Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

The EU response to Brexit is important. The EU summit and the talks with Turkey are very important. Brexit leaders seem as surprised and unprepared for the results as anyone. And a preview on economic data for the week.

The UK choice to leave the EU on a 52%-48% vote is one of those moments that define before and after. It is true that there are examples of the EU not liking the outcome of a referendum and allowed a repeat, such as in the Maastricht Treaty or the European Constitution Lisbon Treaty. Efforts for another referendum or a Scottish or Welsh veto do not seem to be the path forward. That will not fly now. Tsipras of Greece chose to ignore the results of his referendum last summer. We may not be the first to notice this, but the UK is not Greece.

Who is invoking article 50, that starts the exit from the union?

Indeed that is the subject of the first of what promises to be countless dispute.When should the UK invoke Article 50 of the Lisbon Treaty, which formally begins the divorce negotiations? The longer it takes, the more the uncertainty festers.

At first, Cameron has suggested an early decision. Ironically, the leaders of the Brexit movement are in no hurry. After the results, Cameron announced two things. First, that he would resign by October. Second, that he would not invoke Article 50, but would leave it to his successor.

With victory in hand, the Leave camp is in disarray. Like a dog chasing a car and doesn’t know quite what to do when it catches it, the Leave camp seems as surprised as anyone with the results. UKIP’s Farge’s seemingly concession as the polls closed was itself remarkable. The Tories are trying to sideline him, excluding him from the process. The Leave camp does not appear to have a first hundred-day game plan.

Many European officials acted as spurned spouses upon learning that divorce papers have been filed. They cannot wait to see the UK’s back. The head of the European Parliament called it “scandalous” that Cameron would stay on until October. He no longer holds the authority of the office. Europe is being held hostage by the internal politics of the Tory Party. Merkel, after the counselor of caution, noted that while there was no rush, it should not take forever.

Even if this issue is not resolved, the impact of the UK’s decision will be felt immediately in the EU’s decision-making. EC President Juncker called to the resignation of all the UK members of the European Parliament. UK’s EU Commission, Hill, who headed up finance, resigned over the weekend. The EU heads of state summit will need to meet without Cameron to discuss the response. The summit is arguably the most important, or at least one of the most important events in the week ahead. The response to the UK’s decision plays just as important of a role in shaping the future as the UK’s decision.

The internal politics of the UK are important. Churchill had the right temperament to lead the UK to fight WWII; voters decided that another person, Attlee, was needed in peace. Given the fissure in the Tory Party and raw, hard feelings, the Tories are loath to have a general election when the parliamentary system does not require it. Should a partisan, like former London Mayor Johnson, be rewarded, or should the party chose someone who can begin to heal the wounds, like Home Secretary May.

The issue is larger than who occupies 10 Downing Street. Sturgeon, who heads the Scottish National Party, announced that the process of a second referendum for its independence has begun. Some observers raise question of the future of Northern Ireland.

The Brexit vote is an attack on the EU.It is a blow whose magnitude is still not fully clear. This is the time that some countries may press for an advantage. Perhaps it is a concession about this year’s budget. A new government in Spain may find a somewhat more pliant EC. Alternatively, maybe it is a favorable ruling on the implementation of the Bank Resolution and Reconstruction Directive, that some are advocating. It could be some other issue, like where the European Banking Authority should be headquartered now that it cannot be in the UK. London will likely lose its critical passporting rights when it leaves the single market. How can a country secure some of this business?

There may be wide recognition that the EU needs to revise its vision, but that is where the consensus ends. French and Polish officials have called for treaty changes. Merkel and others oppose taking dramatic action. The give the constellation of political forces, sentiment, the state of the economy and the labor market, and the divisiveness of immigration, opening up the treaties now could provide an opening for the variant of populism that appears to be rising everywhere. It would begin a process whose outcome could be unpredictable and uncontrollable.

Has Brexit started a movement for less EU integration?

There are two axis in confronting Europe. One is about more or less integration. The other is more or less democracy. Even if many of us got it wrong in the end, policymakers have developed contingency plans. The EU summit will see these play out. The meeting of the foreign ministers from the original EU founders (Germany, France, Italy, Belgium, Netherlands, and Luxembourg) over the weekend seemed to strike the wrong chord.

An issue on the lips of many is whether Brexit has started a movement. Will it be a shot in the arm of those forces that went to exit the EU themselves? Is there some global meme that links the UK decision to leave the EU and the election of Trump as the next US President? Nationalism does appear to be contagious, especially its exclusive variants, but the roots are domestic, even if it cannot be simply reduced to economic self-interest.

If the market underestimated the strength of the anti-elite and anti-immigrant nationalism, it may also fail to appreciate the commitment to the European Project. This may an even more powerful impulse now that it has been attacked. Perhaps an indication of this type of response may be found on the website of Italy’s 5-Star Movement (5MS), which has been critical of the EU. According to reports, 5MS has stepped back from its previous calls for an EMU-referendum and now seems inclined to transform the EU from within.

The Turkey Visa Question

If the EU Summit is the most important event in the week ahead, the high-level meeting between Turkey and EU officials is the second most important event. It is a delicate situation and a week after losing the UK, if the EU does not play its card right, it can renew the deluge of refugees into Greece.

