Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

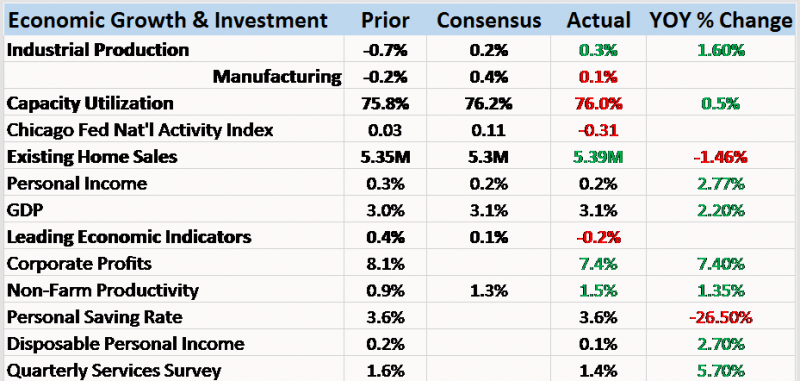

Weekly Market Pulse: The Consensus Will Be Wrong

Weekly Market Pulse: The Consensus Will Be Wrong9 Jan 2023

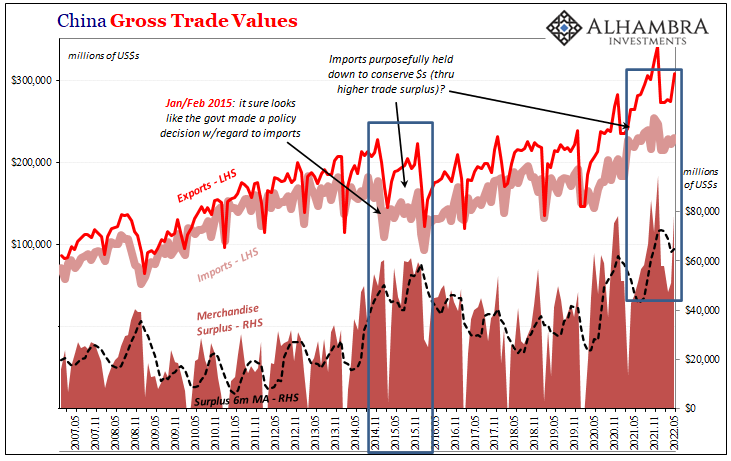

Wait A Sec, That’s Not Really An *RMB* Liquidity Pool…

Wait A Sec, That’s Not Really An *RMB* Liquidity Pool…1 Jul 2022

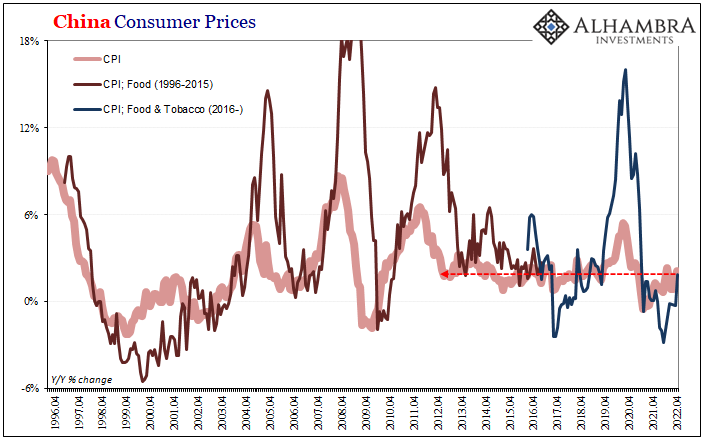

Synchronizing Chinese Prices (and consequences)

Synchronizing Chinese Prices (and consequences)14 May 2022

Who’s Playing Puppetmaster, And Who Is Master of Puppets

Who’s Playing Puppetmaster, And Who Is Master of Puppets9 May 2022

Collateral Shortage…From *A* Fed Perspective

Collateral Shortage…From *A* Fed Perspective7 May 2022

What Really ‘Raises’ The Rising ‘Dollar’

What Really ‘Raises’ The Rising ‘Dollar’3 May 2022

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai25 Apr 2022

So Much Fragile *Cannot* Be Random Deflationary Coincidences

So Much Fragile *Cannot* Be Random Deflationary Coincidences10 Mar 2022

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift1 Mar 2022

Sentiment v. Substance: Checking In On Collateral Via, Yes, The Fed

Sentiment v. Substance: Checking In On Collateral Via, Yes, The Fed13 Jan 2022

White-Hot Cycles of Silence

White-Hot Cycles of Silence28 Dec 2021

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)25 Dec 2021

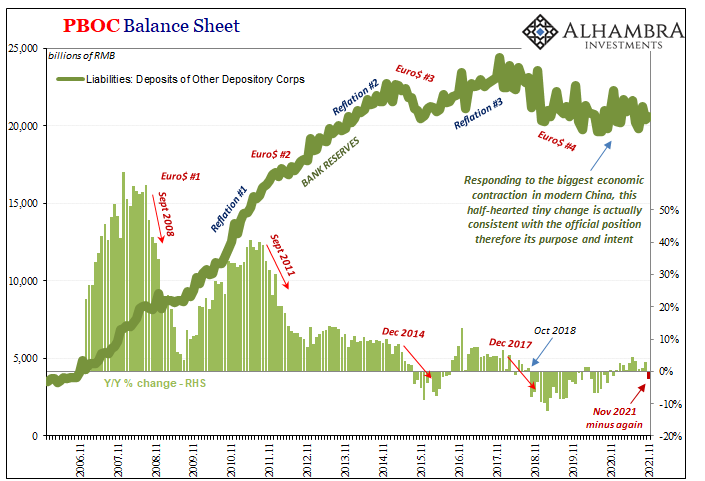

Weekly Market Pulse: Growth Scare?

