Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, March 13(see more posts on EUR/CHF, ) - Click to enlarge |

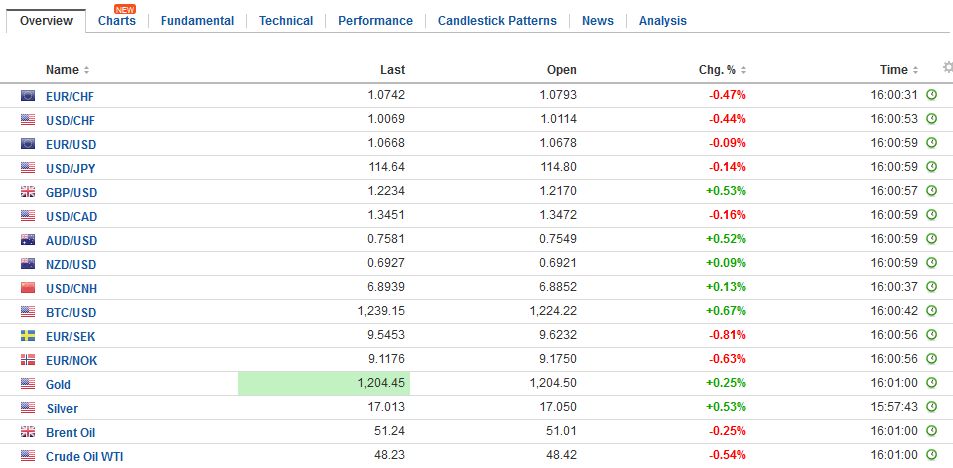

FX RatesThe UK is edging closer to triggering Article 50 to start the formal negotiations of its exit from the EU. The House of Commons is expected to reject the amendments submitted by the House of Lords. If the House of Lords passes the stripped version, Prime Minister May could announce her intention to trigger Article 50 as early as tomorrow. Another twist to the plot is the push for another Scottish referendum. While the May government could withhold legal approval, it appears that the main interest is pushing it until after the UK leaves the EU. The latest Mori poll showed a dead heat. Sterling is 0.4% against the US dollar near $1.2215. It ran out of steam in early Europe near $1.2240. Last week’s high was a little above $1.2250. A base seems to be in place near $1.2130-$1.2150. A gain above $1.2300 would lift the technical tone; otherwise, it is bouncing along its trough. The euro’s pre-weekend gains extended to nearly $.10715, its highest level in a month. It briefly took out the 61.8% retracement of the down move since February 2 (~$1.07). European participants sold into the gains recorded in Asia. The 50% retracement and the 100-day moving average of found near $1.0660. Additional support is seen in the $1.0600-$1.0620 area. |

FX Daily Rates, March 13 - Click to enlarge |

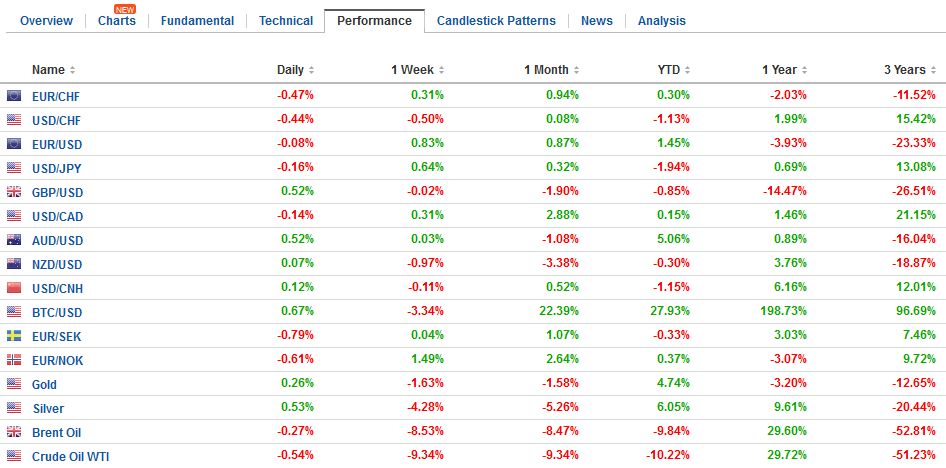

| The dollar is trading with a downside bias against the yen. US yields are softer, which is consistent with the heavier dollar tone against the yen. The day’s lows have been recorded in the European morning near JPY114.50, but the intraday technicals suggest the potential for a recovery in the North American session.

