Pater Tenebrarum

My articles My siteAbout meMy videosMy books

Follow on:TwitterSeeking AlphaFacebook

A Science Goes AstrayHuman beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there is, after all, the interesting fact that observers are influencing measurements at the quantum level by the act of observation. (For our lives in the “macro” world, however, this is not relevant. An engineer does not need to take relativity or quantum physics into account to construct a machine that works.) In the late 19th and early 20th centuries, a never before seen string of very rapid advances in scientific knowledge and technological progress occurred. It is hard to overstate the impact of inventions such as the automobile, radio, airplanes, and so forth. This happened while per capita economic growth in what is today known as the “developed world” reached its fastest pace in all of history — a pace never to be seen again. Although we cannot prove it, we believe there was a good reason why this combination of vast economic and scientific progress took place at the time: governments were but a footnote in the lives of most people. By 1910, spending by the US government was a mere 4% of GDP. There was no central planning and no central bank, although there was of course a certain amount of crony capitalist government intervention, and the forerunner of the Federal Reserve System (the system of “central reserve city, city and country banks”) was already established. |

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge |

Real US GNP per capita (1869-1918) (in 2009 dollars)US real GNP per capita during the so-called “Gilded Age” – it has never again grown this fast or more equitably. This happened under a fairly sound, gold-based monetary regime. Consumer price inflation was slightly negative for most of this time period. However, the astonishing advances in the natural sciences had an unfortunate side-effect: many scientists in the field of the social sciences — especially in the most developed branch of the social sciences, economics — began to develop a fascination for the methodologies of physics. They inter alia assumed that what had been lacking so far in economics was the availability of reliable statistics. Armed with the proper statistical data, so it was held, economists would not only be able to “test” the theorems of economics, but would ultimately also be able to engage in proper macroeconomic planning. As Murray Rothbard put it in the foreword to Ludwig von Mises’ book Theory and History:

|

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge |

In parallel with this, Alfred Marshall’s partial equilibrium approach as well as mathematical economics and Leon Walras’ general equilibrium approach gained greatly in prominence in economics, in stark contrast with the causal-realist approach of the subjectivist economics propagated by the Austrian School. In spite of Carl Menger having been one of the fathers of modern economics, his economic school of thought soon found itself overshadowed.

It can also be assumed that not too many economists in the Anglophone world were fully aware at the time of the extensive debate that had earlier raged in the German-speaking parts of the world over economic methodology — a dispute between economists who asserted the existence of universally and time-invariantly valid economic laws and the German historicists, who denied that such economic laws existed.

The debate continued to simmer though, and was taken up again later with some verve. Milton Friedman e.g. strongly came out in favor of positivism in economic science. The reality of the matter is of course that if one looks closely at the arguments of those favoring empiricism in economics, it soon turns out that they too believe in the existence of economic laws — and are usually blissfully unaware of the contradiction this implies.

One may well wonder: if universally valid economic laws exist, why do economists seem so uniquely unable to come up with correct predictions? Well, they are neither speculators nor entrepreneurs, so as a rule they have no special talent for forecasting the future. Also, contrary to what seems to be widely assumed, furnishing precise predictions is actually not the task of economic science.

Sound economic knowledge can merely help to constrain one’s forecasts. One could also say that economic laws suggest that certain things are simply not possible. The fact that every slice of economic history is slightly different from every other, or the fact that economic development in different cultures seems to proceed differently, is due to what one can call “contingent circumstances”.

At any given point in time, a multitude of factors is at work in the economy, many of which are subject to varying leads and lags to boot. These are what produce concrete historical outcomes — but underneath, economic laws are always operative. For example, the law of marginal utility will never be suspended and empirical testing is certainly not needed to ascertain its validity.

The positivists actually have it the wrong way around: one cannot use economic statistics or economic history to explain or advance economic theory. It is exactly the other way around: one must (inter alia) employ sound economic theory if one wants to properly interpret economic history.

The Economy as a Machine

We first became aware of Ray Dalio of Bridgewater a few years ago when we happened across an article extolling his success as a fund manager. Evidently, he and his team do indeed excel in asset management; we imagine it cannot be easy to achieve the strong long-term returns Bridgewater can boast of with funds of such immense size in terms of assets under management.

