As the 2024 US presidential election approaches, investors worldwide are closely monitoring potential ramifications on global markets, including the euro. The outcome of this election could significantly influence currency fluctuations, trade policies, and international relations as Republican candidate Donald Trump seeks to regain the White House from the Democratic party – which has nominated …

Read More »

Category Archive: 4.) FX Theory

George Dorgan (penname) predicted the end of the EUR/CHF peg at the CFA Society and at many occasions on SeekingAlpha.com and on this blog. Several Swiss and international financial advisors support the site. These firms aim to deliver independent advice from the often misleading mainstream of banks and asset managers.

George is FinTech entrepreneur, financial author and alternative economist. He speak seven languages fluently.

(1.3.) Let’s improve the way we report FX rates

Read More »

(5.6.1) Crowther’s Balances and Imbalances of Payments: METI Paper

Read More »

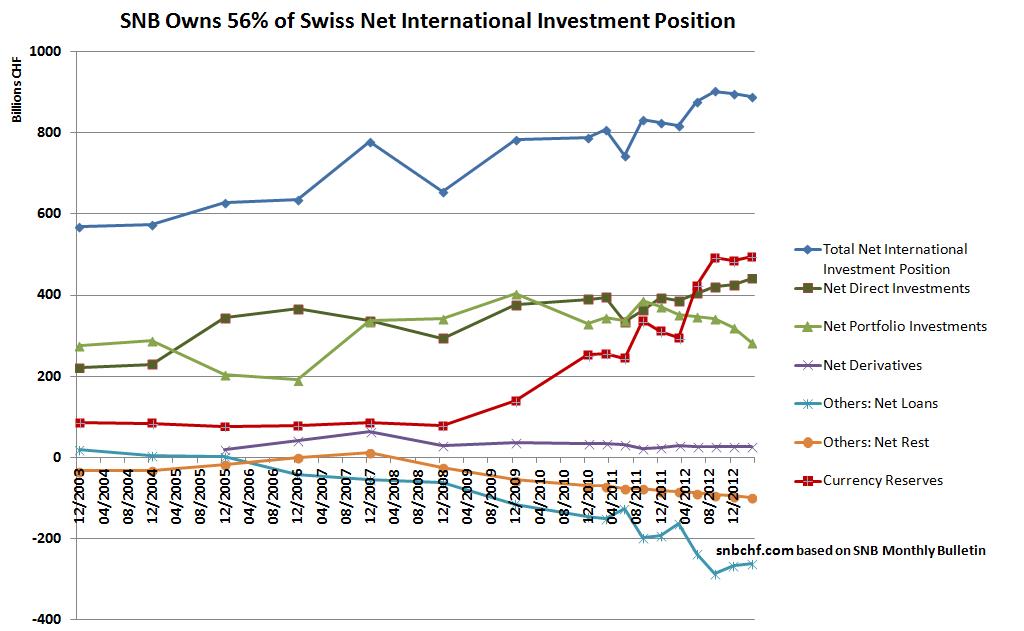

(10.1.2) Net International Investment Position Switzerland and Italy

Read More »

(1) What Determines FX Rates?

Read More »

(1.2) Explaining price movements in FX rates

Read More »

(2) FX Theory: Purchasing Power Parity

Read More »

(2.2) Purchasing Power Parity: Big Mac and Starbucks Tall Latte

Read More »

(2.3) Differences in global CPI baskets

Read More »

