Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

I was on Bloomberg’s Day Break with the team and guest Anne Lester from JP Morgan discussing oil and inflation. Oil prices had bounced back at the end of last week and were lifted further on news that Saudi Arabia and Russia were inclined to support extending output cuts not just until the end of the year, but through Q1 18.

I was on Bloomberg’s Day Break with the team and guest Anne Lester from JP Morgan discussing oil and inflation. Oil prices had bounced back at the end of last week and were lifted further on news that Saudi Arabia and Russia were inclined to support extending output cuts not just until the end of the year, but through Q1 18.

I make two points. First, that US yields seem to be largely decoupled from the oil prices. This is purely a descriptive claim, not normative. Typically the percent change in the US 10-year yield is positively correlated with percent change in oil. This has not been the case since early March. In fact, over this period the correlation is inverse. Even when we run the correlations on the simply the level of oil and US yield level, the correlation is inverse (not by a lot but the sign is the important).

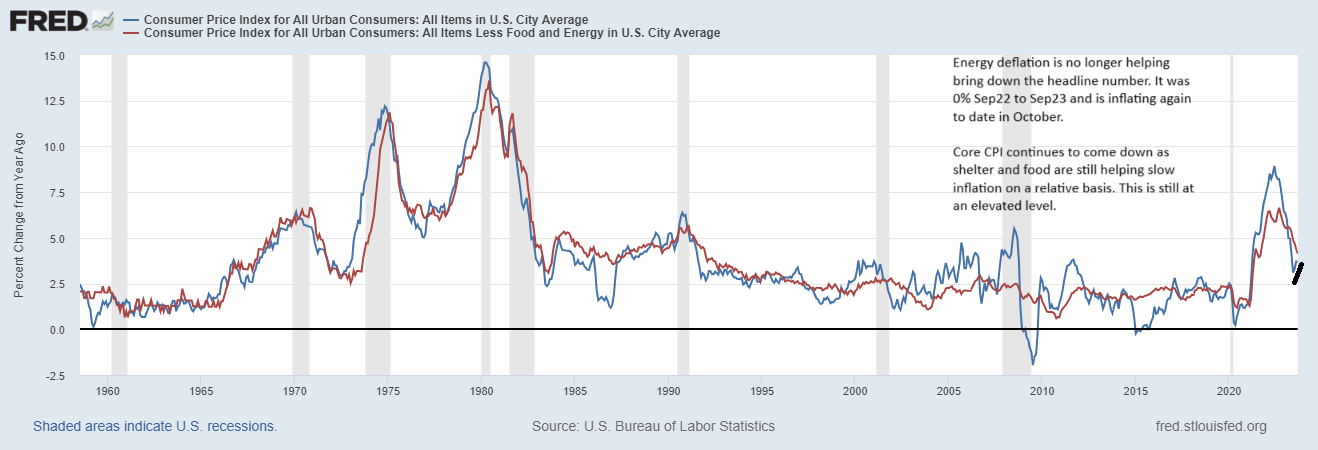

The second point is that the weakness of core CPI reported before the weekend was important because other measures of inflation expectations, like the University of Michigan’s survey and the shape of the US yield curve also softened. One concern I mention is that rents seem to be softening and this could weigh core PCE. Anne suggests the price of oil can be a tailwind for oil companies, but is concerned that a rise in oil prices may curb household consumption.

Full story here Are you the author?Tags: Cool Video,newslettersent,OIL