Later, Dalio came to our attention again as a critic of the Federal Reserve’s quantitative easing program and incidentally as someone who wisely pointed out that the monetary experiments of modern-day central banks strongly suggest that one should hold gold as an insurance policy. Still later, Bridgewater published a lengthy report entitled “How the Economic Machine Works”, which laid out Mr. Dalio’s economic views and the associated policy recommendations, topics to which he returns frequently in interviews in the financial media.

We think he is a much better investor than economist. We want to stress that we don’t want to pick on Mr. Dalio, but rather wish to refer to his paper as an example that helps to make a general point. It should also be pointed out that the study of historical cycles is a perfectly legitimate way for an investor or speculator, and even an entrepreneur, to proceed. But it is not economics. As Ludwig von Mises notes in this context (in Human Action, p. 334):

“In order to see his way in the unknown and uncertain future man has within his reach only two aids: experience of past events and his faculty of understanding. Knowledge about past prices is a part of this experience and at the same time the starting point of understanding the future.”

| The faculty of “understanding” is the main talent of the historian. The reasoning of a speculator, as Mises says elsewhere, is akin to that of a man “looking with the eyes of a historian into the future”. However, although history is part of what Mises termed the sciences of human action (or praxeology, a term he introduced to replace the in his view tainted term sociology), it is a thymological, rather than a teleological science like economics.

Correctly applied, it makes use of a mixture of the empirical data of history as well as the deductively ascertained laws of praxeology and combines them by applying “understanding”. To clear up the meaning of the latter term: a historian, for example, knows that Caesar crossed the Rubicon — this is an established datum. But in order to convey why Caesar did so, what precisely motivated his actions, he has to apply understanding, by pondering all that is known about the man, the time in which he lived, his journey through life and his character. This involves just as much uncertainty as coming to conclusions about the future. The title of Mr. Dalio’s missive already foreshadowed that a critical examination would be required. The economy is actually not a “machine”, even though such analogies seem to make sense on a superficial level. Another well-known, but equally problematic, analogy is to describe the economy as being akin to an “organism”. It is certainly true that there is a division of labor and cooperation between the cells of an organism; in this sense, the comparison seems to make sense. But the processes involved are purely physiological in nature — cells don’t think or have volition. We once again quote Mises on the matter (Theory and History, pp. 252–253):