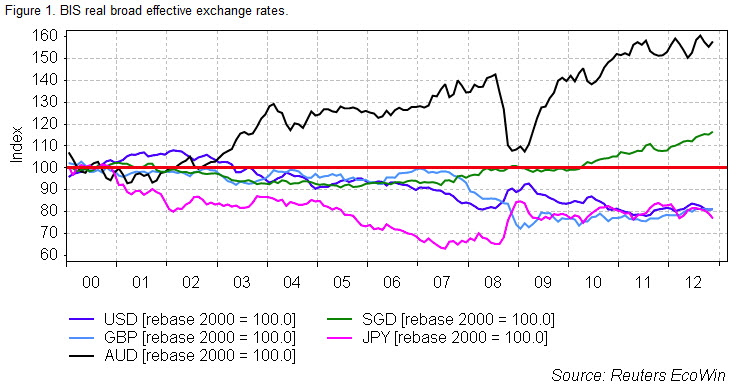

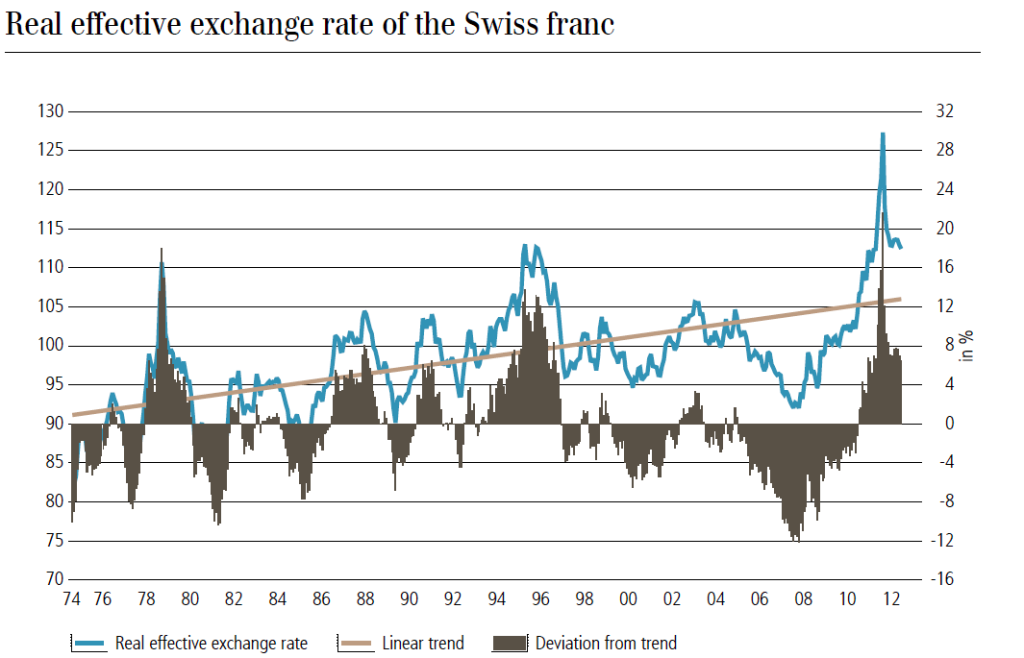

(2.5) Real Effective Exchange Rate, Swiss Franc, Yen and Renminbi

Read More »

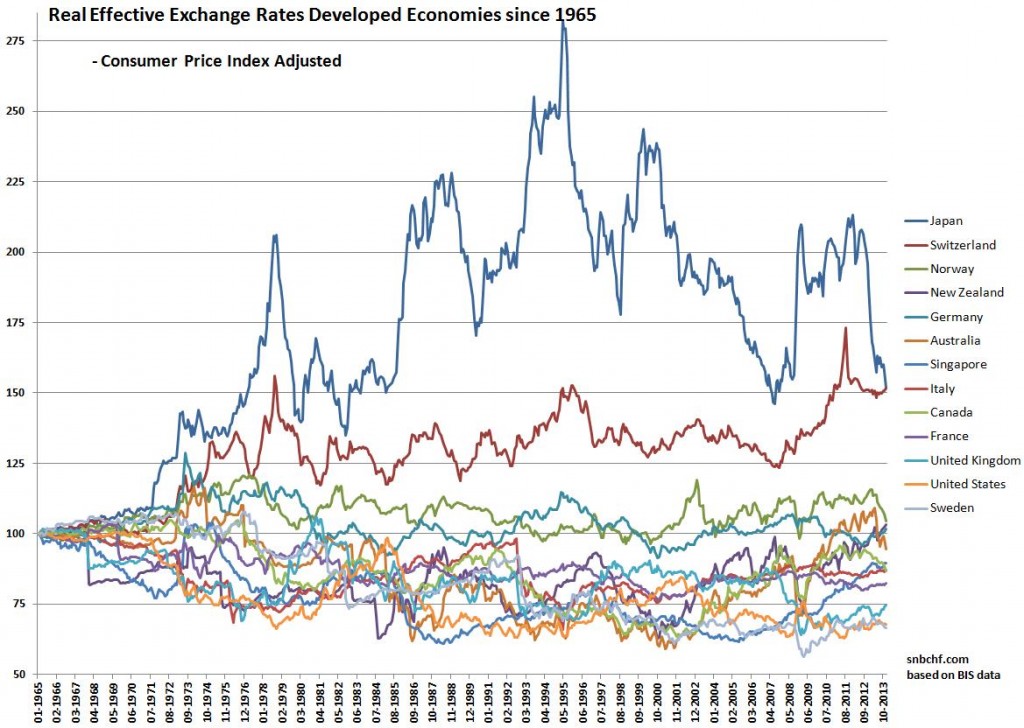

(2.6) CPI-based Real Effective Exchange Rate Since 1965: Yen Still Most Overvalued Currency

Read More »

(2.7) The Most Complete Real Effective FX Rate Comparison

Read More »

(3) Inflation, Central Banks and Interest Rates

Read More »

(3.1) FX Theory: Interest Rate Parity

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: decreased by 15 billion francs compared to the previous four weeks

-

2025-07-31 – Interim results of the Swiss National Bank as at 30 June 2025

-

SNB Brings Back Zero Percent Interest Rates

-

Hold-up sur l’eau potable (2/2) : la supercherie de « l’hydrogène vert ». Par Vincent Held

-

2025-06-25 – Quarterly Bulletin 2/2025

Main SNB Background Info

Featured and recent

-

Weniger Geschenke unter dem Weihnachtsbaum?

Weniger Geschenke unter dem Weihnachtsbaum? -

Wanderwitz dreht endgültig durch: Blamage mit AfD “Prüf-Video”

Wanderwitz dreht endgültig durch: Blamage mit AfD “Prüf-Video” -

Deutschland vor dem Kollaps? Warum alles ab 2016 aus dem Ruder lief

Deutschland vor dem Kollaps? Warum alles ab 2016 aus dem Ruder lief -

Eilmeldung: Stuttgart ist in 17 Tagen pleite!!

Eilmeldung: Stuttgart ist in 17 Tagen pleite!! -

Polit-Bombe bei EU-Finanzministern: “Niemand hat die Absicht, Bargeld einzuschränken!”

Polit-Bombe bei EU-Finanzministern: “Niemand hat die Absicht, Bargeld einzuschränken!” -

So werden Kritiker ausgeschaltet! Ganzes Interview: Heute 18 Uhr!

So werden Kritiker ausgeschaltet! Ganzes Interview: Heute 18 Uhr! -

Wie die Volatilität die Optionspreise beeinflusst

Wie die Volatilität die Optionspreise beeinflusst -

AfD in New York: plötzlich zittert der Verfassungsschutz!

AfD in New York: plötzlich zittert der Verfassungsschutz! -

Vorabpauschale 2025: Das MUSST du im Januar 2026 tun!

Vorabpauschale 2025: Das MUSST du im Januar 2026 tun! -

800 Milliarden – wofür eigentlich? Ganzes Interview: Heute 18 Uhr.

800 Milliarden – wofür eigentlich? Ganzes Interview: Heute 18 Uhr.