Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Harald Leschs Kernkraft GAU!

Harald Leschs Kernkraft GAU!20 May 2024

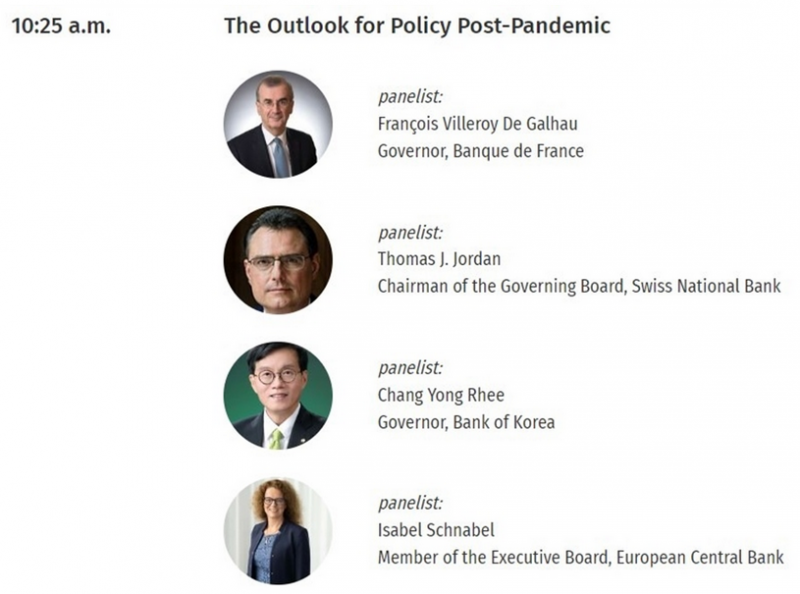

5-20-24 Disinflation Remains The Bigger Risk

5-20-24 Disinflation Remains The Bigger Risk20 May 2024

Nächste Polit-Bombe für die Grünen!

Nächste Polit-Bombe für die Grünen!20 May 2024

WDR Skandal: Georg Restle dreht völlig durch!

WDR Skandal: Georg Restle dreht völlig durch!20 May 2024

Wichtige Morning News mit Oliver Klemm #299

Wichtige Morning News mit Oliver Klemm #29920 May 2024

Fake-Mail von der “Sparkasse” #shorts

Fake-Mail von der “Sparkasse” #shorts20 May 2024

Eilmeldung: Ermittlungen gegen von der Leyen AUSGESETZT!

Eilmeldung: Ermittlungen gegen von der Leyen AUSGESETZT!19 May 2024

BMW vs Mercedes Benz #marketcap

BMW vs Mercedes Benz #marketcap19 May 2024

Faeser eskaliert komplett!

Faeser eskaliert komplett!19 May 2024

Unser Kapitaltag in Hannover (Max Otte, Helmut Reinhardt & Florian Günther)

Unser Kapitaltag in Hannover (Max Otte, Helmut Reinhardt & Florian Günther)19 May 2024

Was taugen Smartsteuer, Taxfix, WISO & co.? Beste Steuer-Apps & Programme! | Steuererklärung 2023

Was taugen Smartsteuer, Taxfix, WISO & co.? Beste Steuer-Apps & Programme! | Steuererklärung 202319 May 2024

Achtung: Extra-Gebühr bei Lieferando

Achtung: Extra-Gebühr bei Lieferando19 May 2024

Wärmepumpen Markt bricht zusammen!

Wärmepumpen Markt bricht zusammen!18 May 2024

Everyone’s excited about central banks, but they’re not the only ones buying gold!

Everyone’s excited about central banks, but they’re not the only ones buying gold!18 May 2024

Massiver Tumult vor AfD Parteitag in Essen!

Massiver Tumult vor AfD Parteitag in Essen!18 May 2024

Brisante Eilmeldung aus dem Gerichtssaal

Brisante Eilmeldung aus dem Gerichtssaal18 May 2024

6 Monate ohne Gehalt leben? Für die meisten Deutschen kein Problem! #gehalt

6 Monate ohne Gehalt leben? Für die meisten Deutschen kein Problem! #gehalt18 May 2024

How Nations Escape Poverty – Vietnam & Capitalism

How Nations Escape Poverty – Vietnam & Capitalism18 May 2024

Spektakulärer Aussetzer! Als Helge Lindh (SPD) die Nerven verlor!

Spektakulärer Aussetzer! Als Helge Lindh (SPD) die Nerven verlor!18 May 2024

Unwirksame Klauseln im Mietvertrag #shorts

Unwirksame Klauseln im Mietvertrag #shorts18 May 2024