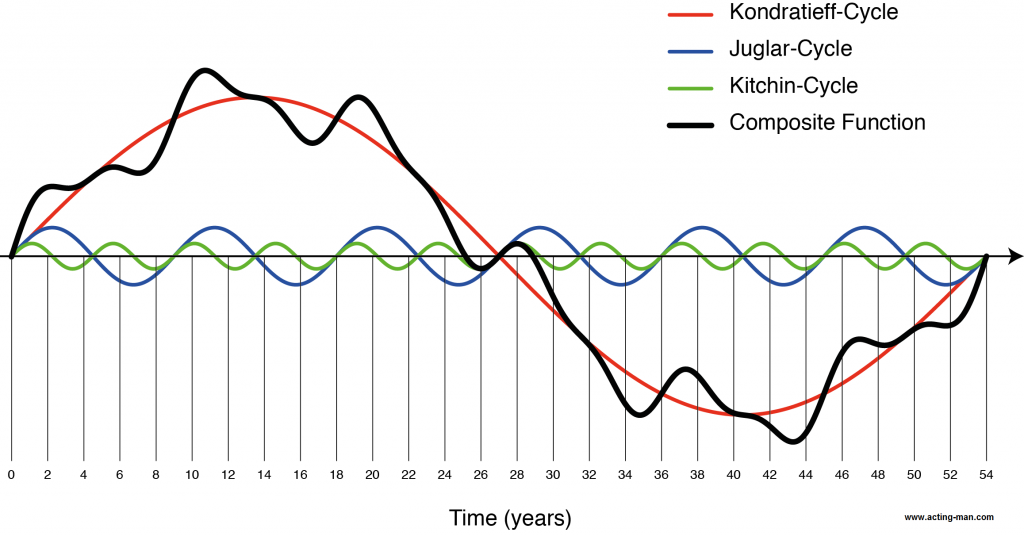

Mr. Dalio’s paper on the “economic machine” is actually quite interesting from a historical point of view. It contains examples of past debt accumulation cycles and the subsequent “deleveraging episodes”, and all of this represents quite valuable information. We would certainly regard it as helpful to investors. However, it does not explain “how the economy works” — and, more importantly, the economic policy advice derived from it is flat-out dangerous. Recall the remark we made above about many economists becoming entranced by economic statistics and econometrics in the early 20th century. One economist who tried to derive a theory on economic cycles from the study of statistics was the Russian Nikolai Kondratiev. He eventually became famous for his “Long Wave” theory of production, prices, and interest rates. The term “Long Wave” was actually popularized by Joseph Alois Schumpeter after Kondratiev’s untimely death (he was exterminated by Stalin, who deemed his theory to be “counter-revolutionary” after a US economics professor denounced Kondratiev as a closet capitalist in Moscow. Western intellectuals have always sympathized with socialism). Schumpeter tried to refine Kondratiev’s work on cycles by integrating into it shorter-term cycles, the existence of which had been posited by other economists, such as Joseph Kitchin (inventory cycle), Clement Juglar (fixed capital investment cycle), and Simon Kuznets (infrastructure and demographic/immigration cycle). |

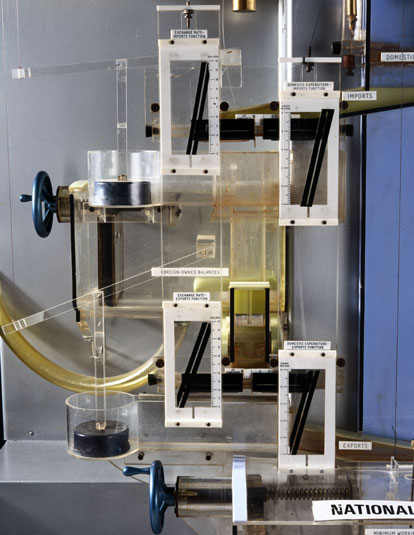

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge The “Phillips Economic Computer”, a.k.a. the “MONIAC”, designed by Bill Phillips in 1949. It is actually a great feat of engineering, but it also perfectly illustrates the mechanistic mindset that has taken root in economics (as the Science Museum in London notes, it “demonstrates in a visual way the circular flow of money within the economy” – which goes to show how superficial this mechanistic view actually is). See also the video embedded at the end of this post which shows the machine in action. |

Kondratieff-Cycle, Juglar-Cycle, Kitchin-Cycle, Composite FunctionSchumpeter’s version of the Long Wave with Kitchin and Juglar sub-cycles – the Kuznets cycle was added by later scholars and is not included in this chart (its length would be approx. 17-20 years, or one third of a Long Wave cycle). The fixed periodicity of these cycles is a mirage, and to the extent they exist, they are solely the result of credit expansion. |

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge |

| While Mr. Dalio’s paper is mainly focused on the cyclical build-up and later reduction of debt, his ideas share common ground with the “Long Wave” and its sub-cycles as it implies a similar determinism. Naturally, if the economy were indeed a machine, such determinism could be assumed to exist. While Mr. Dalio doesn’t propose that the economic cycle has a fixed periodicity, and his focus on money and credit in principle represents the correct approach, he still seems to assume an underlying deterministic process — as though a mysterious force were driving the economy, independent of human action.

Most idiosyncratic business cycle theories such as Kondratiev’s Long Wave and its subsets fail already on the grounds that there is no such thing as a non-monetary business cycle — the expansion of money and credit and the associated manipulation of interest rates are the sine qua non for the cycle to be set into motion. However, Mr. Dalio looks at credit expansion purely in a Keynesian spending-income circular flow context. The problem with this framework is that it completely misses the essential problems caused by the business cycle. |

