Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: Happy Days Are Here Again!

Weekly Market Pulse: Happy Days Are Here Again!7 Feb 2023

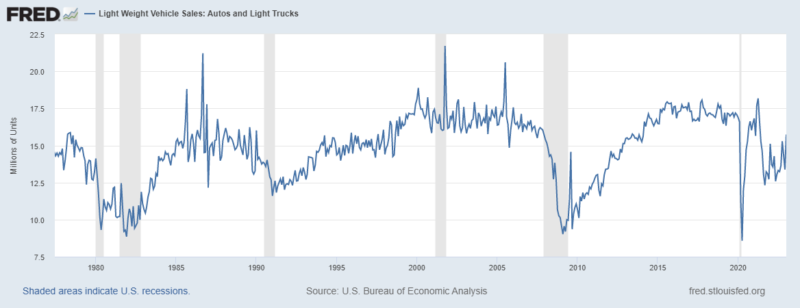

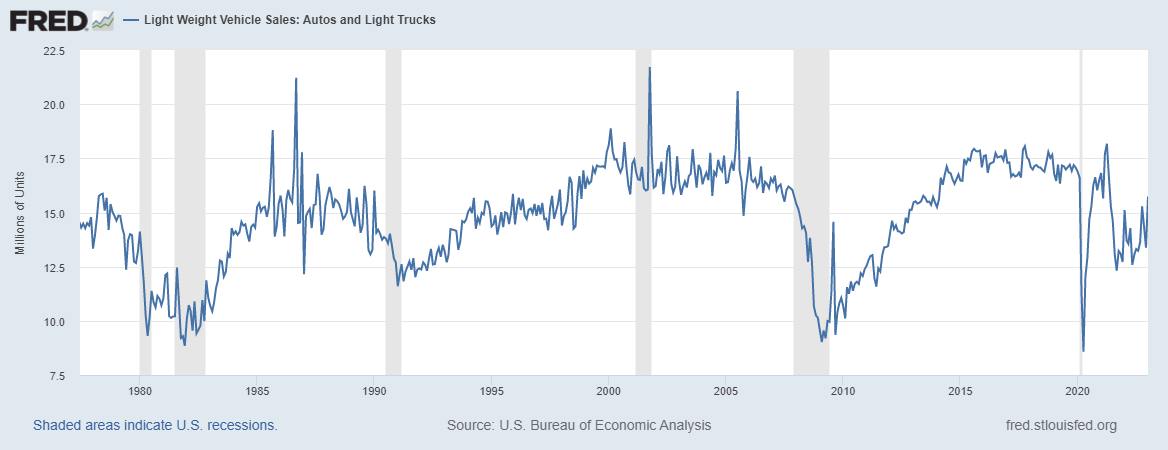

Spending Here, Production There, and What Autos Have To Do With It17 Mar 2021

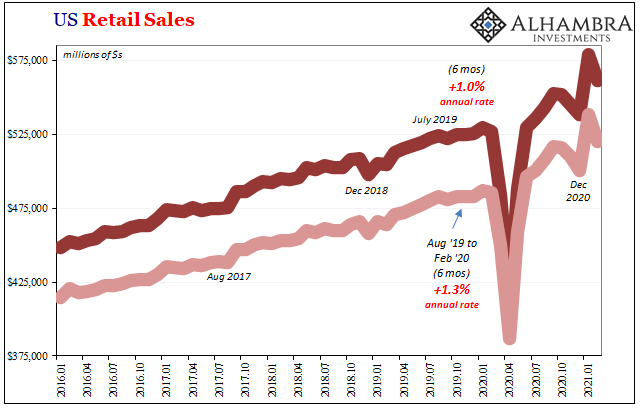

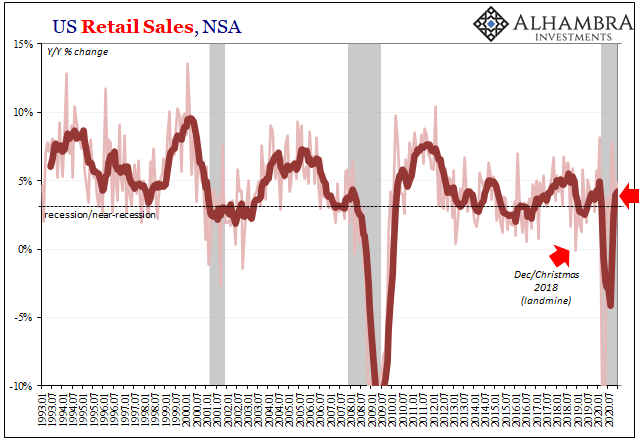

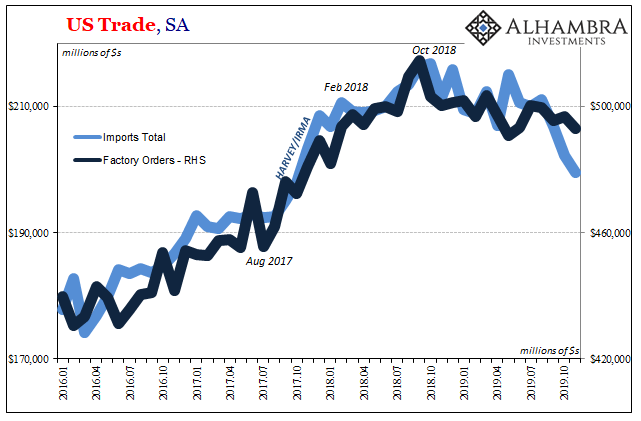

Consumers, Producers, and the Unsettled End of 202017 Jan 2021

Extending the Summer Slowdown20 Nov 2020

More Trends That Ended 2019 The Wrong Way8 Jan 2020