Weekly Market Pulse: Growth Scare?1 Nov 2021

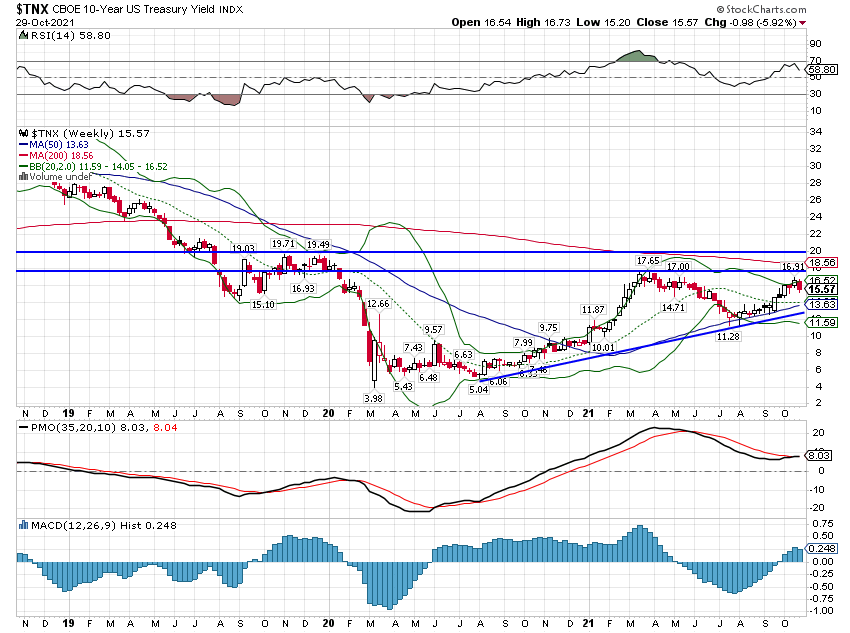

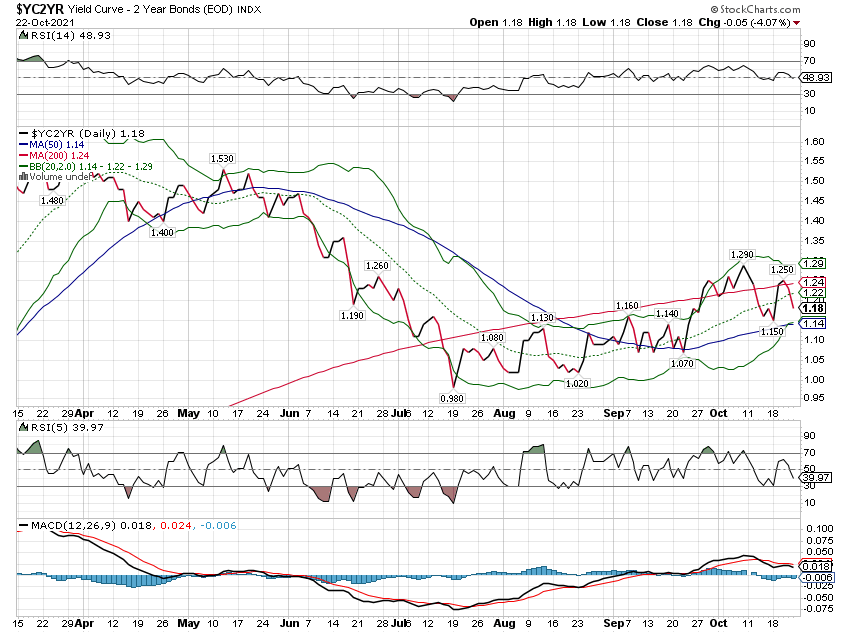

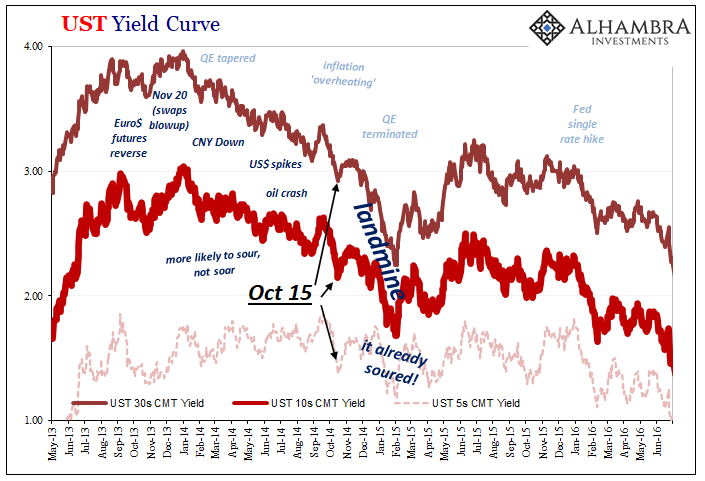

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!25 Oct 2021

Taper *Without* Tantrum

Taper *Without* Tantrum17 Aug 2021

Weekly Market Pulse: What Is Today’s New Normal?

Weekly Market Pulse: What Is Today’s New Normal?9 Aug 2021

Real Dollar ‘Privilege’ On Display (again)

Real Dollar ‘Privilege’ On Display (again)8 Apr 2021

For The Dollar, Not How Much But How Long Therefore How Familiar

For The Dollar, Not How Much But How Long Therefore How Familiar24 Feb 2021

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

Two Seemingly Opposite Ends Of The Inflation Debate Come Together19 Feb 2021

The Endangered Inflationary Species: Gazelles

The Endangered Inflationary Species: Gazelles11 Feb 2021