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge |

Unsound Credit and Malinvested CapitalMr. Dalio’s main concern is the “deleveraging” part of the cycle; this is to say, a period in which more debt is paid back than is taken up and unsound debt is liquidated — or at least would be, in an unhampered free market economy. He posits that this point is generally reached once central banks are finally at the end of the “stimulus” rope — namely, once they have manipulated interest rates to zero. We would note that the subset of history on which he bases this latter assertion is one that offers an extremely small sample size. Many different monetary systems are thinkable and possible and have operated throughout history. The modern pure fiat money system is relatively young and should be seen as just one facet of the unique contingent circumstances characterizing the current economic backdrop. A term Mr. Dalio has made famous in this context is “beautiful deleveraging” — as opposed to the ugly liquidation of unsound debt by means of write-downs. As he points out, every debt is someone else’s asset, and the liquidation of unsound debt is therefore liable to create a kind of “reverse wealth effect”, by destroying the wealth of creditors. He believes this should be avoided, because it would undoubtedly be quite painful and would hamper “aggregate demand”. However, it would actually be more precise to state that the wealth that would be “destroyed” is simply wealth which creditors erroneously thought existed. By the time debt becomes unsound, this wealth has in reality already been consumed. Easy money invariably leads to the misallocation of capital, as it distorts relative prices in the economy. This in turn falsifies economic calculation, leading to malinvestment and a distortion in the time structure of production. This means that the balance between saving, investment and consumption will no longer be optimally aligned. Businessmen will underestimate current consumer demand and overestimate both currently available savings and future consumer demand. An inevitable long-term result of this is that investment is directed toward the wrong lines and capital consumption will eventually ensue. Money and credit are providing the impetus for this process, but what is actually consumed is real capital. One can of course choose to pretend that unsound debt is just fine, so as not to have to write it off — but that cannot alter the fact that real wealth has been consumed. Demand will as such never be a problem as long as there are unsatisfied human wants. The problem is rather whether the means to pay for this demand exist — and this has nothing to do with money, which is merely a medium of exchange. The wealth represented by real capital does not depend on whether the amount of money in the economy is X or Y. Or putting it differently by way of an example: If the government’s central economic planning committee gives every citizen one million rubles, but the shops are at the same time completely empty, then the money can at best be used for heating purposes. |

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge |

A Dangerous IdeaUnfortunately, the solution Mr. Dalio proposes — the thing that is supposed to make the deleveraging “beautiful” — is that central banks should print money to make debt service easier, by so to speak “inflating the debt away”. Not to put too fine a point on it, this isn’t exactly a revolutionary new idea. Rather, it is precisely one of the reasons governments have been so eager to establish central banks and a monetary system that makes nigh unlimited money creation ex nihilo possible. It is also an extremely dangerous idea (wrongly believed to work based on misunderstood historical examples). First of all, central banks have balance sheets, too — in today’s system, base money (currency and bank reserves) is their liability, which is offset by assets, most of which consist of debentures issued by governments (leaving aside that some central banks are even buying equities nowadays). These in turn are a claim on the government’s ability to tax away a sufficient amount of wealth from its citizenry in the future. The only way in which central banks can create additional money without at the same time causing an offsetting increase in debt somewhere in the system and with it the potential for this new money to disappear again (if/ when said debt is actually paid back), is by making the increase in money supply “permanent”. Note: We are not so naïve as to believe even for one second that the money supply increase they have caused so far is somehow not going to turn out to be permanent. However, in theory it isn’t: every bond on the central bank balance sheet will eventually mature. |

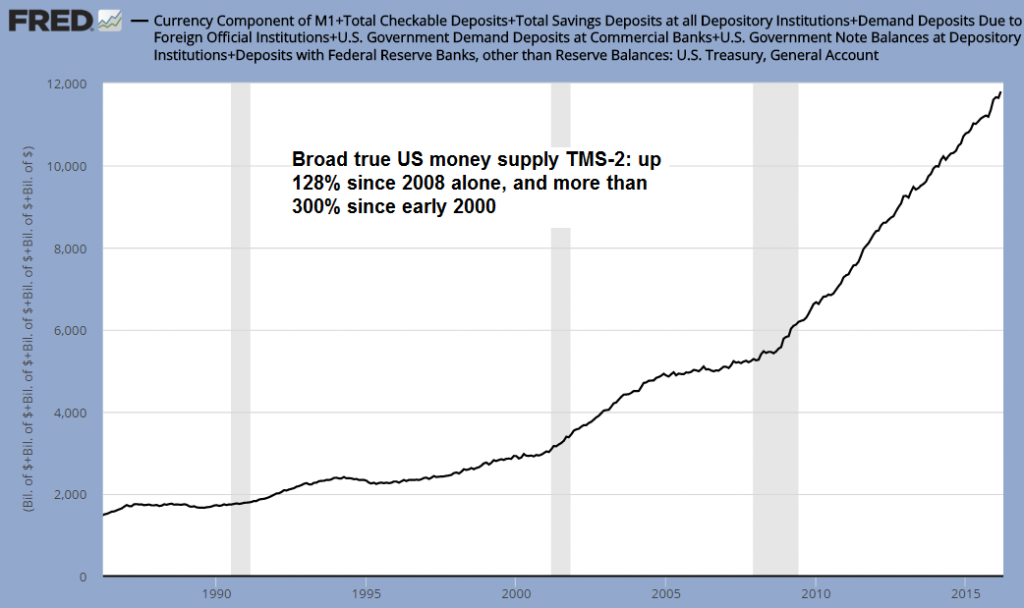

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge The true broad US money supply TMS-2 (excludes all credit transactions and includes everything that is actually money) – it is extremely unlikely that the Fed will ever allow it to shrink again. |

