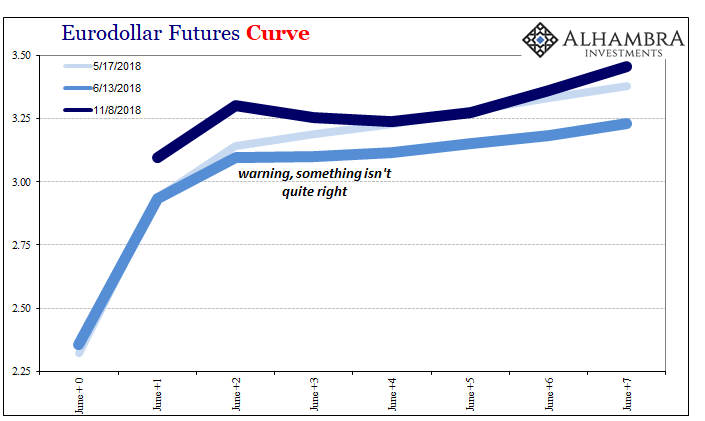

Europe Starting To Reckon Eurodollar Curve14 Sep 2018

The (Economic) Difference Between Stocks and Bonds4 Nov 2017

Swimming The ‘Dollar’ Current (And Getting Nowhere)26 Sep 2017

Moscow Rules (for ‘dollars’)

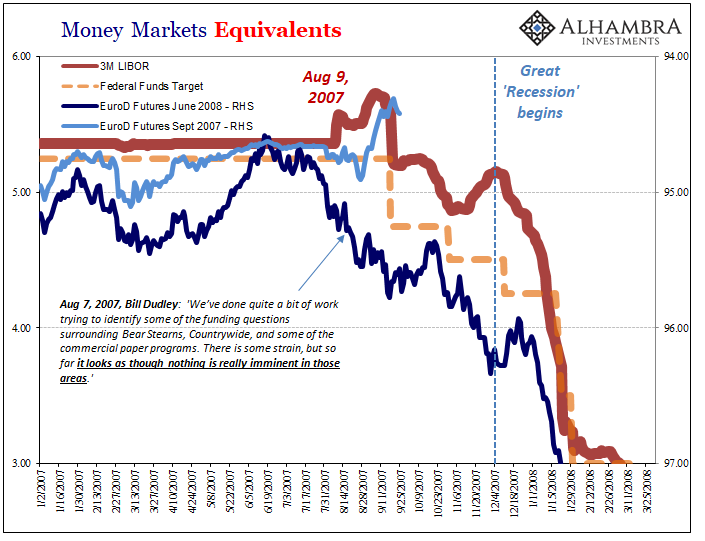

Moscow Rules (for ‘dollars’)2 Sep 2017

Repeat 2015; An Embarrassing Day For The Fed

Repeat 2015; An Embarrassing Day For The Fed24 Jun 2017

All In The Curves26 Mar 2017