China Data: Something New, or Just The Latest Scheduled Acceleration?18 Dec 2019

Dollar (In) Demand12 Sep 2019

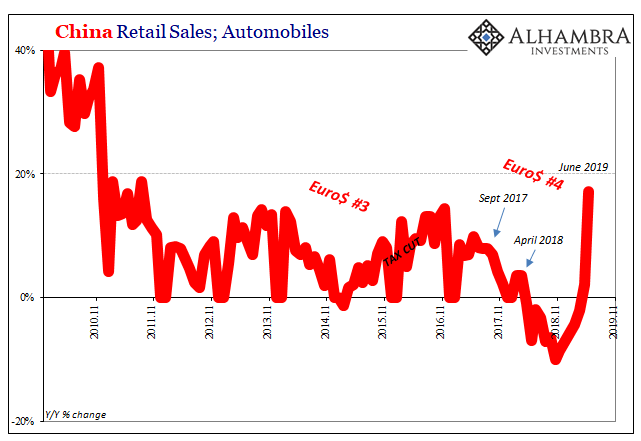

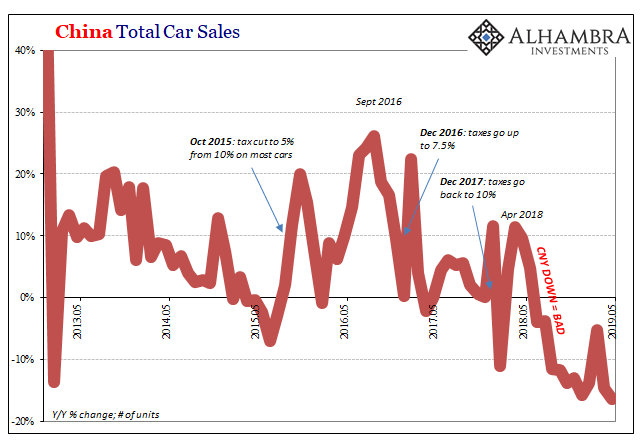

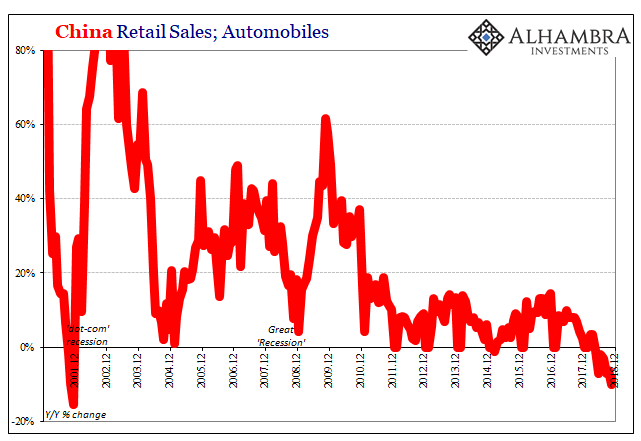

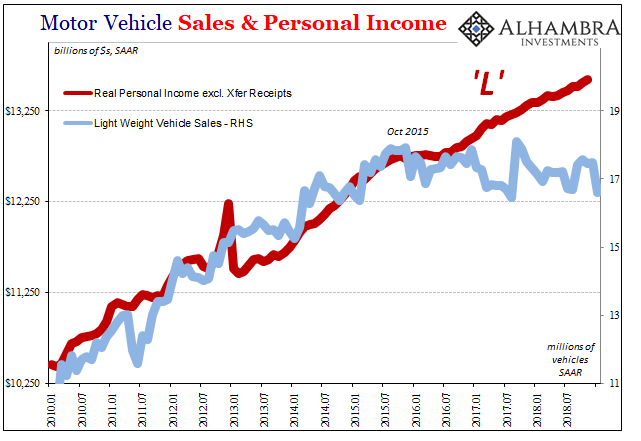

Dimmed Hopes In China Cars, Too15 Jun 2019

Something Different About This One22 Feb 2019

Getting Back Up To Speed On Loss Of Speed in US Economy21 Feb 2019

Industrial Fading19 Dec 2018

Sometimes Bad News Is Just Right16 Dec 2018

Just The One More Boom Month For IP18 Oct 2018

Now Back To Our Regularly Scheduled Economy