| Still, what Mr. Dalio seems to have in mind is more akin to some version of “helicopter money” — a form of debt monetization that is explicitly made permanent. Numerous such proposals have been making the rounds already, including the idea of simply extinguishing the debt that central banks now hold.

Presumably, it would be replaced with a $1 trillion platinum coin as Mr. Krugman once proposed in a different context — after all, something has to replace the extinguished debt on the balance sheet. A finger-painting made by Mr. Kuroda under the influence of too much sake might for instance be used by the BoJ. It could be declared a work of art worth one quadrillion yen. Another idea is for governments to issue “perpetual bonds” directly to the central bank, which will then simply grace its balance sheet for all eternity. This is supposed to encourage more spending, since citizens will no longer fear being taxed in the future so as to enable the government to repay its debt. All these ideas have a few rather major flaws in common. One of them we have already mentioned above: issuance of additional money cannot alter the state of real wealth. Not one iota in additional real capital will be created; all that will happen is that the existing supply of money will be diluted. An associated flaw is that in the longer term, even more real wealth will be consumed as a result, as nothing (money from thin air) will be exchanged for something (real resources) by the earliest recipients of the newly created money. This also implies that real wealth will be redistributed, primarily from the prudent to the well-connected and the irresponsible (and due to the uneven manner in which the price effects will spread, as a rule also from the poor to the rich). The idea that economic growth is created by “spending” is fundamentally misguided anyway; saving, wise investment and production are what creates wealth, not spending and consumption. One cannot put the cart before the horse and expect to actually get somewhere that way. There is also a considerable danger that resorting to issuing any form of “helicopter money” will simply destroy the public’s confidence in central bank-issued money. After all, the pretense that money is still “backed” by something — even if it is only the future wealth creation capability of the citizenry and the State’s ability to extract a share thereof — will then be abandoned completely. What remains to support faith in the currency after that is a thin reed, indeed. |

A Science Goes Astray Human beings have a strong tendency to look for patterns. The natural sciences have shown that the universe is governed by laws, the effects of which are observable and measurable in an objective manner. Mostly, anyway — there... - Click to enlarge |

No Painless Way Out

As much as one might want to wish for it: there is no “beautiful” or “painless” deleveraging. Both unsound credit and unsound investments will have to be liquidated eventually. All attempts to delay this process only make the prospect of this liquidation more formidable. Moreover, by now it should be obvious even to empiricists that these attempts not only create no economic growth, but are actually hampering it considerably.

It is of course true that giving market forces free rein would likely create quite a bit of short- to medium-term economic pain. The process of economic cure takes time, and the more malinvested capital and unsound debt there is, the more effort and time will be needed to restore a sound capital structure. Many assets may well change ownership in the process — economic power would shift from the beneficiaries of inflation to other members of society.

However, this period of economic pain is required to restore a sound economic foundation and with it, the basis for a resumption of sound and strong economic growth. It should not be feared. What should be feared are the ever more desperate experiments of central bankers and financial repression measures imposed by governments. The choice is only between short-term pain and long-term gain, or a long-lasting malaise followed by an even bigger catastrophe at the bitter end.

Addendum: The MONIAC in Action

One of the still working “MONIAC” machines made by Bill Phillips is demonstrated at Cambridge University. This video is both funny and slightly scary. Unfortunately, our vaunted central planners really believe that they just have to pull the right levers and the economy will run perfectly (or attain “escape velocity”, like a space ship)…

Chart sources: Wikipedia, J. Philipp for www.acting-man.com, St. Louis Federal Reserve Research

This article appeared originally in Dr. Marc Faber’s Gloom, Boom and Doom Report.

Full story here Are you the author?

Tags: Helicopter Money,Ludwig von Mises,monetization of debt,Murray Rothbard,newslettersent,On Economy,Ray Dalio