There are two issues. First, the EU has and continues to be ambivalent about Turkey joining. It flirts and teases but has offered little satisfaction. The dalliance has lasted half a century. Merkel took a political expedient way to deal with the refugee problem that was threatening the foundation as it eroded the Schengen Agreement which gave Turkey exactly the kind of leverage that President Erdogan understands.

As part of the deal on refugees, the EU agreed to open a new chapter (set of discussions) that cover financial and budgetary issues. It is the sixteenth chapter of 35 chapters that have been opened. Only one has been closed. Erdogan accuses the EU of dragging its feet and threatens to hold a referendum of his own on whether Turkey wants to halt membership talks.

The second issue is about visa-free travel through the Schengen area by people by Turkish passports. Turkey has met many of the EU’s requirements, but there is an outstanding issue that threatens to sour the refugee deal. The EU is insisting that Turkey narrow its definition of terrorism, as the country fights the PKK, which is a widely recognized as a terrorist organization. It appears that the broad definition of terrorism allows the curtailing human rights and freedom of the press. Erdogan refuses to concede.

Functioning of capital markets and Currency Interventions

The G7 issued a statement before the weekend, ostensibly to reaffirm its commitment to ensure the smooth functioning of the global capital markets, and the willingness to cooperate as necessary. It reiterated its desire for stable and orderly markets. The Fed’s swap lines that make dollar funding available through the ECB and BOJ are the first line of defense. They proved sufficient during the Great Financial Crisis.

Japanese officials may be tempted to intervene, but perhaps the only thing worse than intervention is failed intervention.The track record of unilateral Japanese intervention is nothing to write home about. Although speculators have been buyers of yen (judging from the futures market), and foreigners have been buying Japanese government bonds (weekly MOF data), the yen’s strength appears to have a real demand as well.

It appears to be coming from Japanese investors themselves, repatriating foreign earnings and hedging foreign portfolio investment. There has been some suggestion that Japanese corporates have begun hedging their foreign retained earnings. They had been earning superior yields, which have been offset and more by the yen’s strength.

Economic Data

The economic data in the week ahead pales in comparison to the reverberations of Brexit. However, there are a few macroeconomic takeaways.

United StatesFirst, Q1 US GDP is expected to be revised to 1.0%, twice the initial estimate, though still disappointing. The second quarter is promising to be considerably better. The May personal consumption is expected to be consistent with around a 3.5% quarterly annualized pace. If the other GDP components of are a wash, Q2 GDP would be around 2.5% GDP. June auto sales may be flat on a sequential basis but at elevated levels. |

Click to enlarge. |

EurozoneSecond, the eurozone reports the flash estimate of CPI on June 30. It has been negative since February. In June it is expected to be flat. That this is a function of higher energy prices will be concluded if the core rate is unchanged at 0.8%. |

Click to enlarge. |

United KingdomThird, the UK data is irrelevant, but it offers a bit of a base case, of how the UK was performing before the Brexit shock hit, even if some uncertainty bled into an already moderating economy. Growth in Q1 is expected to be confirmed at 0.4% for a 2.0% year-over-year pace. The Q1 current account deficit is expected to have narrowed to GBP28 bln from nearly GBP33 bln in Q4 15. Is there not some chance that Brexit makes it more difficult (expensive) to finance? Will it worsen? The June manufacturing PMI is expected to be confirmed at 50.1, leaving it average Q2 more than a full index point below the Q1 average. However, sentiment has been worse than actual manufacturing output. Will the two converge now? |

Click to enlarge. |

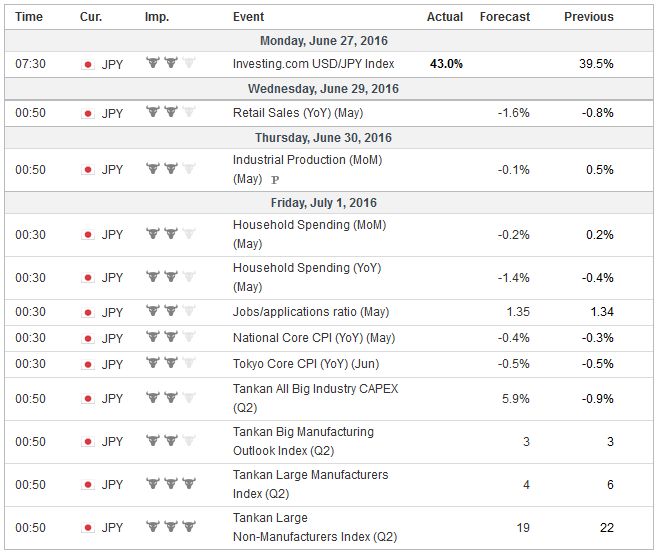

JapanFourth, the slew of Japanese data on top will likely provide the Bank of Japan will hard evidence that monetary policy may not be sufficiently accommodative given the economic conditions. The economy continues to sputter. May retail sales and especially overall household spending are falling. Industrial output may have contracted. And May’s CPI, under various measures, is likely moving in the wrong direction. Will it be surprising if sentiment in the Tankan (July 1 in Tokyo) deteriorates? |

Click to enlarge |

Full story here Are you the author?

Tags: Angela Merkel,Article 50,newslettersent,Post-Brexit,Recep Erdoğan