Now Back To Our Regularly Scheduled Economy17 Oct 2018

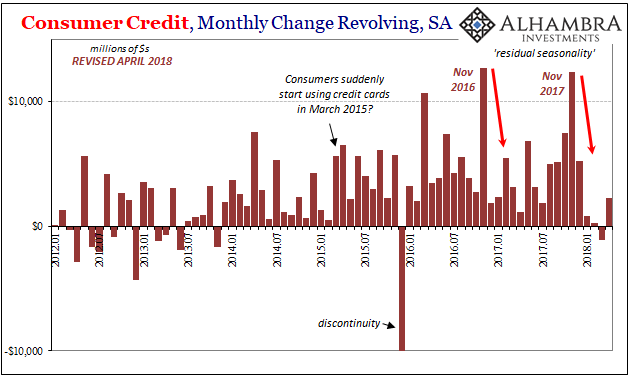

Recent Concerning Consumer Credit Trends Carry On Into April16 Jun 2018

Globally Synchronized Asynchronous Growth26 May 2018

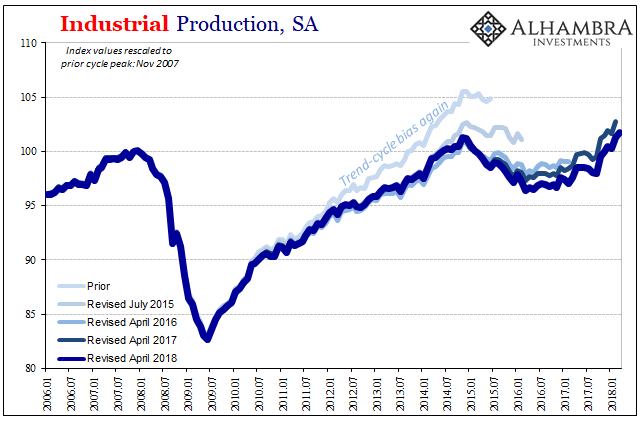

Why The Last One Still Matters (IP Revisions)26 Apr 2018

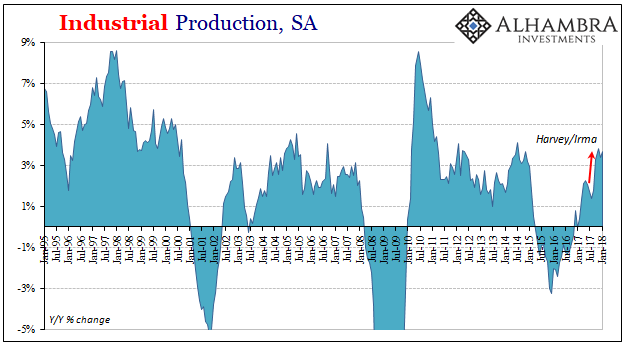

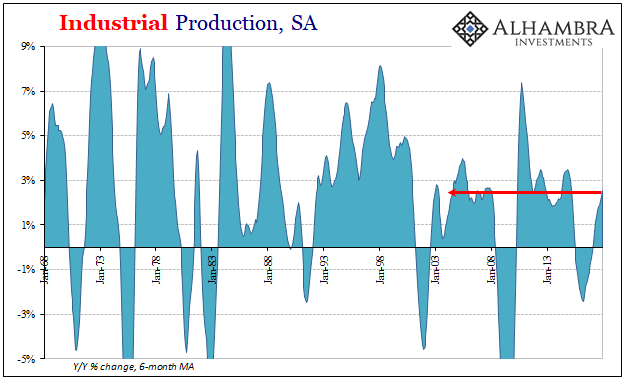

US IP On The Other Side of Harvey and Irma19 Feb 2018

Is Un-Humming A Word? It Might Need To Become One19 Jan 2018

The Economy Likes Its IP Less Lumpy23 Dec 2017