Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

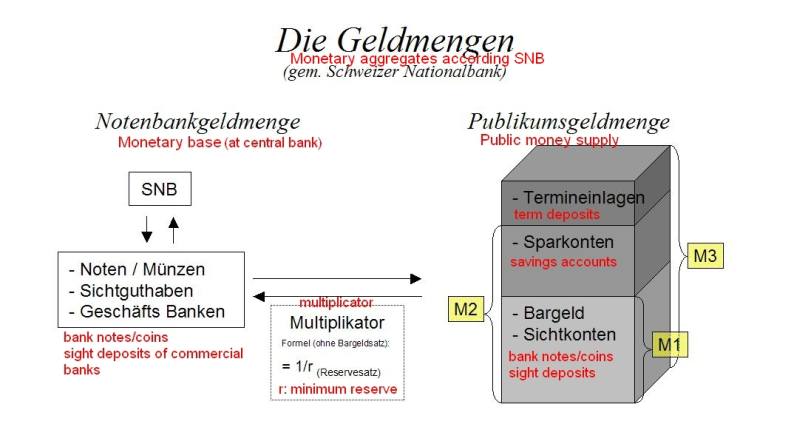

Main SNB Background Info

Digital Swiss Francs

Digital Swiss Francs5 May 2017

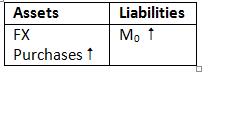

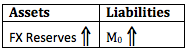

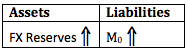

No SNB Intervention: Massive Swiss M0 Increase due to Post Finance Transformation into a Bank1 Sep 2013

SNB Monetary Data Week October 2629 Oct 2012

SNB Monetary Data Week October 1922 Oct 2012

SNB Monetary Data Week October 1215 Oct 2012

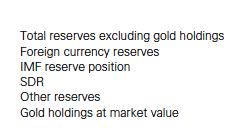

IMF Data: SNB Forex Reserves and Gold in September 201212 Oct 2012

SNB Monetary Data Week October 58 Oct 2012

SNB Monetary Data Week of September 281 Oct 2012

Do Swiss companies prefer to hold cash at the SNB instead of local banks ?24 Sep 2012

Otmar Issing’s new book on the euro crisis10 Aug 2012

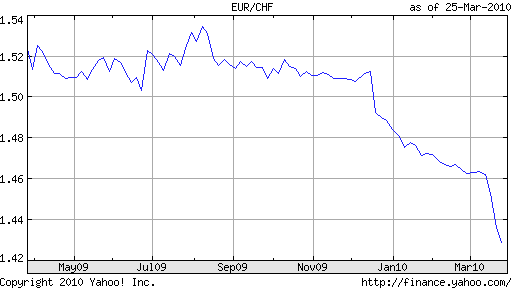

Swiss Franc Surges to Record High: Where was the SNB? (March 2010)22 Mar 2010

Recent History of the Swiss franc: March 2009

Recent History of the Swiss franc: March 200931 Mar 2009

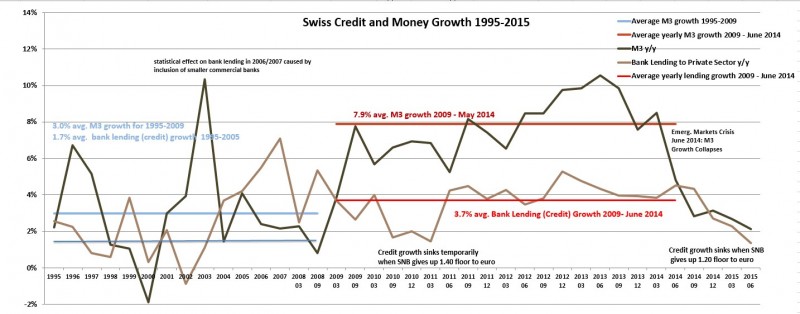

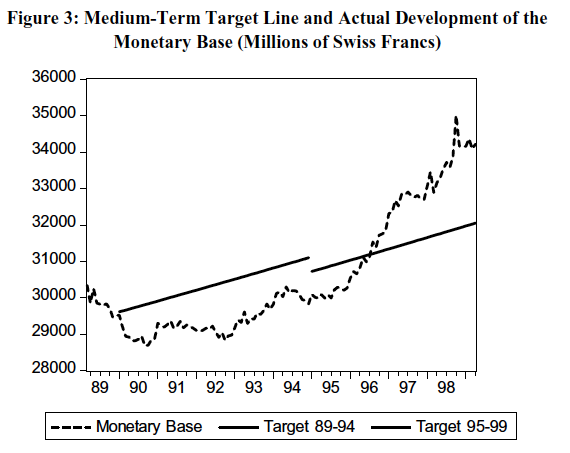

Swiss Inflation, GDP, Monetary Base between 1974 and 2000

Swiss Inflation, GDP, Monetary Base between 1974 and 200011 Aug 2003