The Canadian dollar is trading within the pre-weekend range, but the Australian dollar continued to recover, reading almost $0.7600. Its 0.5% gain puts it atop the best performers. It has met the 38.2% retracement objective of its slide since late February’s $0.7740. The next target is near $0.7615. Support is now seen in the $0.7550 area. The US and Canadian economic calendars are light today. The market is positioning for this week’s events. There is some chunky option expires today. In the euro, strikes rolling off today include, $1.0646-$1.0650 (1.33 bln euros) and $1.0670 (560 mln euros) and $1.0680-$1.0690 (2 bln euros) and $1.07 (680 mln euros). In dollar-yen, JPY114.00 ($400 mln), JPY114.50 ($295 mln) and JPY115. ($690 mln). In dollar-CAD, there is CAD1.35 ($555 mln) and CAD1.3530 ($522 mln), and in the Aussie, $0.7600-$0.7610 (A$728 mln). |

FX Performance, March 13 - Click to enlarge |

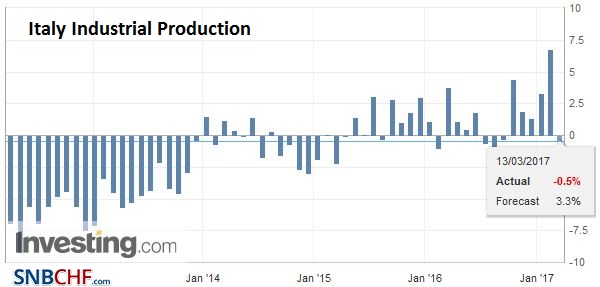

ItalyWhat will be the busiest week of the quarter, if not year, has begun off slowly. The main economy news was the Italian industrial output figures. They disappointed, and follow the poor French figures are the end of last week (-0.3% instead of the expected 0.5% gain). Italian output fell 2.3% in January after a 1.4% gain in December. The median estimate in the Bloomberg survey was for a 0.8% decline. |

Italy Industrial Production YoY, February 2017(see more posts on Italy Industrial Production, ) Source: Investing.com - Click to enlarge |

Hit by profit-taking ahead of the weekend, despite US jobs data that remove the last hurdle to another Fed hike this week, the greenback remains on the defensive. It has softened against all the major currencies and many of the emerging market currencies. The chief exception is those in eastern and central Europe.

Turkey and Dutch tensions rose over the weekend as the Dutch refused to the left Turkey’s foreign minister to enter the country to campaign, took another minister to the border, earning the wrath of Turkey’s Erdogan. The Dutch go to polls Wednesday. The Rutte government is credited with handling the affair well, and although supporters for the Freedom Party, may have become more enthusiastic, the PVV does not appear to be growing its base. Overall, the market impact looks minor.\

Last week’s ECB meeting gave investors the clear impression that the central bank recognizes that the downside risks have lessened in the region. No more rate cuts are anticipated, and greater attention is being given to the eventual exit from the unorthodox monetary policy. The sequencing of the exit between asset purchases and negative interest rates may take a different form than the exit by the Fed or the earlier exit by the BOE.

Still, we can’t help but wonder who leaked news that there was a discussion along these lines (reduced negative deposit rate before asset purchases are complete) and to what end. It seems those who are critical of the ECB’s course may have had the incentive to provide that information to the media. Of course, it is reasonable to expect a push back. It came from Belgium’s central banker Smets, who recognize the macro improvement, was clear that no decisions were taken.

Also, over the weekend, the head of the US administration’s strategic and policy committee, Schwarzman, told a CNN interviewer the confrontation with China that candidate Trump had seemed to emphasize, might not materialize after all. Treasury Secretary Mnuchin had already indicated that the normal Treasury review would take place before any judgment was made about China and its yuan policy. Chinese stocks, especially those that trade in Hong Kong, did well. The Hang Seng Enterprise Index rallied 1.8%, the most since November, and is now up 9.2% year-to-date. The MSCI Asia Pacific Index advanced 0.8%. The index has been down only two week’s this year for a 7.7% gain.

European shares began firmer but surrendered the early gains. The Dow Jones Stoxx 600 was fractionally lower in later morning turnover. Telecoms and energy led most sectors lower. Materials seemed to like the rebound in some industrial goods (iron ore, zinc, copper) and the second was up nearly 1%.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Italy Industrial Production,Japan Core Machinery Orders,newslettersent