Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

9 Aug 2023

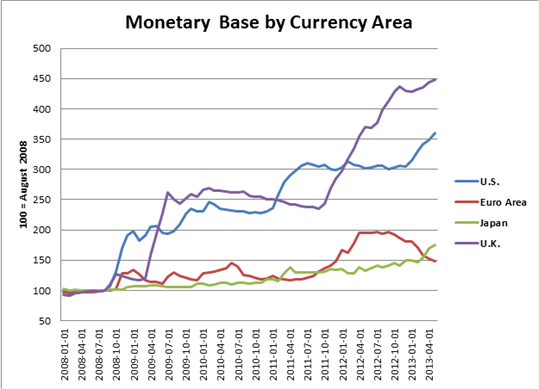

Helicopter Money and the End of Taxes

Helicopter Money and the End of Taxes1 Oct 2020

Albert Edwards: Investors Should Brace For A World Of Negative Rates, 15percent Budget Deficits And Helicopter Money

Albert Edwards: Investors Should Brace For A World Of Negative Rates, 15percent Budget Deficits And Helicopter Money8 Feb 2019

Revenu universel, du néo-libéralisme jusqu’au bout

Revenu universel, du néo-libéralisme jusqu’au bout6 Apr 2018

The Path to Inflation: “Helicopter Money”

The Path to Inflation: “Helicopter Money”6 Jun 2017

30 Oct 2016

12 Oct 2016

26 Sep 2016

A Convocation of Interventionists – Part 1

A Convocation of Interventionists – Part 16 Sep 2016

Finland Unleashes Helicopter Money In “Greatest Societal Transformation Of Our Time”

Finland Unleashes Helicopter Money In “Greatest Societal Transformation Of Our Time”31 Aug 2016

‘Last Economist Standing’ John Taylor Urges “Less Weird Policy” At Jackson Hole

‘Last Economist Standing’ John Taylor Urges “Less Weird Policy” At Jackson Hole25 Aug 2016

Incrementum Advisory Board Meeting, July 2016

Incrementum Advisory Board Meeting, July 201624 Aug 2016

The Helicopter Mortgage

The Helicopter Mortgage1 Aug 2016

Richard Koo: If Helicopter Money Succeeds, It Will Lead To 1,500 percent Inflation

Richard Koo: If Helicopter Money Succeeds, It Will Lead To 1,500 percent Inflation28 Jul 2016

A Nation of Crooks?

A Nation of Crooks?27 Jul 2016

Unsound Money Has Destroyed the Middle Class

Unsound Money Has Destroyed the Middle Class26 Jul 2016

More Signs the End is Nigh

More Signs the End is Nigh22 Jul 2016

The Central Planning Virus Mutates

The Central Planning Virus Mutates20 Jul 2016

“It’s Prohibited By Law” – A Problem Emerges For Japan’s “Helicopter Money” Plans

“It’s Prohibited By Law” – A Problem Emerges For Japan’s “Helicopter Money” Plans14 Jul 2016

Stockman Rages: Ben Bernanke Is “The Most Dangerous Man Walking This Planet”

Stockman Rages: Ben Bernanke Is “The Most Dangerous Man Walking This Planet”12 Jul 2016