It was not even a month ago when we last looked at the total amount of negative yielding debt around the globe, and were shocked to find that according to Fitch, for the first time in history (obviously), there was over $10 trillion in negative yielding debt. Fast forward 4 weeks later, and the grand total is now $1.3 trillion higher, or $11.7 trillion.

|

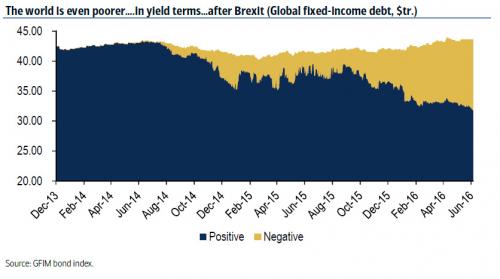

The split between positive and negative yielding debt is shown in the chart below: The world is even poorer … In yield terms…after BrexitIn a report released earlier, Fitch updates on the “investors’ flight to safe assets following the UK’s EU referendum on June 23” and finds that the global total of sovereign debt with negative yields was a staggering $11.7 trillion as of June 27, up $1.3 trillion from the end-May total. Brexit-related concerns drove more long-dated bond yields negative, with particularly big shifts in German, French and Japanese yield curves during June. As Fitch notes, worries over the global growth outlook, further fueled by Brexit, have continued to support demand for higher-quality sovereign paper in June. Widespread adoption of unconventional monetary policies, including large-scale bond-buying programs and negative deposit rates, have driven the large increases in negative-yielding debt seen this year. |

It was not even a month ago when we last looked at the total amount of negative yielding debt around the globe, and were shocked to find that according to Fitch, for the first time in history (obviously), there was over $10 trillion in negative yielding debt. Fast forward 4 weeks later, and the grand total is now $1.3 trillion higher, or $11.7 trillion. - Click to enlarge |

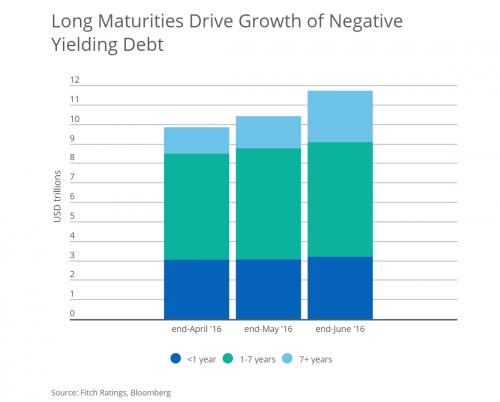

Long Maturities Drive Growth of Negative Yielding DebtThe chart below highlights the monthly changes in the outstanding par amount of negative-yielding sovereign debt by maturity bucket. The biggest drivers of the total increase during June were seen in longer-dated bonds. For example, German 10-year bund yields swung into negative territory and sub-zero yields moved further out on the curve for Japan — now out to 17 years. Also, in Switzerland, virtually all sovereign debt carried a negative yield on June 27. |

It was not even a month ago when we last looked at the total amount of negative yielding debt around the globe, and were shocked to find that according to Fitch, for the first time in history (obviously), there was over $10 trillion in negative yielding debt. Fast forward 4 weeks later, and the grand total is now $1.3 trillion higher, or $11.7 trillion. - Click to enlarge |

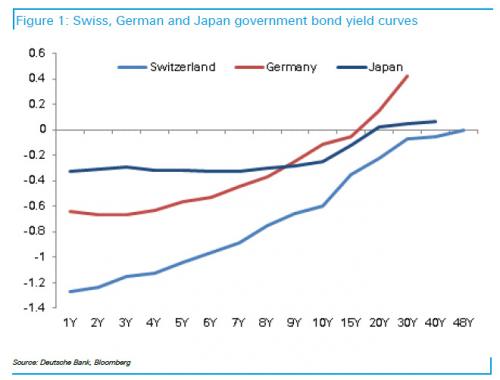

Swiss, German and Japan government bond yield curvesAs DB’s Jim Reid writes, yesterday we saw the Swiss yield curve actually trade negative the whole way out the curve. The longest dated Swiss government bond due in 2064 (so 48 years) touched -0.0082% at one stage before settling at +0.011% by the close. The chart below shows the Swiss yield curve to show how remarkable this is. We’ve also added the JGB curve where the longest dated bond due in 2056 (40 year) is trading at a minuscule 6bps and the Bund curve where the longest dated 30y bond is trading at 42bps. |

It was not even a month ago when we last looked at the total amount of negative yielding debt around the globe, and were shocked to find that according to Fitch, for the first time in history (obviously), there was over $10 trillion in negative yielding debt. Fast forward 4 weeks later, and the grand total is now $1.3 trillion higher, or $11.7 trillion. - Click to enlarge |

Japanese government bonds (JGBs) continue to represent about two-thirds of the global total ($7.9 trillion), while Germany and France each now have over $1 trillion in sovereign debt with sub-zero yields. Japan’s negative-yielding debt total grew by about 18% during the month, while Germany and France’s total grew by 8% and 13%, respectively. European negative-yielding debt increases were offset in part by an approximately $0.2 trillion reduction in the Italian total since May 31. This likely reflected investor risk aversion related to Italy leading up to and following the Brexit referendum.

The spread of negative yields into longer-dated paper was particularly evident in June. A total of $2.6 trillion in sovereign bonds with maturities of seven years or more now trade at a negative yield. This compares with the end-April total of $1.4 trillion.

The increasing amount of long-term negative-yielding debt underscores the challenges faced by large bond investors such as insurance companies that need to match long-term liabilities with similar maturity assets. As more of the global universe of safe assets drops into negative-yielding territory, income for these investors continues to fall.

UK sovereign bonds continue to trade at positive yields across the curve, but the Brexit vote has had a dramatic effect on the UK yield curve. Following the June 23 referendum, 10-year gilt yields dropped by 44 bps to 0.93% as of June 27, according to Bloomberg.

The $11.7 trillion total, which includes $3.2 trillion of short-term and $8.5 trillion of long-term sovereign debt, is influenced by the dollar’s exchange rate with the yen and euro. During June, the dollar rose slightly against the euro, but weakened significantly (approximately 9%) versus the yen. This had a major impact on the dollar value of yen-denominated negative-yielding debt in our latest analysis, pushing the JGB total up by approximately $0.6 trillion beyond increases that would have occurred on an FX-neutral basis.

Full story here Are you the author?Tags: Bond yield,France,Insurance Companies,Italy,Japan,Japanese yen,Jim Reid,newslettersent,public debt,Swiss government bonds,Switzerland,Yield Curve