Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

A Volcker Pan Recession

A Volcker Pan Recession10 Jun 2022

Collateral Shortage…From *A* Fed Perspective

Collateral Shortage…From *A* Fed Perspective7 May 2022

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai25 Apr 2022

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’21 Apr 2022

What Does Taper Look Like From The Inside? Not At All What You’d Think

What Does Taper Look Like From The Inside? Not At All What You’d Think5 Nov 2021

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation13 Oct 2021

Tapering Or Calibrating, The Lady’s Not Inflating

Tapering Or Calibrating, The Lady’s Not Inflating7 Oct 2021

CPI’s At Fives Yet Treasury Auctions

CPI’s At Fives Yet Treasury Auctions12 Aug 2021

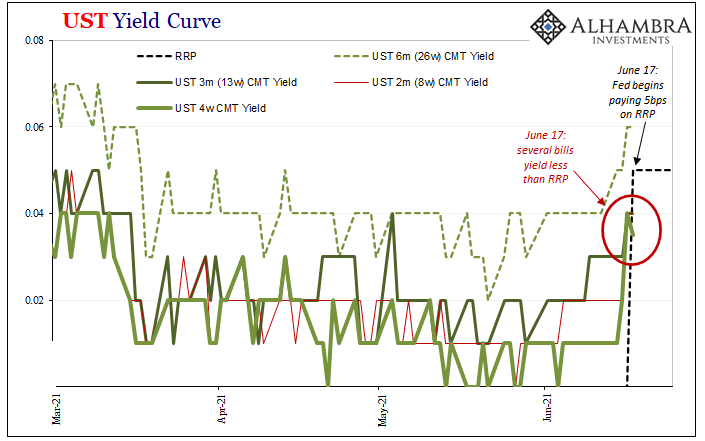

The FOMC Accidentally Exposes Itself (Reverse Repo-style)

The FOMC Accidentally Exposes Itself (Reverse Repo-style)18 Jun 2021

Rechecking On Bill And His Newfound Followers

Rechecking On Bill And His Newfound Followers9 Apr 2021

Even The People ‘Printing’ The ‘Money’ Aren’t Seeing It

Even The People ‘Printing’ The ‘Money’ Aren’t Seeing It7 Feb 2021

Meanwhile, Outside Today’s DC

Meanwhile, Outside Today’s DC5 Nov 2020

Part 2 of June TIC: The Dollar Why

Part 2 of June TIC: The Dollar Why21 Aug 2020

Wait A Minute, The Dollar And The Fed’s Bank Reserves Are Directly Not Inversely Related

Wait A Minute, The Dollar And The Fed’s Bank Reserves Are Directly Not Inversely Related17 Jul 2020

Why The FOMC Just Embraced The Stock Bubble (and anything else remotely sounding inflationary)

Why The FOMC Just Embraced The Stock Bubble (and anything else remotely sounding inflationary)14 Jun 2020

There Was Never A Need To Translate ‘Weimar’ Into Japanese

There Was Never A Need To Translate ‘Weimar’ Into Japanese17 May 2020

Everyone Knows The Gov’t Wants A ‘Controlled’ Weimar

Everyone Knows The Gov’t Wants A ‘Controlled’ Weimar9 May 2020

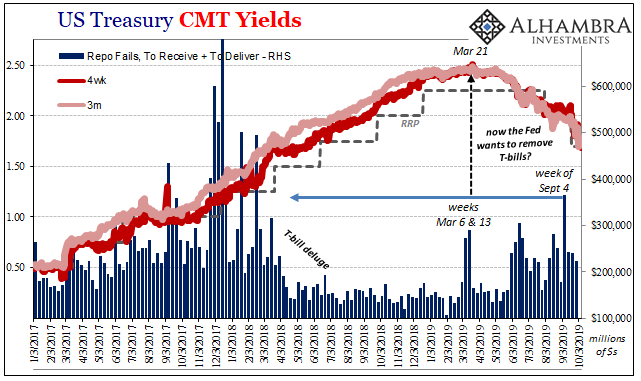

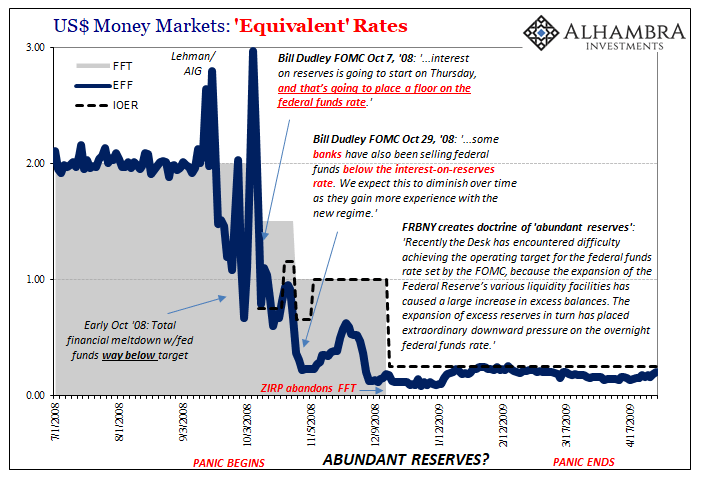

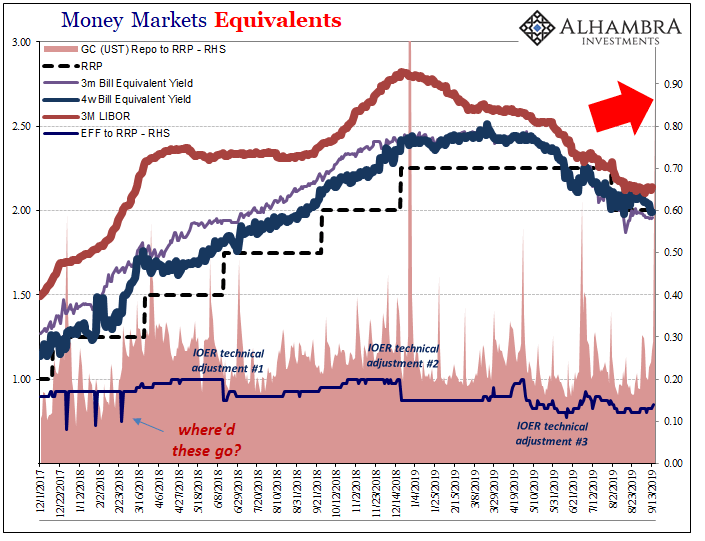

2019: The Year of Repo

2019: The Year of Repo4 Jan 2020

A Repo Deluge…of Necessary Data

A Repo Deluge…of Necessary Data18 Dec 2019

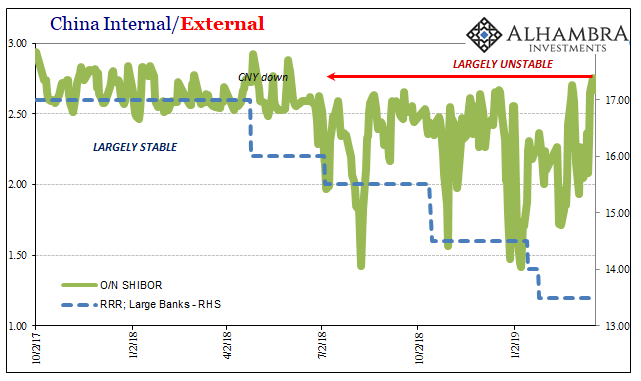

China’s Financial Stability: A Squeeze and a Strangle

China’s Financial Stability: A Squeeze and a Strangle27 Nov 2019