Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Understanding Elliott Wave Theory and Investment Strategies – Andy Tanner and Bob Prechter

Understanding Elliott Wave Theory and Investment Strategies – Andy Tanner and Bob Prechter24 Apr 2024

4-20-24 Candid Coffee – Open Season Episode

4-20-24 Candid Coffee – Open Season Episode24 Apr 2024

Habecks Geheimakten enthüllt!

Habecks Geheimakten enthüllt!24 Apr 2024

Diese Aktien sind extrem günstig!

Diese Aktien sind extrem günstig!24 Apr 2024

Bitcoin Price Prediction and the Future of Crypto – Robert Kiyosaki, Mark Moss

Bitcoin Price Prediction and the Future of Crypto – Robert Kiyosaki, Mark Moss24 Apr 2024

The DNA of Success: Habits of Millionaires Unveiled

The DNA of Success: Habits of Millionaires Unveiled24 Apr 2024

4-24-24 What Does Realistic Retirement Look Like?

4-24-24 What Does Realistic Retirement Look Like?24 Apr 2024

Eklat: Grünen Politiker wirft genervt hin!

Eklat: Grünen Politiker wirft genervt hin!24 Apr 2024

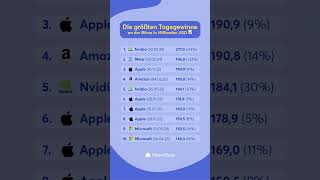

Die größten Tagesgewinne an der Börse! #highlife

Die größten Tagesgewinne an der Börse! #highlife24 Apr 2024

Heftig: Maximilian Krahs Mitarbeiter verhaftet!

Heftig: Maximilian Krahs Mitarbeiter verhaftet!24 Apr 2024

EURUSD Technical Analysis – WATCH what happens around this key resistance

EURUSD Technical Analysis – WATCH what happens around this key resistance24 Apr 2024

Happy World Book Day!

Happy World Book Day!23 Apr 2024

EURUSD has a cap near the 38.2% retracement, but buyers are pushing.

EURUSD has a cap near the 38.2% retracement, but buyers are pushing.23 Apr 2024

Skandal-Studie: MEGA Gau für Grüne!

Skandal-Studie: MEGA Gau für Grüne!23 Apr 2024

Jeder spricht über finanzielle Ziele, aber der Weg dorthin ist meistens lang und mühsam. 🧗️

Jeder spricht über finanzielle Ziele, aber der Weg dorthin ist meistens lang und mühsam. 🧗️23 Apr 2024

Der beste Hedge der Welt!

Der beste Hedge der Welt!23 Apr 2024

150€ Strafe bei Grünem Pfeil? Das musst Du wissen #shorts

150€ Strafe bei Grünem Pfeil? Das musst Du wissen #shorts23 Apr 2024

Homelab Teil 3 – Backup, 3-2-1-Regel, Offsite Sicherung, Datentransfer, LTO Tape

Homelab Teil 3 – Backup, 3-2-1-Regel, Offsite Sicherung, Datentransfer, LTO Tape23 Apr 2024

AUDUSD reacts to the weaker US data. Pair moves higher as yields move lower/stocks higher.

AUDUSD reacts to the weaker US data. Pair moves higher as yields move lower/stocks higher.23 Apr 2024

Financial Mistakes to Avoid If You’re Retiring within Five Years

Financial Mistakes to Avoid If You’re Retiring within Five Years23 Apr 2024